Prices

March 21, 2015

Comparison Price Indices: Still a Slippery Slope

Written by John Packard

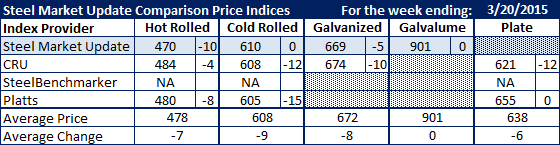

This weeks Comparison Price Indices analysis saw flat rolled steel prices as continuing their 8 month slide.

Benchmark hot rolled coil (or bands) moved Lower by an average of $7 per ton this past week. Of the four steel indexes followed by Steel Market Update (including our own) the spread from low (SMU at $470) to high (CRU at $484) is $14 per ton.

The spread on cold rolled is less than HRC with Platts at $605, CRU $608 and then SMU at $610 per ton making the spread a mere $5 per ton.

The galvanized spread has also shrunk between CRU and ourselves. Only $5 per ton separates us with SMU at $669 per ton and CRU at $674 per ton (.060″ G90 is the benchmark used for galvanized).

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

CRU: Midwest Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.