Market Data

December 8, 2015

Steel Buyers Basics: Cost of Galvanized and Galvalume Steel Sheet Update 2

Written by Mario Briccetti

The following article was written by Mario Briccetti of Briccetti & Associates, a Supply Chain consulting firm, and is also one of our instructors for Steel 101 as well as our Sales Training Workshop.

Recently, in my series of articles, I have written about the coating cost of galvanized and Galvalume on flat rolled steel. These coatings are made from Zinc and Aluminum which are commodity metals whose price is subject to an open world-wide auction on the London Metal Exchange (LME).

![]() The ingot price for Aluminum and Zinc is published each day on the LME’s website and is expressed in $/metric ton. The price Steel Mills pay for their Aluminum and Zinc ingot is set by the LME’s price and with the addition of a separate premium price that is related to warehousing costs. The LME has just begun to publish Aluminum premiums (hopefully Zinc will soon be next). Interestingly US premiums for Aluminum are $200/tonne compared to $120 for Europe and $90 for Asia.

The ingot price for Aluminum and Zinc is published each day on the LME’s website and is expressed in $/metric ton. The price Steel Mills pay for their Aluminum and Zinc ingot is set by the LME’s price and with the addition of a separate premium price that is related to warehousing costs. The LME has just begun to publish Aluminum premiums (hopefully Zinc will soon be next). Interestingly US premiums for Aluminum are $200/tonne compared to $120 for Europe and $90 for Asia.

Since these prices have been so volatile (and many buyers are negotiating reduced coating costs based on the current low prices of these metals) I thought it would be a good time to update their effect on coating costs. To do that across a wide range of gauges, coating weights, coating types and mill practices as prices change I developed a spreadsheet to automate and track this calculation.

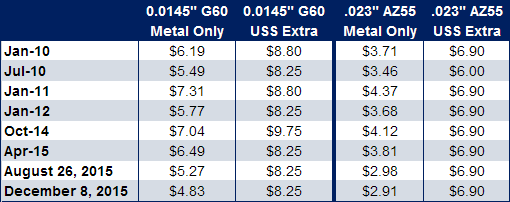

Here are the latest results, in $/cwt, for a typical galvanized and Galvalume gauge spec. compared to US Steel’s extras published in over time – the last being April 2015.

Since August galvanized is down 8.4 percent due to the continued fall in Zinc prices but Galvalume is down only 2.3 percent since Aluminum prices have been stable. (Both prices would be $0.25/cwt or $5/ton lower if the US premium was the same as Asia’s.) Both galvanized and Galvalume costs are down substantially from a year ago.

What’s important about this chart is that, on average, from Jan 2010 to April 2015 charged mill extras for 0.0145″ G60 are $2.30/cwt higher than ingot cost. Right now they are $3.42 higher. For 0.023″ AZ55 the average was $3.04 vs. today’s difference of $3.99. Currently, buyers who are negotiating these prices should know how what these differences are.

Coating costs are not the only interesting aspect of coated coil. Since Aluminum is much lighter than Zinc (and steel), pound for pound galvalume coil has more square feet in it – substantially more at thin gauges. Also the coating thickness, which drives lifetime in most (but not all) applications, of G90 is roughly equivalent to AZ55. So I developed my spreadsheet to report all these properties for Galvanized and Galvalume (and ZAM and Galfan). Please let me know (Mario@mbriccetti.com) if you have an interest.