Prices

August 18, 2015

SMU Price Ranges & Indices: Prices Weakening

Written by John Packard

Steel buyers are reporting a weakening steel market in both our phone conversations as well as through our survey responses. SMU reported a drop in hot rolled coil prices last week of $5 per ton and we are reporting an additional $5 per ton move lower this week.

We are seeing weakness in all products. In our HARDI steel conference call held earlier today, buyers of galvanized steel reported prices as being down by $20 per ton compared to just a few weeks ago. We are hearing from large service centers that the $440 per ton level for hot rolled is becoming a “normal” spot number when it was $460 to $480 per ton just a few weeks ago.

Steel buyers and industry executives are reporting most of the domestic mills as having short lead times and they are aggressively looking for business. Buyers do not expect prices to totally collapse but momentum is certainly not on the side of prices moving higher anytime soon. At the same time, many of the same buyers who are reporting weakness now, still believe there will be higher prices coming in the not too distant future due to the trade suits and potential labor issue at US Steel or ArcelorMittal (or both).

One service center executive told SMU this afternoon, “It’s really a bizarre market. Shipments are holding up and no one is buying steel.” He went on to explain to us that many of their end user customers loaded up on steel in late April and early May. Those stocks will get worked down and there will come a time when they will need to buy again. His prediction was for prices to begin to rise by October (late 4th Quarter to early 1st Quarter production).

Others are not so sure. “I think the post trade case analysis is yielding more and more to the observer a lack of demand than a case of oversupply. It won’t be surprising to see levels from US mills start trending lower again.”

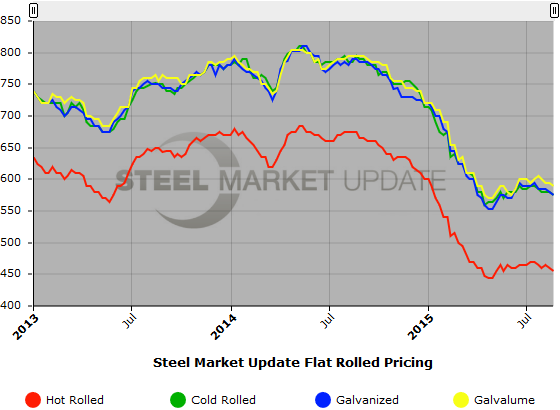

Here is how we see spot flat rolled prices this week (all prices shown are in net tons which are equal to 2,000 pounds):

Hot Rolled Coil: SMU Range is $430-$470 per ton ($21.50/cwt- $23.50/cwt) with an average of $450 per ton ($22.50/cwt) FOB mill, east of the Rockies. The lower end of our range dropped $10 per ton compared to last week as did the upper end of our range. Our overall average is down $10 per ton compared to one week ago. SMU price momentum for hot rolled steel is Neutral at the moment but we are seeing short term pockets of weakness which could take prices lower over the next couple of weeks.

Hot Rolled Lead Times: 2-5 weeks.

Cold Rolled Coil: SMU Range is $550-$600 per ton ($27.50/cwt- $30.00/cwt) with an average of $575 per ton ($28.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton from one week ago while the upper end remained unchanged. Our overall average is down $5 per ton compared to last week. SMU price momentum on cold rolled steel is at Neutral but, like hot rolled above, we could see a weakening in prices over the next two or three weeks.

Cold Rolled Lead Times: 4-8 weeks.

Galvanized Coil: SMU Base Price Range is $28.00/cwt-$29.50/cwt ($560-$590 per ton) with an average of $28.75/cwt ($575 per ton) FOB mill, east of the Rockies. The lower end of our range remained the same compared to last week while the upper end dropped $10 per ton. Our overall average is down $5 per ton compared to one week ago. Our price momentum on galvanized steel is Neutral with some pockets of short term weakness. There are a number of items that need to be watched regarding galvanized. These include the negotiations at US Steel and ArcelorMittal where GI lead times are “inquire,” automotive labor contract negotiations which come to a head in early October and input costs – especially for zinc which closed the day today at $0.80 per pound.

Galvanized .060” G90 Benchmark: SMU Range is $629-$659 per net ton with an average of $644 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-7 weeks.

Galvalume Coil: SMU Base Price Range is $28.50/cwt-$30.50/cwt ($570-$610 per ton) with an average of $29.50/cwt ($590 per ton) FOB mill, east of the Rockies. The lower end of our range declined $10 per ton over one week ago while the upper end remained the same. Our overall average is down $5 per ton compared to last week. Like the other flat rolled products mentioned above our price momentum for Galvalume is currently pointing towards Neutral but with a short term downward tilt.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU Range is $861-$901 per net ton with an average of $881 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-7 weeks.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.