Market Data

December 4, 2016

November Consumer Confidence Report Was Excellent

Written by Peter Wright

The source of this data is the Conference Board with analysis by Steel Market Update. This article is normally reserved for our Premium level members but we are sharing it with all of our readers in an effort to give you some taste of what kind of analysis you get with a Premium membership to Steel Market Update. Please see the end of this piece for an explanation of the indicator.

The November report was excellent. Consumer confidence is the driver of consumer spending which is the largest component of GDP and which ultimately drives a large portion of steel consumption.

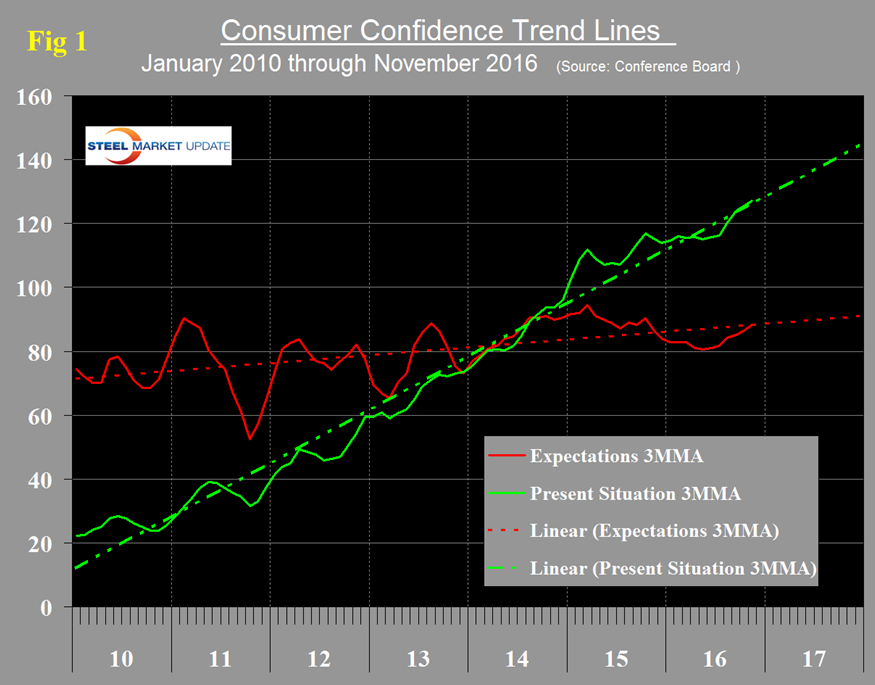

The low point for consumer confidence this year was May with a value of 92.4, its lowest value since July last year. Confidence increased to 103.5 in September, declined to 100.8 in October and shot up to 107.1 in November, its highest value since July 2007. Included below is the official news release from the Conference Board. The three month moving average (3MMA) has risen for six consecutive months from 94.4 in May to 103.8 in November. We prefer to smooth the data in this way because of monthly volatility which in the case of consumer confidence has been quite extreme since the beginning of last year. The composite index is made up of two sub-indexes. These are the consumer’s view of the present situation and his/her expectations for the future. The 3MMA of both components are now back to their six year trend lines (Figure 1).

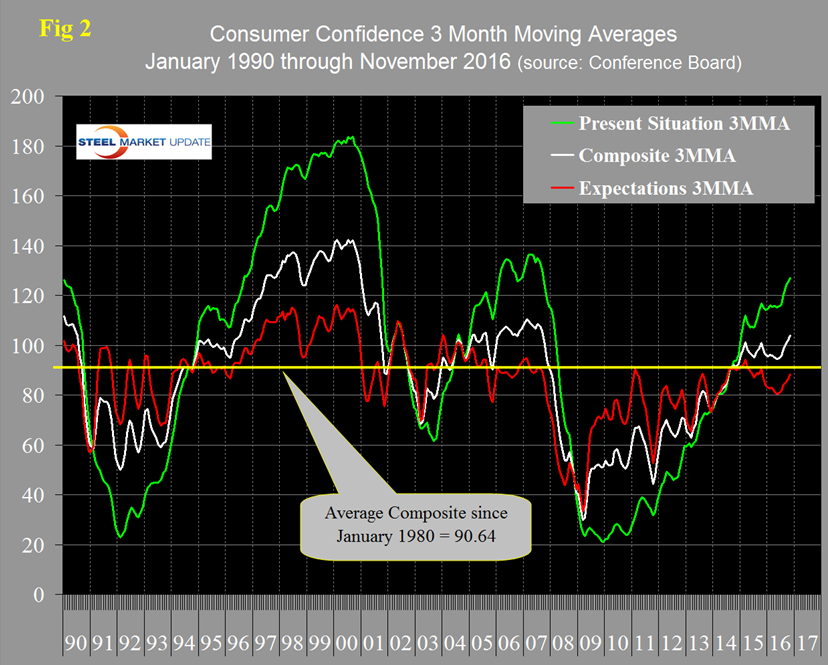

The historical pattern of the 3MMA of the composite, the view of the present situation and expectations are shown in Figure 2.

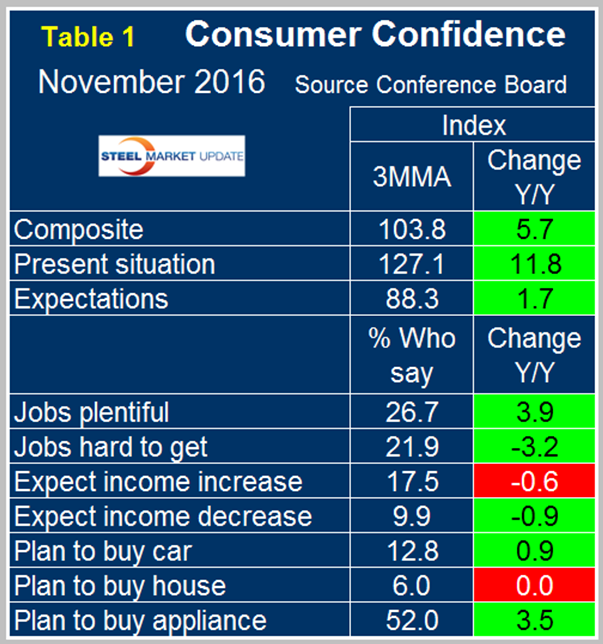

The progression of the 3MMA of the composite was positive throughout 2014 into early 2015 and then lacked direction for 15 months before the surge of the last six months. The pattern of the present situation and expectations that developed in the late 90s and mid-2000s is now well established as shown in Figure 2. Comparing November 2016 with November 2015 (y/y) the 3MMA of the composite was up by 5.7, the present situation was up by 11.8 and expectations were up by 1.7 (Table 1).

This was the first time for the 3MMA of expectations to have positive growth after 16 straight months of the opposite. The consumer confidence report includes data on job availability and wage expectations. It reports on the proportion of people who find that jobs are hard to get and those who believe jobs are plentiful and it measures those who expect a wage increase or a decrease. Since August 2011 both of the job availability components have steadily improved. Expectations for wage increases have not been as consistent. Plans to buy homes have been positive y/y in 16 of the last 18 months. Plans to buy appliances have been positive for 9 of the last 11 months. Plans to buy a car have been positive y/y for 7 of the last 8 months.

SMU Comment: Consumer confidence is positively correlated with personal consumption which accounts for about 2/3 of GDP. Ultimately a positive growth of GDP has a positive effect on steel consumption therefore the overall November improvement is very welcome.

The official news release from the Conference Board reads as follows and is entirely based on monthly changes. This is a highly regarded indicator which we believe needs to be examined in a longer time context to get the true picture which is why we only consider three month moving averages and focus our comments on year over year results.

The Conference Board Consumer Confidence Index Rebounds Strongly in November

“Consumer confidence improved in November after a moderate decline in October, and is once again at pre-recession levels,” said Lynn Franco, Director of Economic Indicators at The Conference Board. (The Index stood at 111.9 in July 2007.) “A more favorable assessment of current conditions coupled with a more optimistic short-term outlook helped boost confidence. And while the majority of consumers were surveyed before the presidential election, it appears from the small sample of post-election responses that consumers’ optimism was not impacted by the outcome. With the holiday season upon us, a more confident consumer should be welcome news for retailers.”

Consumers’ assessment of current conditions improved in November. The percentage saying business conditions are “good” improved from 26.5 percent to 29.2 percent, while those saying business conditions are “bad” fell from 17.3 percent to 14.8 percent. Consumers’ appraisal of the labor market was moderately more positive than last month. The percentage of consumers stating jobs are “plentiful” increased from 25.3 percent to 26.9 percent, while those claiming jobs are “hard to get” was unchanged at 21.7 percent.

Consumers’ short-term outlook, on balance, was more optimistic in November. The percentage of consumers expecting business conditions to improve over the next six months fell from 16.4 percent to 15.3 percent; however those expecting business conditions to worsen also decreased, from 11.8 percent to 10.0 percent. Consumers’ outlook for the labor market was likewise somewhat mixed. The proportion expecting more jobs in the months ahead was virtually unchanged at 14.5 percent, but those anticipating fewer jobs fell from 16.6 percent to 13.8 percent. The percentage of consumers expecting their incomes to increase—17.5 percent—was little changed from last month, while the proportion expecting a drop in income fell moderately, from 10.2 percent to 9.0 percent.

About The Conference Board: The Conference Board is a global, independent business membership and research association working in the public interest. Our mission is unique: To provide the world’s leading organizations with the practical knowledge they need to improve their performance and better serve society. The monthly Consumer Confidence Survey, based on a probability-design random sample, is conducted for The Conference Board by Nielsen, a leading global provider of information and analytics around what consumers buy and watch. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months. The Conference Board is a non-advocacy, not-for-profit entity holding 501 (c) (3) tax-exempt status in the United States. www.conference-board.org.