Market Data

July 13, 2015

Shipments and Supply of Sheet Products through May 2015

Written by Peter Wright

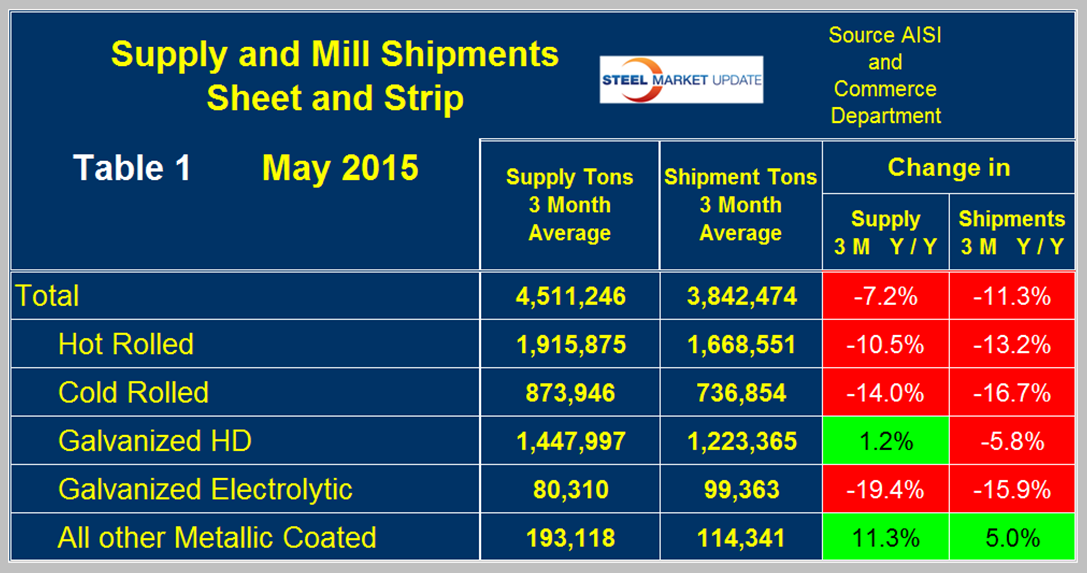

This report compares domestic mill shipments and total supply to the market. It quantifies market direction by product and enables a side by side comparison showing the degree to which imports have absorbed demand. Sources are the American Iron and Steel Institute and the Department of Commerce with analysis by SMU. Table 1 shows both supply and mill shipments of sheet products (shipments includes exports) side by side as a three month average for the periods March through May for both 2014 and 2015.

Comparing these two periods total supply to the market was down by 7.2 percent but shipments were down by 11.3 percent. In other words, imports took share from the domestic mills. Table 1 breaks down the total into the individual sheet products. Supply of hot and cold rolled was down by 10.5 percent and 14.0 percent respectively year over year and US mill shipments were down by 13.2 percent and 16.7 percent respectively. HDG had a 1.2 percent gain in supply but shipments were down by 5.8 percent. Electro-galvanized (EG) which enjoys a trade surplus had a greater decline in supply than it did in shipments. Other metallic coated products (OMC, mainly Galvalume) continued to buck the trend and enjoyed an 11.3 percent increase in supply and a 5.0 percent increase in shipments. A review of supply and shipments separately for individual sheet products is given below.

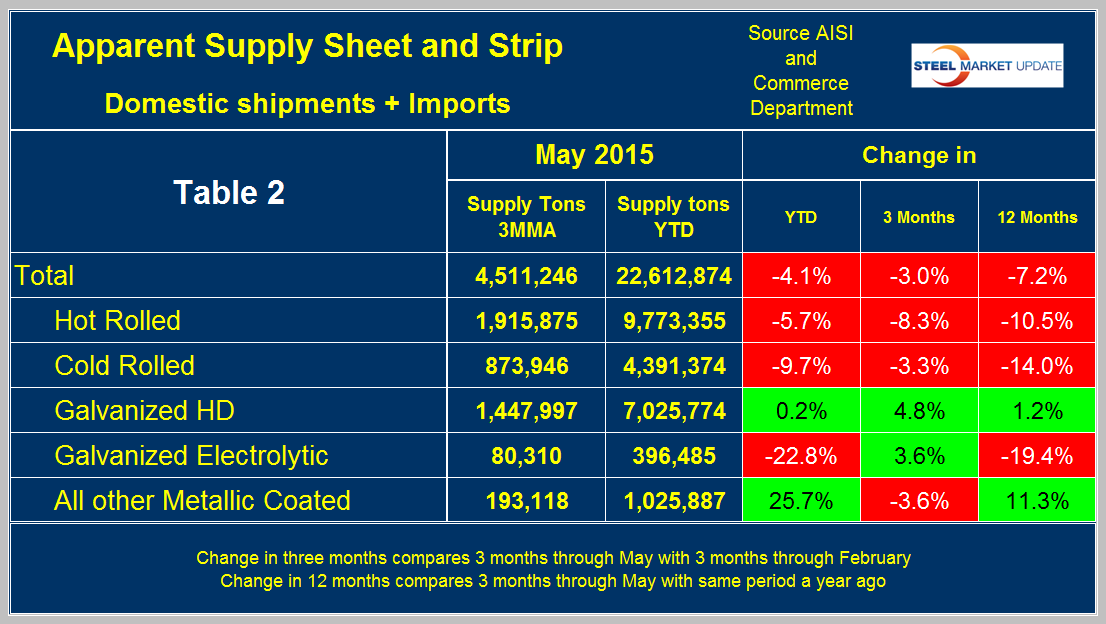

Apparent Supply is a proxy for market demand and is defined as domestic mill shipments to domestic locations plus imports. In the three months through May 2015 average monthly supply of sheet and strip was 4,511,246 tons, down by 3.0 percent from the previous three month period, December through February, down by 7.2 percent from the same period last year and down by 4.1 percent YTD compared to the first five months of 2014. Table 2 shows the change in supply by product on the same basis through May.

There is a big difference between products. Hot and cold rolled followed the overall trend but coated products did not. HDG strengthened slightly in all three time comparisons. The results for EG look strange. YTD was down by 22.8 and in 3 months was up by 3.6 percent. This is because the YTD result is year over year and the 3 month result compares three months through May with 3 months through February. The first half of 2014 was strong for EG then faded significantly. Results for other metallic coated look strange in the opposite direction because the 2nd half of 2014 was stronger than the 1st half. YTD growth year/year for OMC products was strong at 25.7 percent but that has faded in the last three months through May compared to three months through February.

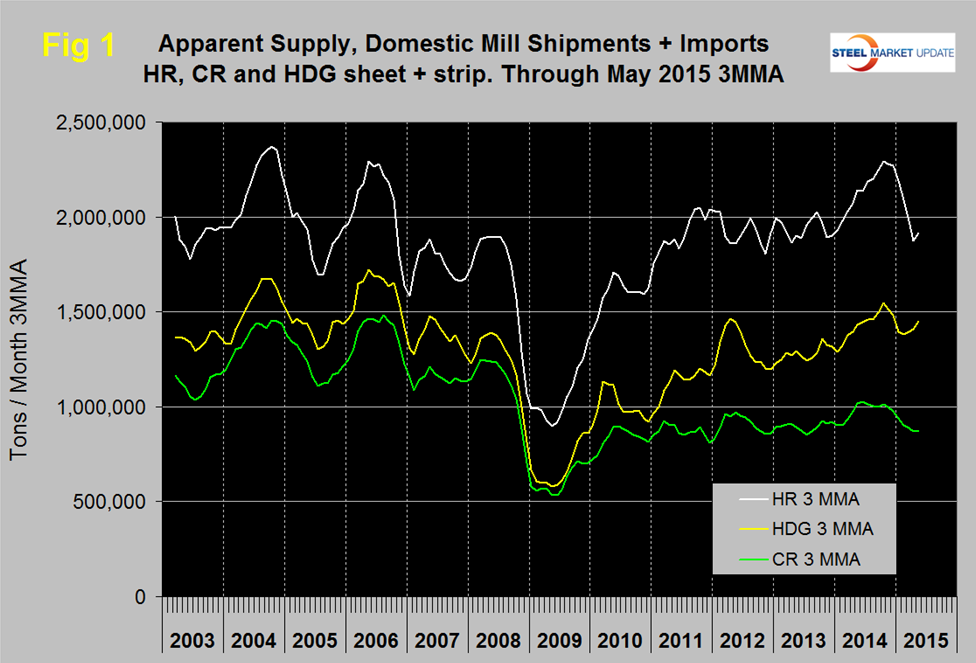

Figure 1 shows the long term supply picture for the three major sheet and strip products, HR, CR and HDG, since January 2003.

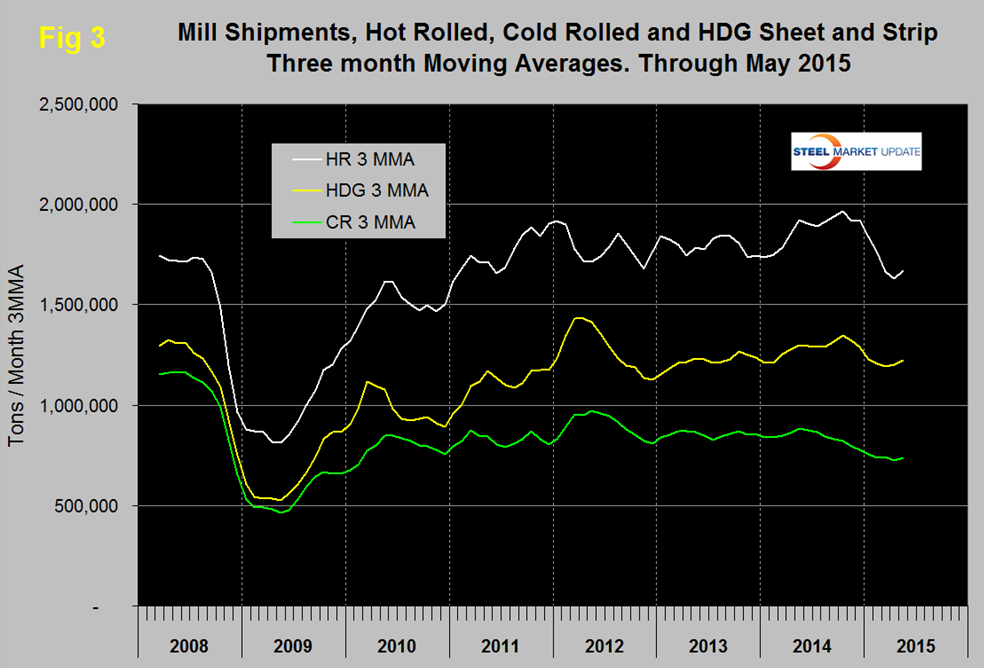

Hot rolled declined strongly in the first four months of this year but picked up slightly in May, (Note these are three month moving averages). Cold rolled declined each month November through April and was up very slightly in May. Hot dipped galvanized has strengthened for the last three months. In Q4 2014 all three were in higher demand than at any time since the recession, that is no longer the case. Hot band was range bound for 2.5 years until April 2014 when it broke out and advanced through October followed by a small decline in November and December and a more rapid decline this year. Cold rolled supply fell below a million tons to 977,452 tons in December (3MMA) after being above that threshold for six of the previous seven months and in May totaled 874,000 tons. Prior to this recent past the last time cold rolled exceeded a million tons was in October 2008 as we prepared to go over the cliff. Hot dipped galvanized had a strong bump in H1 2012, declined in H2 2012 and steadily improved for 22 months with a small decline in November and December, a more rapid decline in January then a pickup in the last three months.

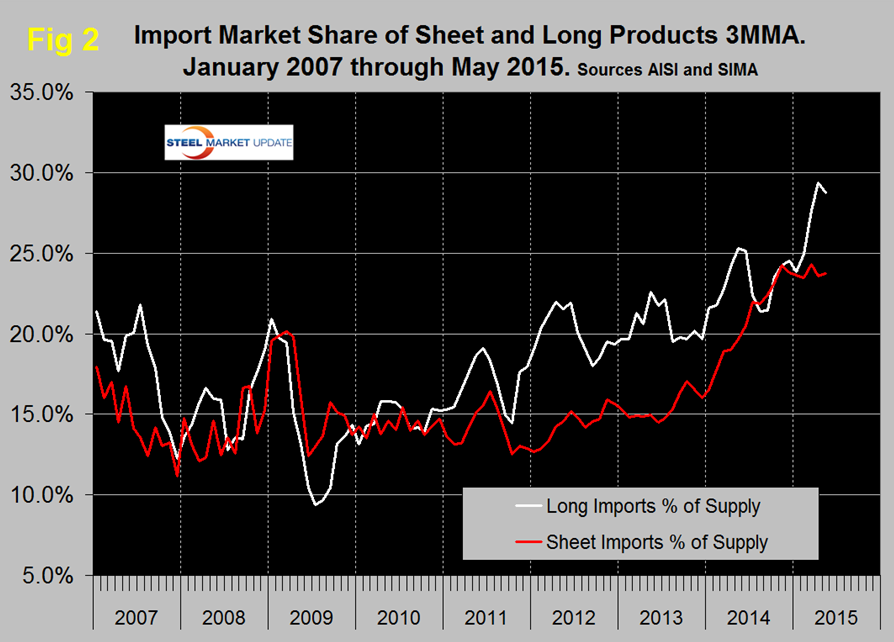

Figure 2 shows import market share of sheet products and includes long products for comparison.

Based on a 3MMA the import market share of sheet products was 23.7 percent in May and has ranged between 23.1 percent and 24.3 percent since October last year. The months March and November had the highest import market share since the beginning of the recovery.

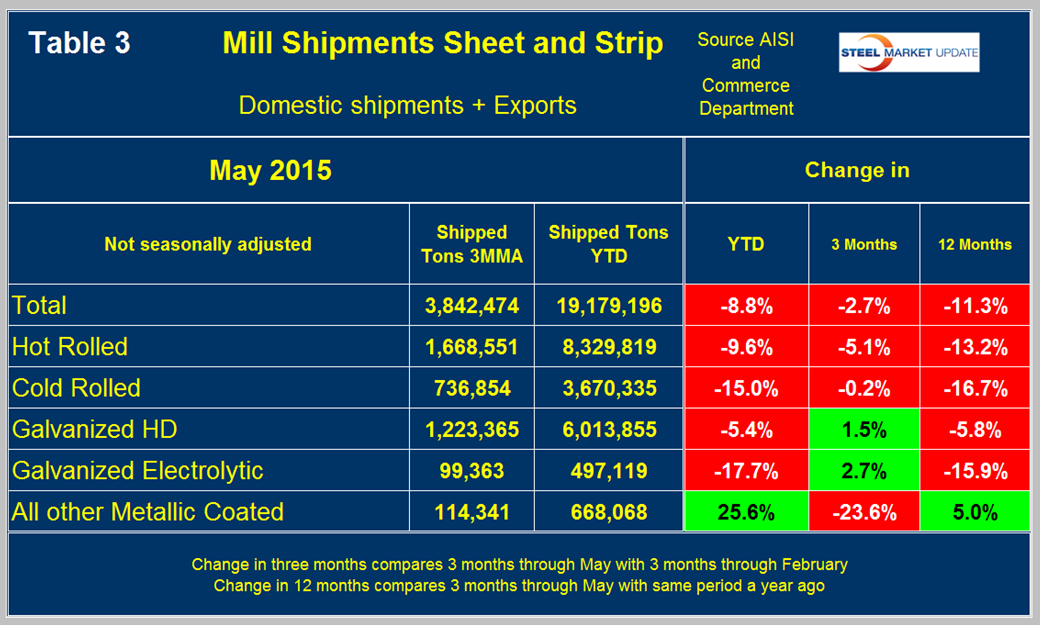

Mill Shipments: Table 3 shows that total shipments of sheet and strip products including hot rolled, cold rolled and all coated products were down by 8.8 percent YTD year over year and down by 2.7 percent in 3 months through May compared to 3 months through February.

Three months through May year over year was down by 11.3 percent. Hot rolled and cold rolled were down in all three time comparisons. Hot dipped and EG both strengthened in 3 months through May compared to 3 months through February. Other metallic coated was down by 23.6 percent in 3 months through May compared to 3 months through February, this was mainly because of an extremely strong shipment volume in January. Figure 3 shows the history of mill shipments since January 2008.

SMU Comment: Import market share is still exceptionally high, longs being even worse than sheet products. Year over year mill shipments are declining faster than apparent supply a differential that is driven directly by import market share.