Market Segment

June 20, 2016

Service Center Intake, Shipments and Inventory through May 2016

Written by Peter Wright

Based on Steel Market Update (SMU) analysis of the recently released MSCI service center inventory and shipment data, total service center carbon steel shipments decreased by 41,100 tons in May to 3.050 million tons. The number of shipping days was he same at 21. On a tons per day (t/d) basis shipments decreased from 147,200 in April to 145,200 tons in May.

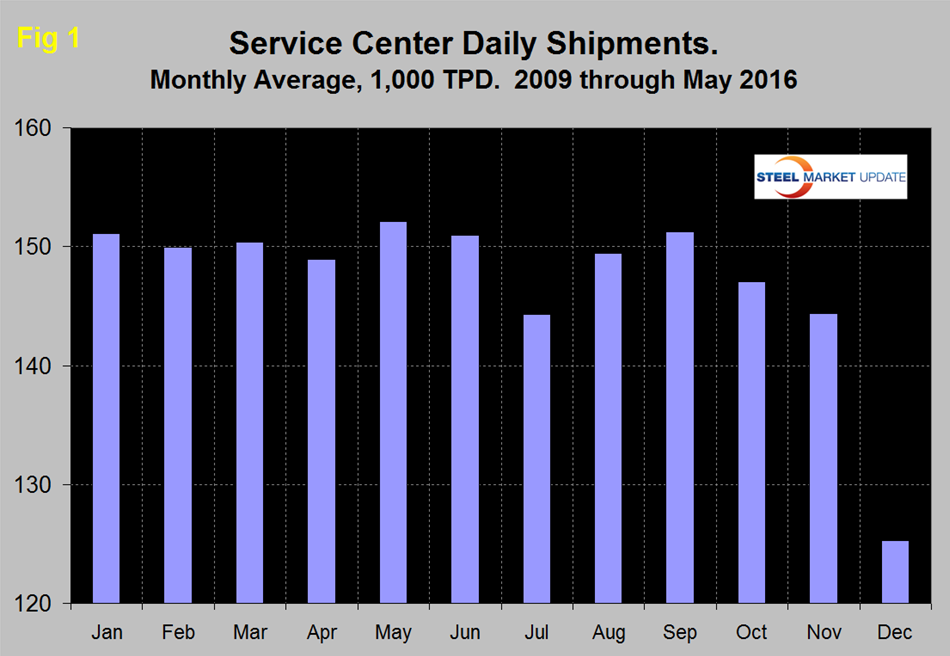

In the eight years since and including 2009, May shipments on average on a t/d basis have been up by 2.1 percent from April. This year shipments were down by 1.4 percent. Therefore on a long term basis (8 years) the May performance was disappointing. This observation is only intended to give a long term perspective because MSCI data is quite seasonal and we need to get past that before commenting in detail on current results. Figure 1 demonstrates this seasonality and why comparing a month’s performance with the previous month is usually misleading.

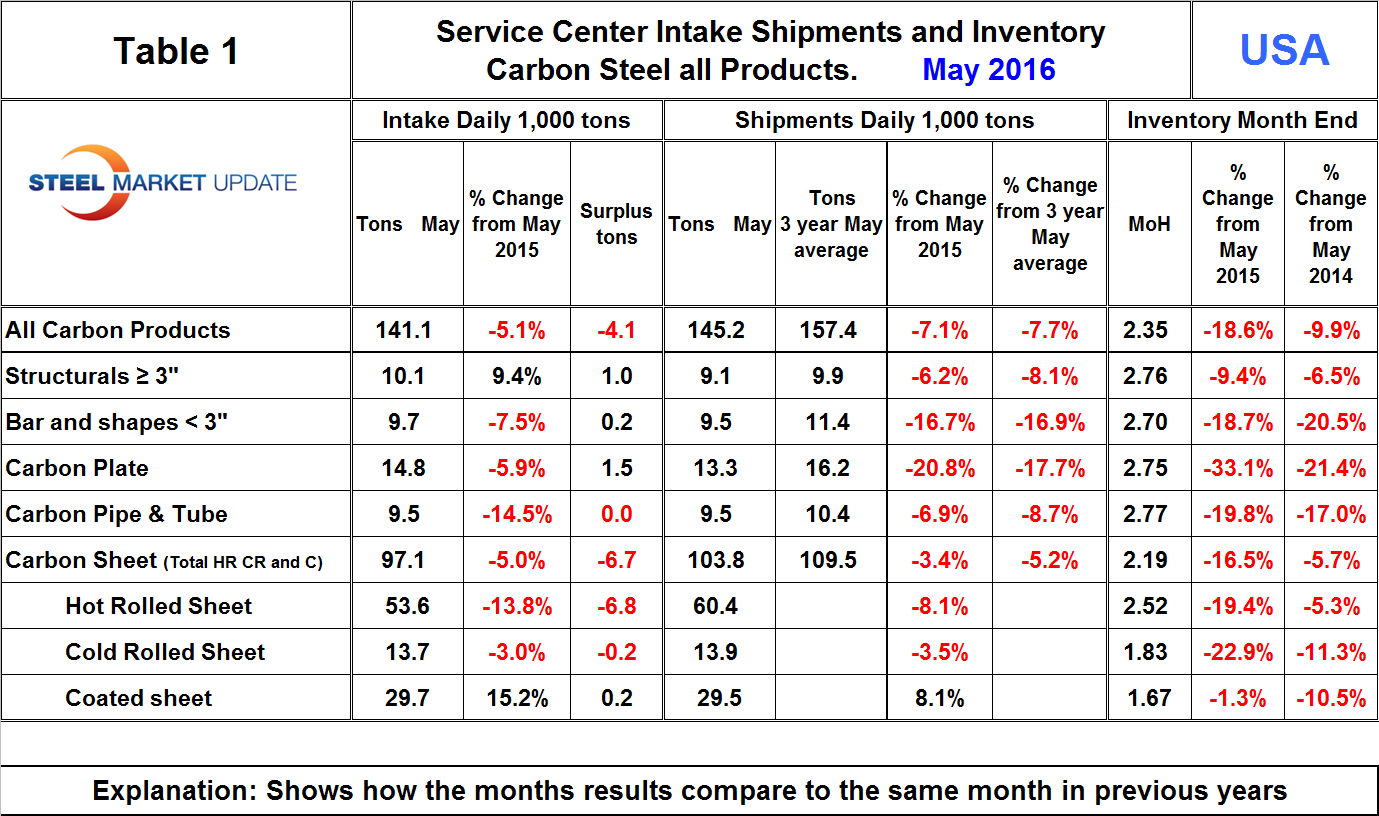

In the SMU analysis we always consider year over year changes to eliminate this seasonality. Table 1 shows the performance by product in May compared to the same month last year and also with the average t/d shipments for May in the last three years.

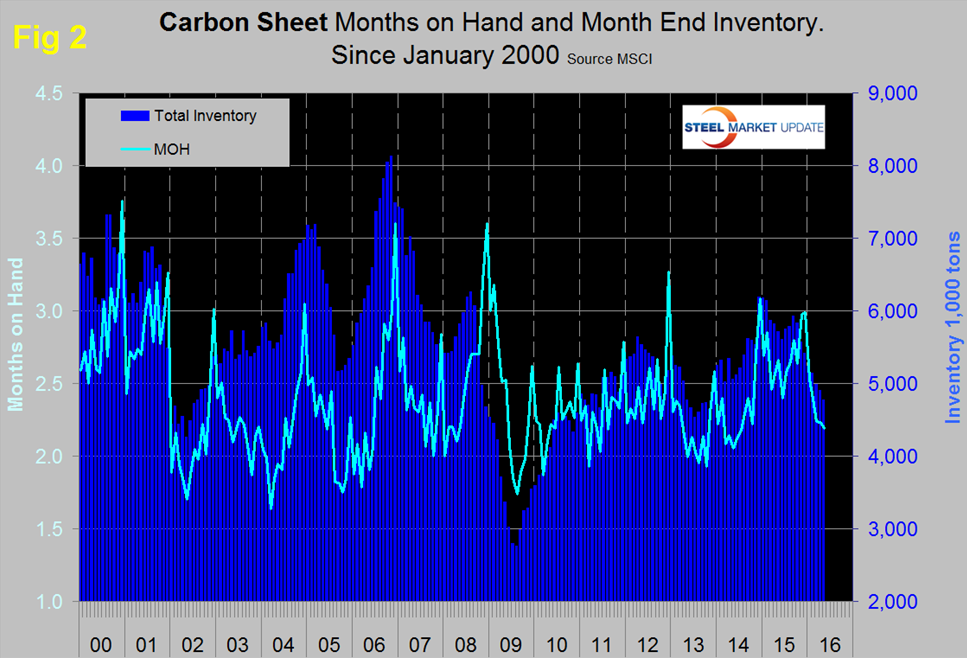

We then calculate the percent change between May 2016 and May 2015 and with the 3 year May average. Our intention is to provide an undistorted view of market direction. In May, intake at 141,100 t/d was 4,100 tons less than shipments. This was the eighth month of deficit after three months of surplus. Total sheet products had a deficit of 6,700 tons and intake was down by 5.0 percent y/y. Figure 2 shows both the inventory and months on hand, monthly since January 2000 for total sheet products.

Total sheet inventory has been in a steady decline since September last year with a total reduction since then of 1.161 million tons. Months on hand have declined from 2.99 in December last year to 2.19 in May.

In December 2015 the MSCI expanded their data to include sub sets of the major product groups and provided two years of data for 2014 and 2015. Table 1 shows the breakdown of sheet products into hot rolled, cold rolled and coated products. The intake deficit was evident for all sheet products except cold rolled which eked out a small surplus. Long products and plate had an intake surplus. Compared to May 2015, intake was down by 5.1 percent for all carbon steel products but the intake of coated sheet products continued to increase for the fourth consecutive month. Intake of hot rolled was down by 13.8 percent and of cold rolled by 3.0 percent y/y.

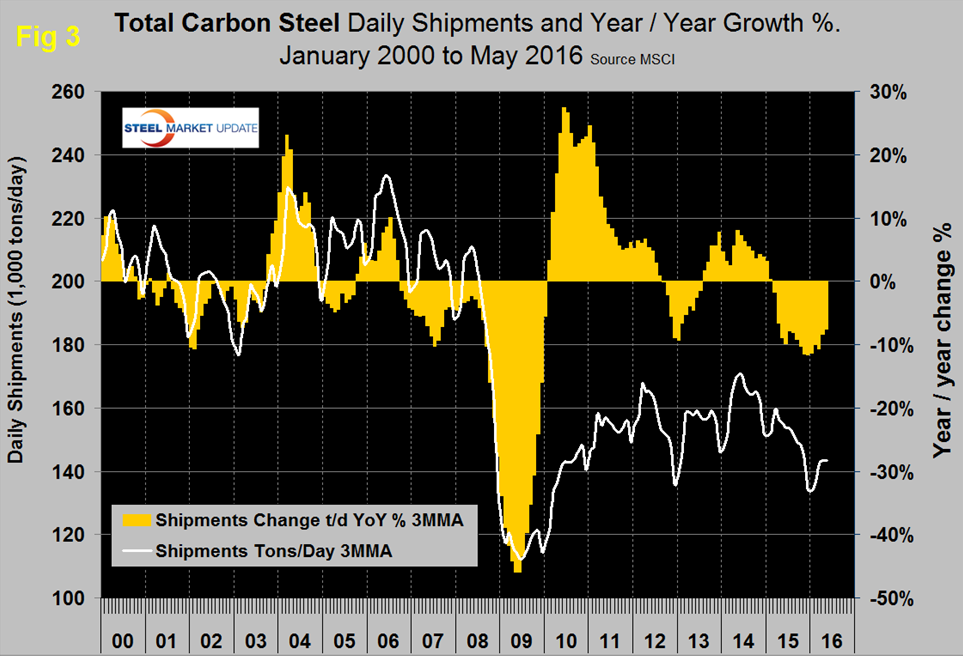

Shipments of all carbon steel products in May on a t/d basis were down by 7.1 percent y/y and were 7.7 percent less than the average May shipments for 2016, 2015 and 2014. The fact that the single month y/y growth comparison is similar to the three year comparison suggests that momentum is neutral with no significant improvement in sight. Figure 3 shows the long term trends of daily carbon steel shipments since 2000 as three month moving averages. In our opinion the quickest way to size up the market is the orange bars in Figures 3, 6, 7 and 9 which show the y/y change in shipments; all four of these graphs show a y/y contraction.

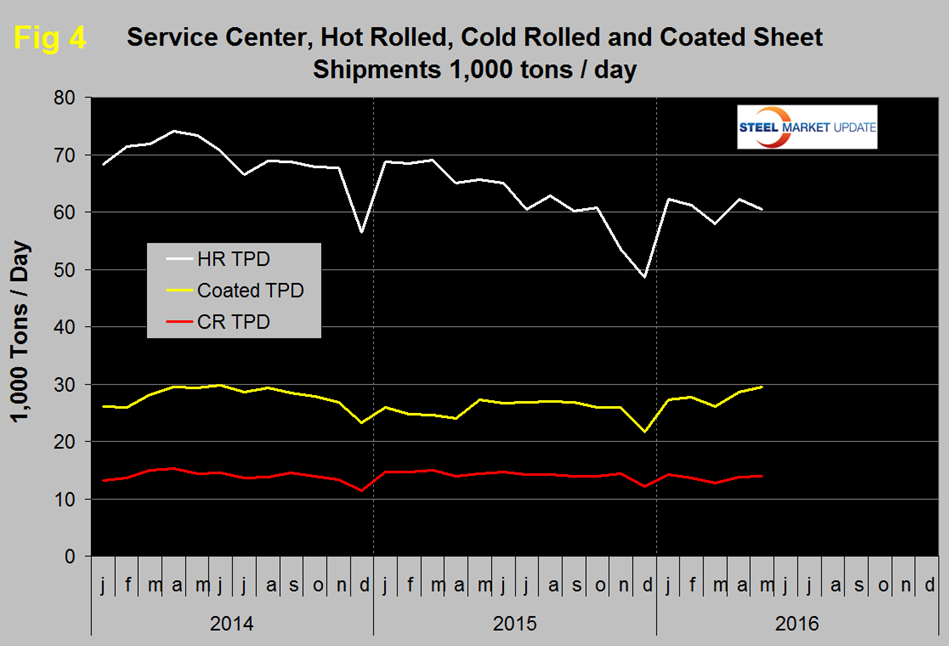

Total daily shipments had a post recessionary high of 173,300 in May 2014 and as shown by the brown bars in Figure 3 have had 15 consecutive months of negative y/y growth. In May shipments of all products except coated sheet were down year over year. Sheet products in total were down by 3.4 percent led by hot rolled down by 8.1 percent. Figure 4 shows the historical shipping rate of the three major sheet products since January 2014. Coated products enjoyed the highest shipments since mid-2014, hot and cold rolled have made no progress this year.

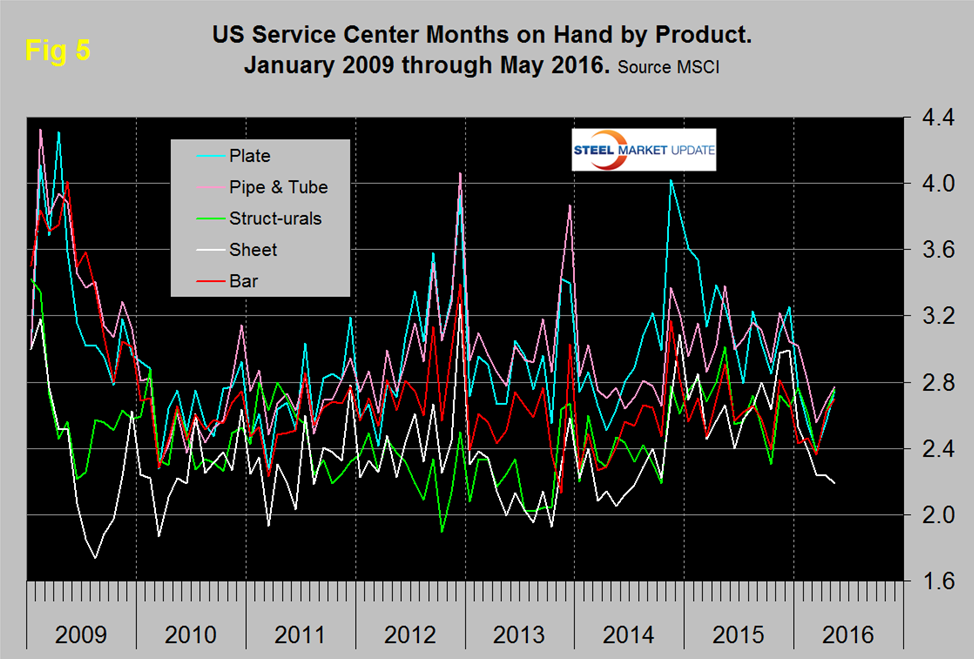

May closed with months on hand (MoH) of 2.35, almost exactly the same as April. All products except structurals and coated sheet had a double digit y/y decrease in MoH and plate was down by 33.1 percent. Figure 5 shows the MoH by product monthly since January 2009. Sheet products have by far the lowest inventory as all other product groups have converged at about 2.7 months.

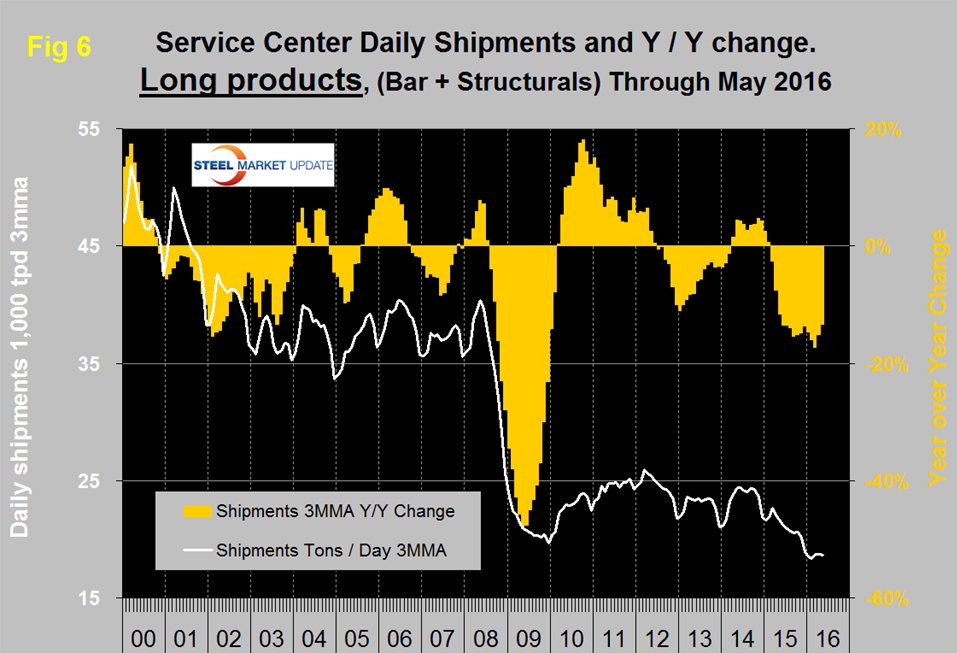

There continues to be a wide difference between the performances of flat rolled (sheet + plate) and long products (structurals + bar) at the service center level. Long product shipments from service centers are now lower than they were at the depths of the recession which as we have reported previously makes no sense to us unless there has been a mass migration of buyers direct to the mills. Alternatively the numbers are just wrong because of gaps in company participation (Figure 6).

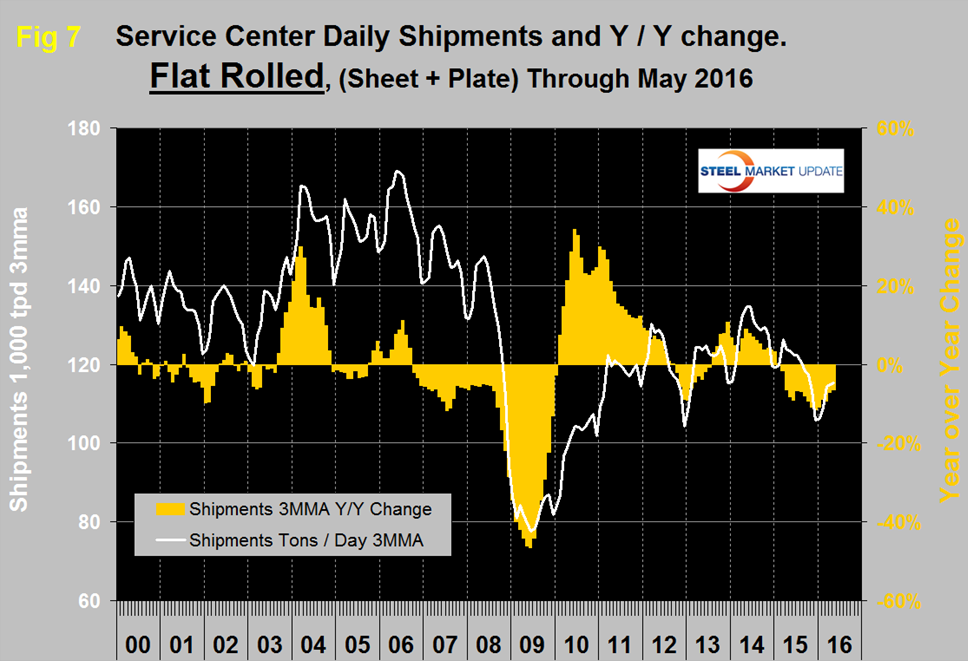

Considering the improving construction statistics, we have no explanation for this dismal long product performance. Flat rolled has had a much better recovery since mid-2009 and had positive y/y growth for 18 straight months through January 2015. In February 2015 growth slowed to zero and has been negative ever since (Figure 7).

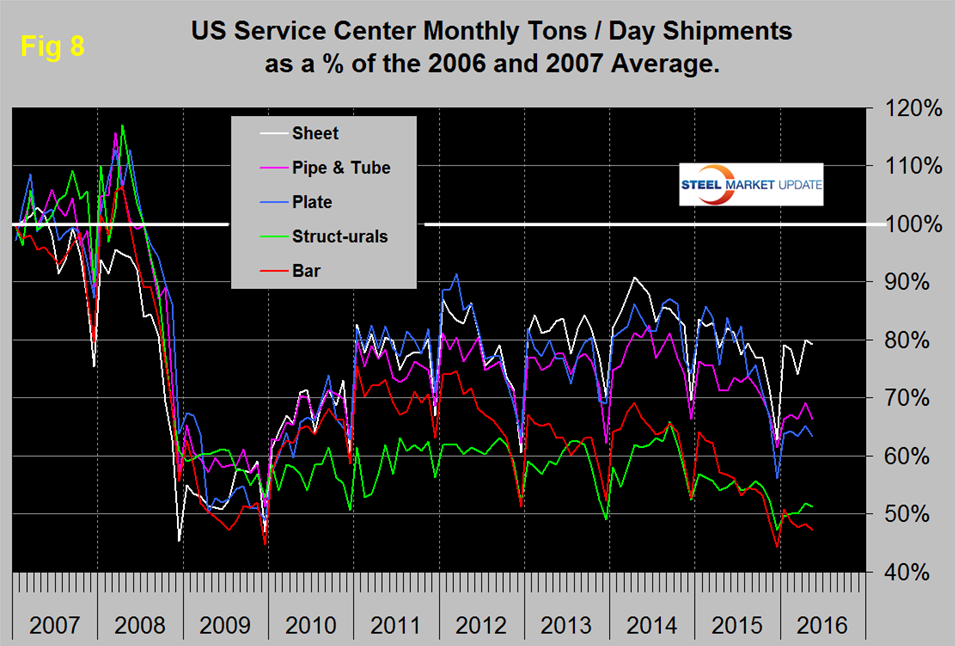

In 2006 and 2007, the mills and service centers were operating at maximum capacity. Figure 8 takes the shipments by product since that time frame and indexes them to the average for 2006 and 2007 in order to measure the extent to which service center shipments of each product have recovered.

All products experienced the normal end of year collapse and January pick up. The total of carbon steel products is now at 68.4 percent of the shipping rate that existed in 2006 and 2007, with structurals and bar at 51.3 percent and 47.3 percent respectively. Sheet is at 79.3 percent, plate at 63.3 percent and tubulars at 66.4 percent.

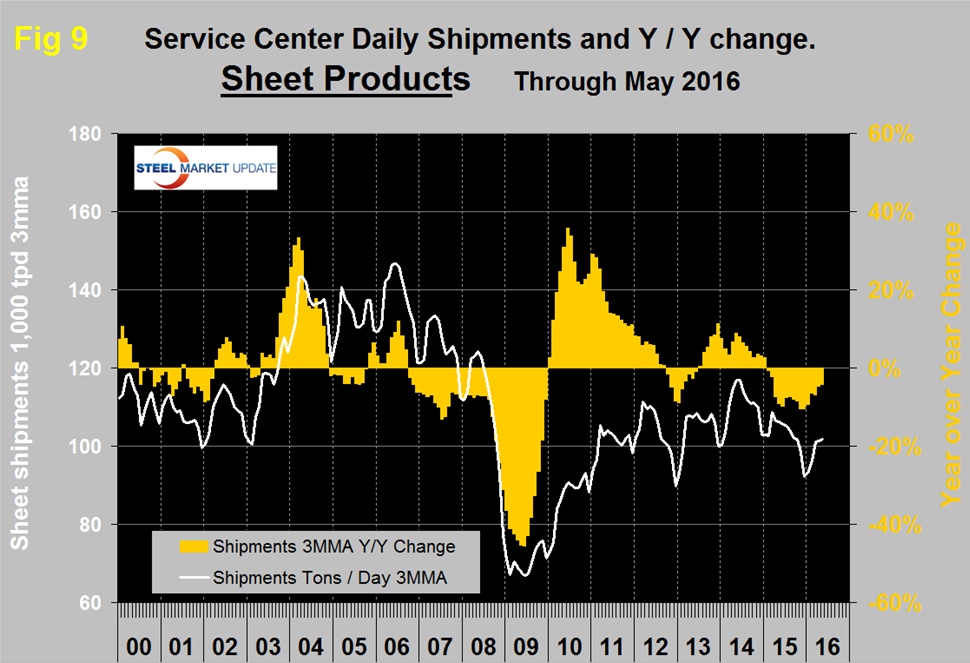

MSCI uses product nomenclature flat and plate. In this analysis at SMU we replace the term flat with sheet. MSCI’s definition of “flat” is all hot rolled, cold rolled and coated sheet products. Since most of our readers are sheet oriented we have removed plate from Figure 7 to highlight the history of sheet products which are shown in Figure 9.

Following the strong post-recession recovery, sheet products experienced 9 months of decline from October 2012 through June 2013. This was followed by 19 months of growth through December 2015 but January 2015 slipped back into negative territory at -0.7 percent year over year and has been negative ever since with a 6.6 percent contraction in May 2016.

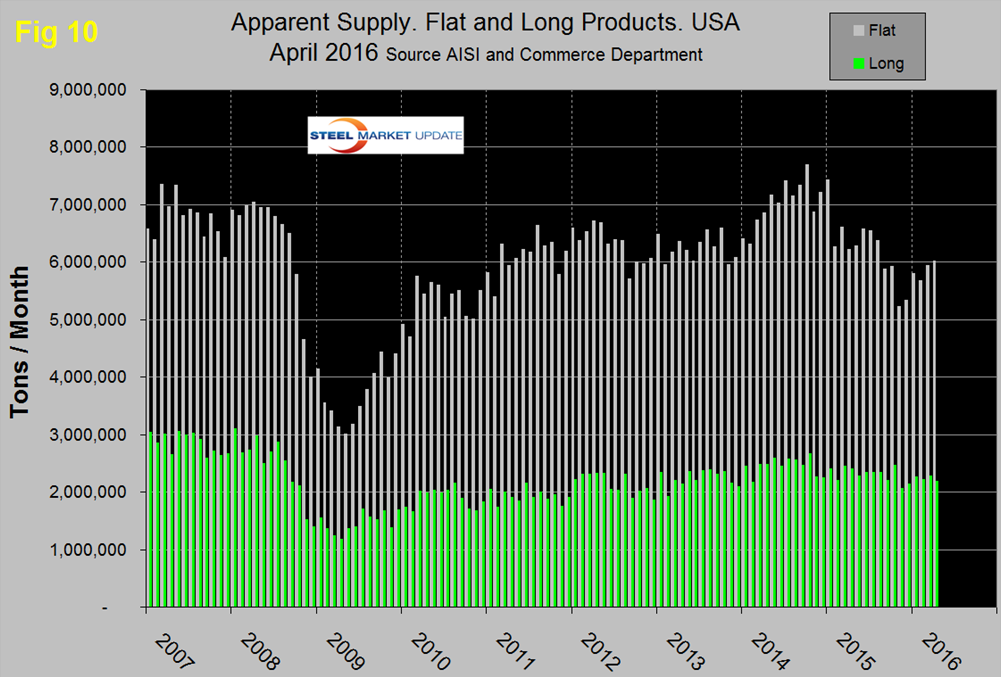

SMU Comment: In Figures 3, 6, 7 and 9, the white lines show t/d shipments. There was a distinct decline in shipments for all major product groups in 2015 on a y/y basis with a partial recovery of flat rolled sheet and plate this year. Figure 10 shows the total supply to the market of long and flat products based on AISI shipment and import data.

Total supply of long products is much better than the MSCI report of service center shipments with a volume almost double the recessionary low point. Total supply of flat rolled products peaked in October 2014, dropped sharply in May 2015 then through August didn’t change much. However in November supply was the lowest since May 2010. There has been an uptick in total flat rolled supply this year but compared to this time last year volumes are still depressed. For flat rolled the MSCI and AISI data are in reasonable agreement with one another. Note: this supply data is one month behind the MSCI information.

The SMU data base contains many more product specific charts than can be shown in this brief review. For each product we have ten year charts for shipments, intake, inventory tonnage and months on hand. Some readers have requested these extra charts for a particular product and others are welcome to do so.