Prices

October 10, 2014

US Steel Mill Shipments of Sheet and Strip Products through August 2014

Written by Peter Wright

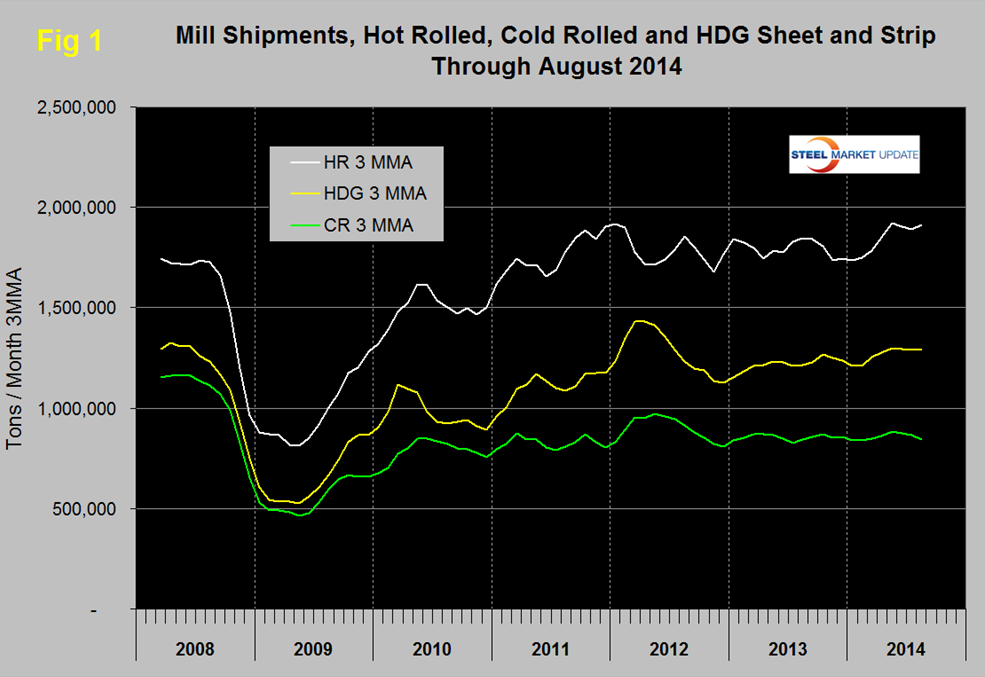

Following the post-recession recovery, shipments of hot rolled steel from US mills to domestic locations have been trending in a range for three years. Shipments of hot dipped galvanized sheet and strip declined strongly in Q2 through Q4 2012 and have climbed slightly in 2014. Cold rolled shipments have shown little direction for almost two years, (Figure 1). This analysis is based on shipments to domestic locations plus exports and uses the AISI AIS10 monthly report and Commerce Department trade data.

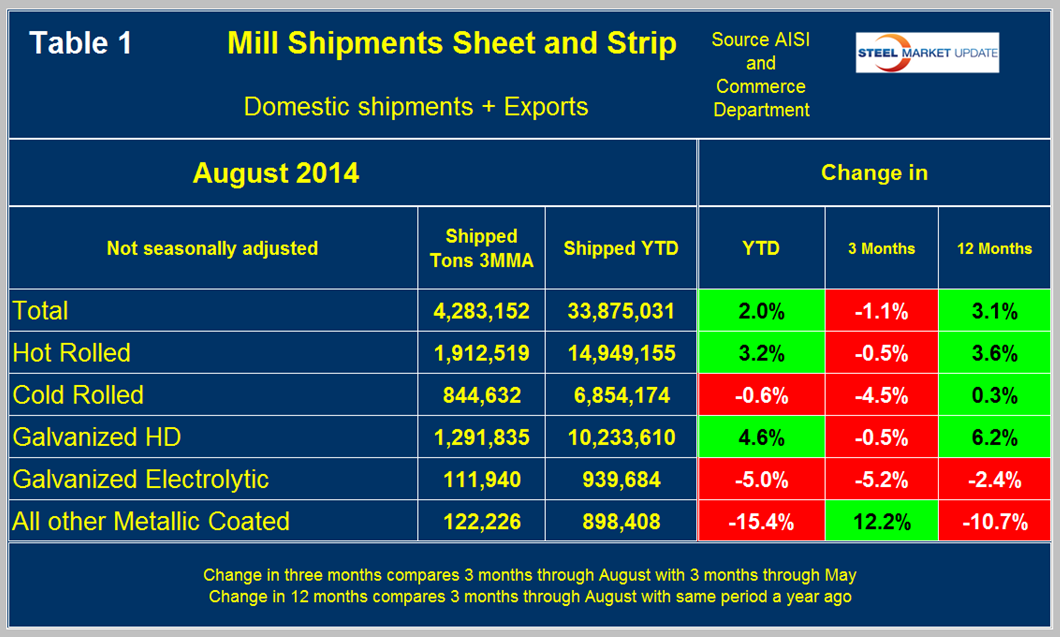

Table 1 shows that total shipments of sheet and strip products including hot rolled, cold rolled and all coated products were up by 2.0 percent YTD through August compared to the same period last year.

In the three months through August compared to three months through May, the total tonnage was down by 1.1 percent. Comparing three months through August with the same period a year ago, the tonnage of sheet and strip products was up by 3.1 percent. Comparing YTD shipments for 2014 and 2013 for individual products, hot band was up by 3.2 percent and HDG by 4.6 percent. Cold rolled was down by 0.6 percent, electro galvanized by 5.0 percent and other metallic coated, (mainly Galvalume) by 15.4 percent (Figure 2).

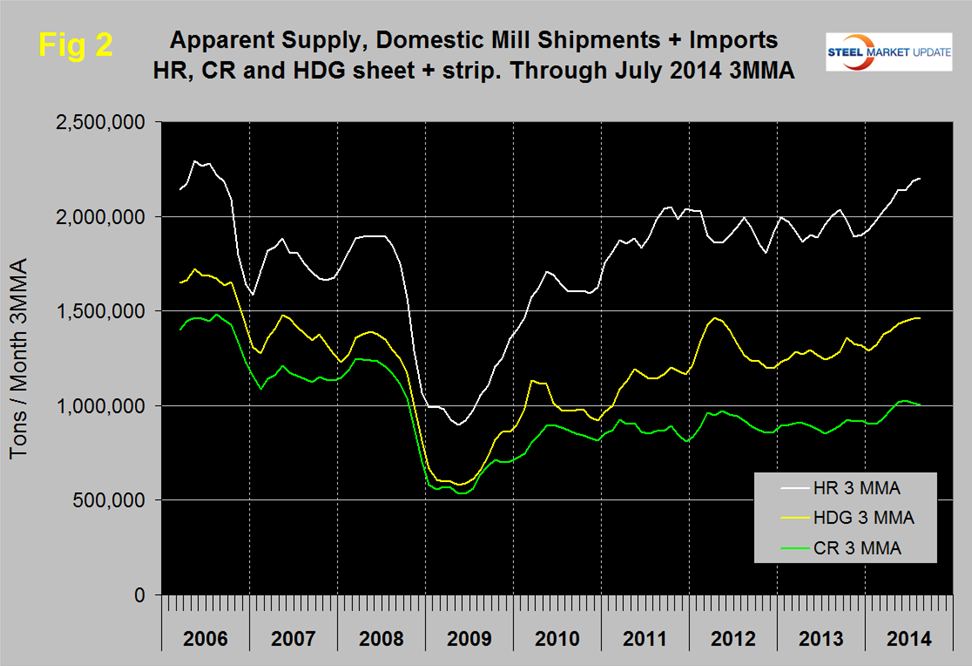

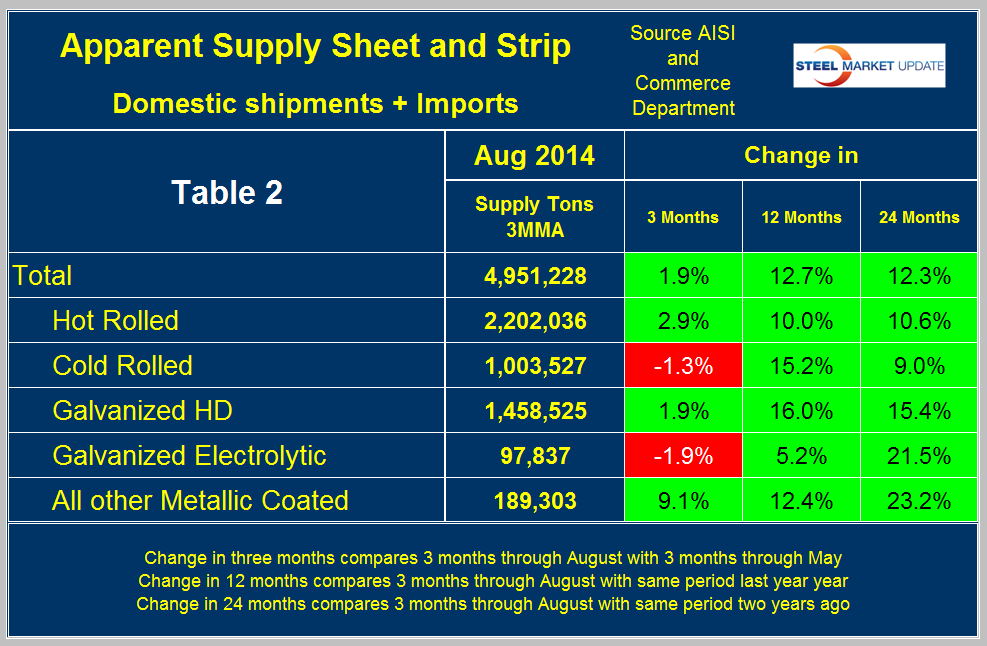

The situation with the supply of sheet products to the US market is quite different to that of mill shipments as imports have taken an increasing market share. In the three months through August imports of sheet and strip products were up by 60.8 percent year over year which compares to the increase of domestic mill shipments of 3.1 percent mentioned above. Table 2 shows the change in supply by product. In three months through August year over year total supply of sheet and strip products was up by 12.7 percent and mill shipments were up by 3.1 percent.

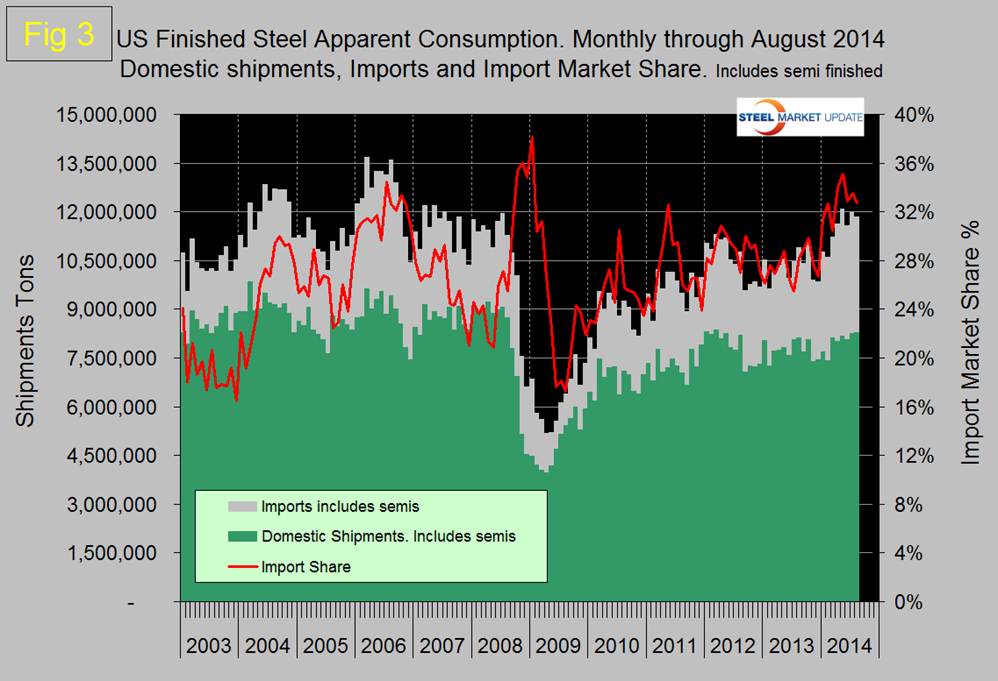

Figure 3 shows import market share of all steel products including semi-finished to have been above 32 percent for most of this year. Apparent consumption is back to its pre-recession level but mill shipments are still down by about 800,000 tons per month.