Prices

July 7, 2015

May Imports Total 3.4 Million Net Tons

Written by John Packard

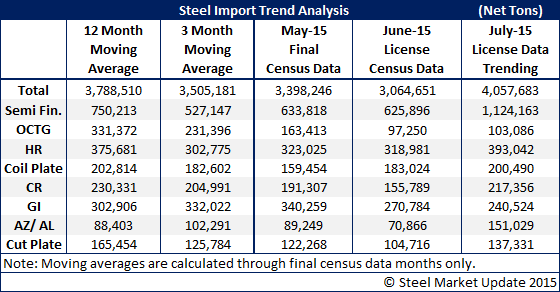

Final Census Data for May foreign steel imports was released by the U.S. Department of Commerce (US DOC) earlier today. Imports for May were 107,000 net tons lower than the month of April. The May 2015 number is 600,000 net tons lower than the 4,033,351 net tons received during the month of May 2014.

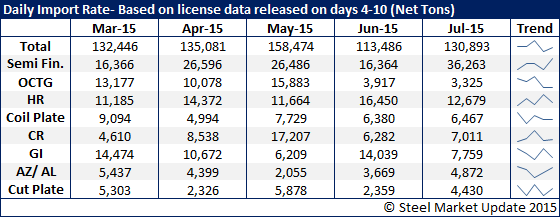

June license data was also updated by the US DOC and the month appears as though total tonnage will be right around 3.0 million net tons. One items that sticks out is OCTG, which appears will be below 100,000 net tons or more than 3 times lower than the 12-month moving average.

We are reporting the “trend” for July imports based on license data through the 7th of the month. At this moment July licenses are in line with what we saw during January through May. We do not put a lot of weight on the trending number since it is so early in the month, but we thought we would share it with you for your review. The trend is determined by calculating the daily average and then projecting that rate to remain through the month which gives us the number shown. Our opinion is the number will come in closer to what we are seeing in June (and perhaps below 3.0 million net tons).

Below is a table showing daily import rates. We added a trend line in the far right column to give a general trend for each product. Note that the license data figures below were gathered between the 4th and 10th day their respective month.