Prices

April 14, 2015

Price Spread Suggests Foreign Steel Imports Should Break Down in Coming Months

Written by John Packard

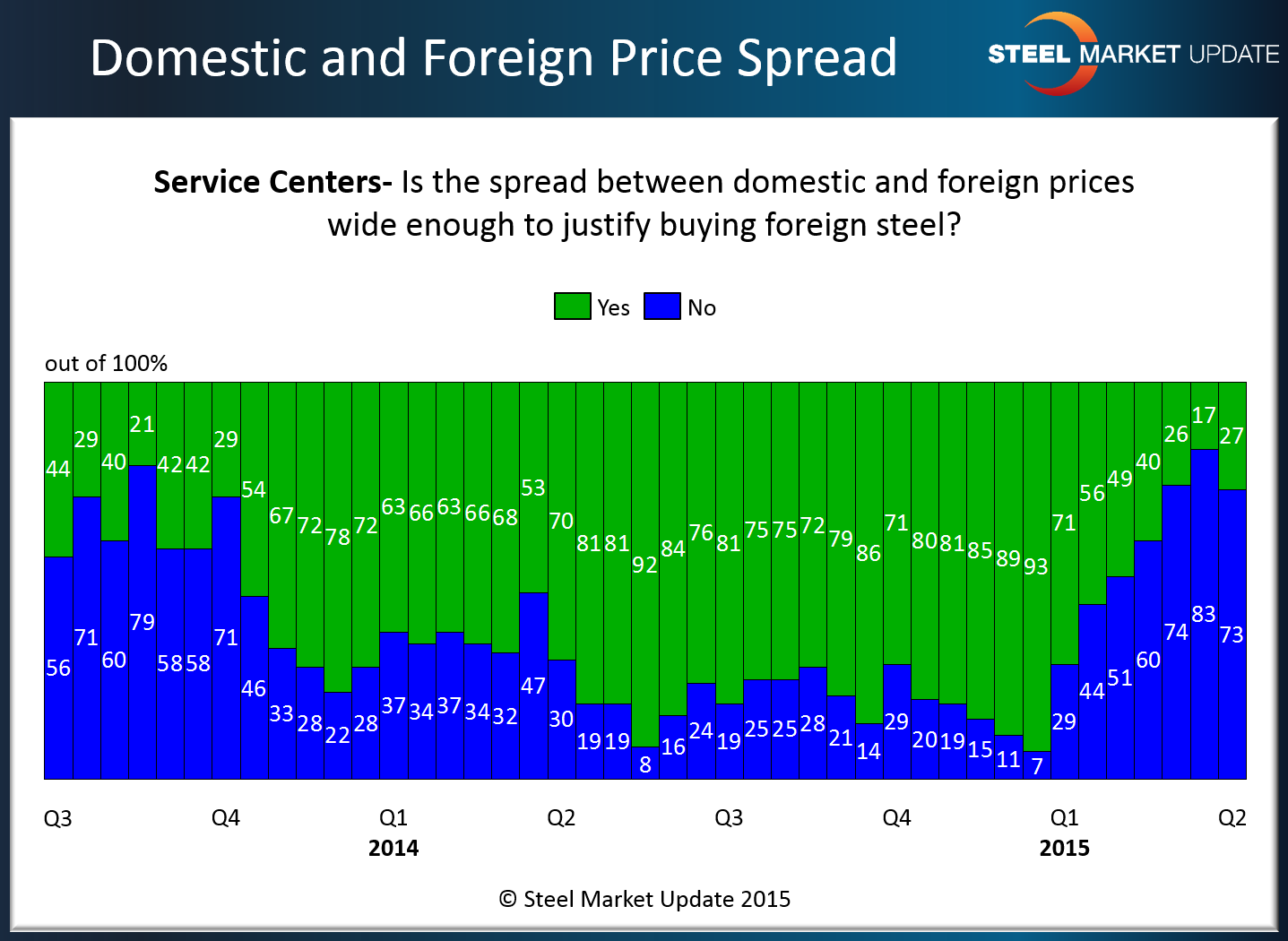

One of the questions asked during the flat rolled steel market analysis we conduct twice per month is regarding the spread between domestic and foreign steel pricing. When spreads are large, as they were for most of calendar year 2014, then you can expect a surge in imported steel. As the spread subsides the need to go off-shore diminishes and foreign steel imports wane.

We find the following graphic to be especially telling when trying to understand both the surge in imports and then to project where imports will be over the coming months as most foreign steel lead times run from 3 to 5 months before the steel arrives in the U.S.

Out of curiosity we took a look at a number of the quarters from 2nd Quarter 2013 then 3rd Quarter 2014 and beyond. Looking at our graph, our expectation is that import tonnage totals should have begun to surge during 1st Quarter 2014 and remain quite high through the balance of the year and into the 1st Quarter 2015.

Looking at the import numbers that is exactly what we found in the data. Assuming a minimum three month lead time lag the first import surge reported should be the month of January 2014. Buyers were reporting a widening spread in 4th Quarter 2013 and that spread continued for all of 2014, peaking in December 2014. If our logic is correct, we should see continued high import levels through March 2015 and then they should drop off fairly rapidly during second quarter 2015, getting back to levels last seen in 2013.

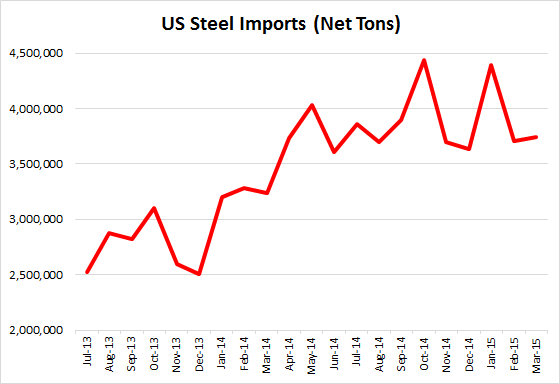

In the graph below we provide total steel import statistics (net tons) going back to July of 2012. We chose to go back to 2012 so we could show how 2012 and 2013 were “normal” import years. The monthly average for 2012 was 2.8 million tons, 2013 was 2.7 million tons and 2014 was 3.7 million tons. The first 3 months 2015 are averaging 3.95 million tons.

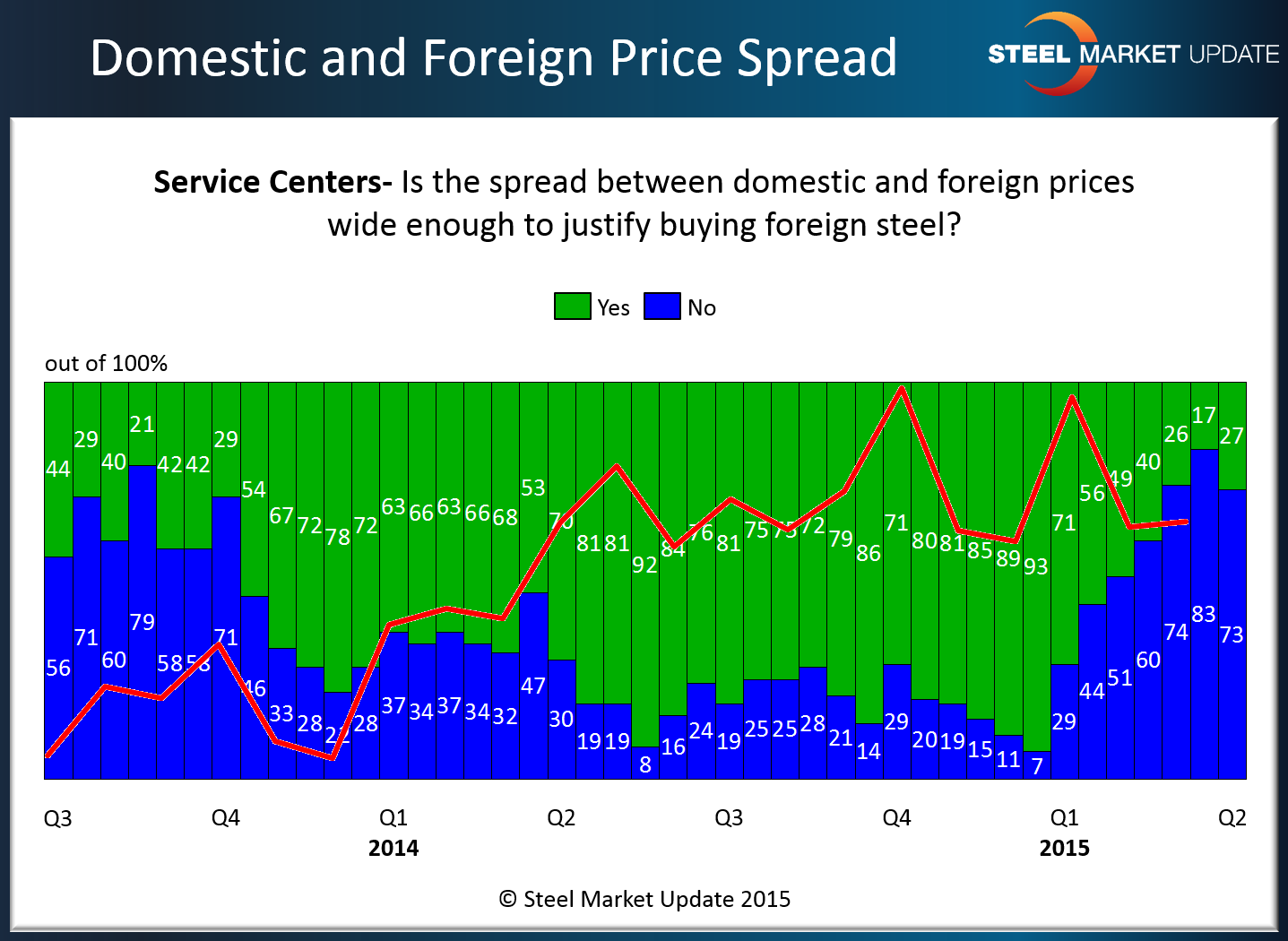

Here is the same data shown above placed on top of the previous graphic to give you a better feel for the timing of the movement in tonnage.

The question is: If the spreads between foreign steel and domestic steel do not increase over the next few months will we see more “normal” import patterns emerge where the monthly totals decline to the 2.7-2.8 per month figure?

SMU data is suggesting that will be the case.