Market Data

February 24, 2017

Currency Update for Steel Trading Nations

Written by Peter Wright

Please see the end of this report for an explanation of data sources.

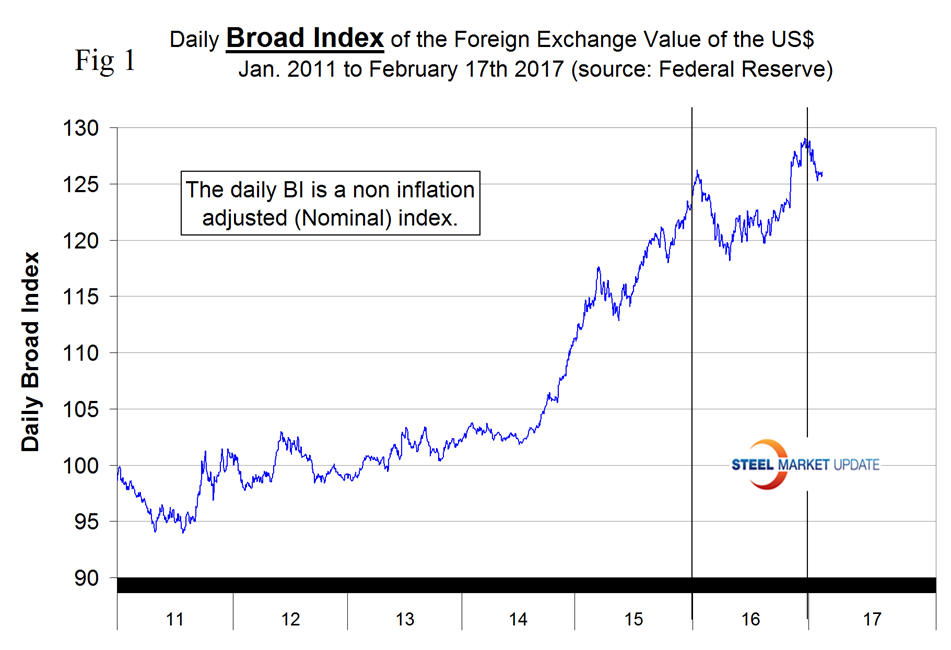

The Broad Index value of the US $ is reported several days in arrears by the Federal Reserve, the latest value published was dated February 17th (Figure 1).

The dollar had a recent peak of 128.963 on January 3rd which was the highest value since April 4th 2004, almost 15 years. The escalation was driven by the Fed’s increase in its target short-term interest rate on the 14th of December to 50 – 75 basis points. Traders look for and anticipate interest rate differentials. Based on the hawkish pronouncements of the Fed, the interest rate spread between the dollar and the Euro and the Yen could be 1.75 percent or more by this time next year. Since January 3rd the dollar has weakened to 126.045 a decline of 2.3 percent. On Tuesday, Janet Yellen said it would be “unwise” to wait too long to hike rates, adding that the March meeting is “alive” in terms of a rate hike probability as well as any other meeting this year. The FedWatch tool of CME Group has shown a tangible shift in expectations as the previous week ended with an 82.3 percent chance of the March meeting being a non-event, and the odds fell to 69 percent by Thursday.

From Andrew Hecht on February 21st: Last week the dollar moved higher, and as I wrote in my recent article, there are so many reasons that the greenback will continue higher over the weeks and months ahead. The dollar is the reserve currency of the world. The wealth and power of the nation are reasons enough for a strong currency but it is the current level of interest rate differentials between the U.S. currency and other major world currencies that provide the support and will eventually lead to an upward trajectory for the dollar. The dollar offers the potential for capital appreciation and pays holders a superior rate of return while they wait. On Wednesday, as Chairperson Yellen was testifying before Congress, Eric Rosengren the Governor of the Federal Reserve Bank of Boston said that he expects “at least three interest rate hikes in 2017. With the rising potential for three hikes to fight inflation which appears to be heating up when one looks at the current trends of commodity prices, the interest rate gulf between the greenback and other currencies could propel the dollar to a new high. Chairperson Yellen cautioned on inflation in her comments to Congress and her colleague Governor Rosengren lit a fuse for the dollar. The likelihood is that we will hear more hawkish comments from other voting members of the FOMC in the days ahead if they intend to act in March to “fight” rising inflation. After all, if the inflation rate “will” rise to the 2 percent target rate it is not likely to stop there.

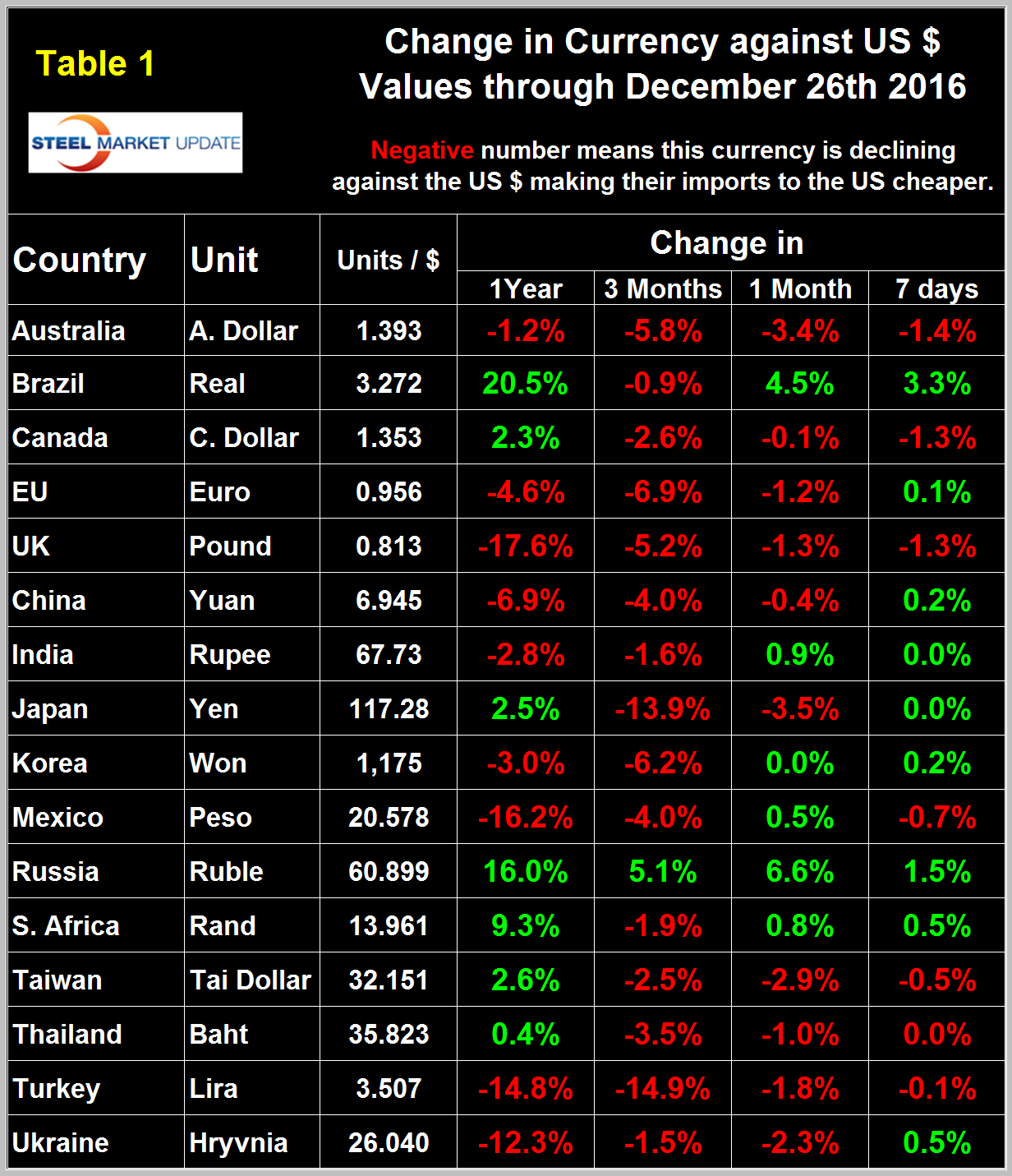

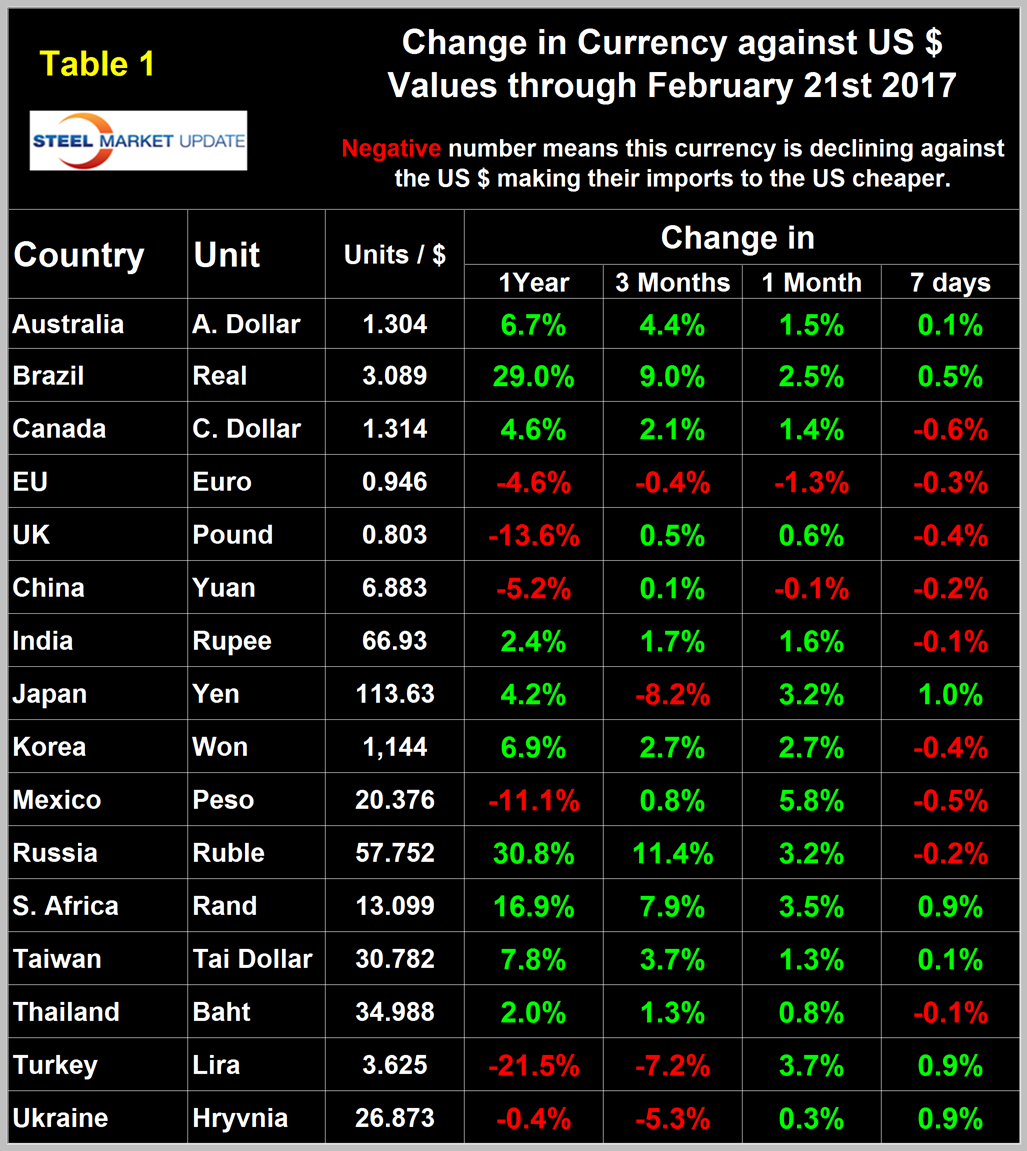

To illustrate the volatility of the currencies of the steel trading nations we at SMU have included in this report, two versions of Table 1, each of which shows the value of the US $ measured in the currencies of 16 steel and iron ore trading nations. It reports the changes in one year, three months, one month and seven days for each currency and is color coded to indicate strengthening of the dollar in red and weakening in green. We regard strengthening of the US Dollar as negative and weakening as positive because the effect on net imports. The December 26th version of Table 1 has the $ strengthening against 15 of the 16 currencies at the 3 month level.

Since then a major reversal has occurred. Table 1 version February 21st has the dollar weakening against 12 of the 16 at the 3 month level and against 14 of the 16 at the one month level.

There may be signs of another reversal to the upside at the 7 day level where the dollar strengthened against 9 of the 16. This seems to illustrate major uncertainty on the part of traders who are whipsawed by comments from both the Fed and our leading politicians. In each of these reports we comment on a few of the 16 steel trading currencies listed in Table 1. Charts for each of the 16 currencies are available through February 21st for any premium subscriber who requests them. We also include writings from experts who we regard as credible to explain some of the currency moves that we are living through.

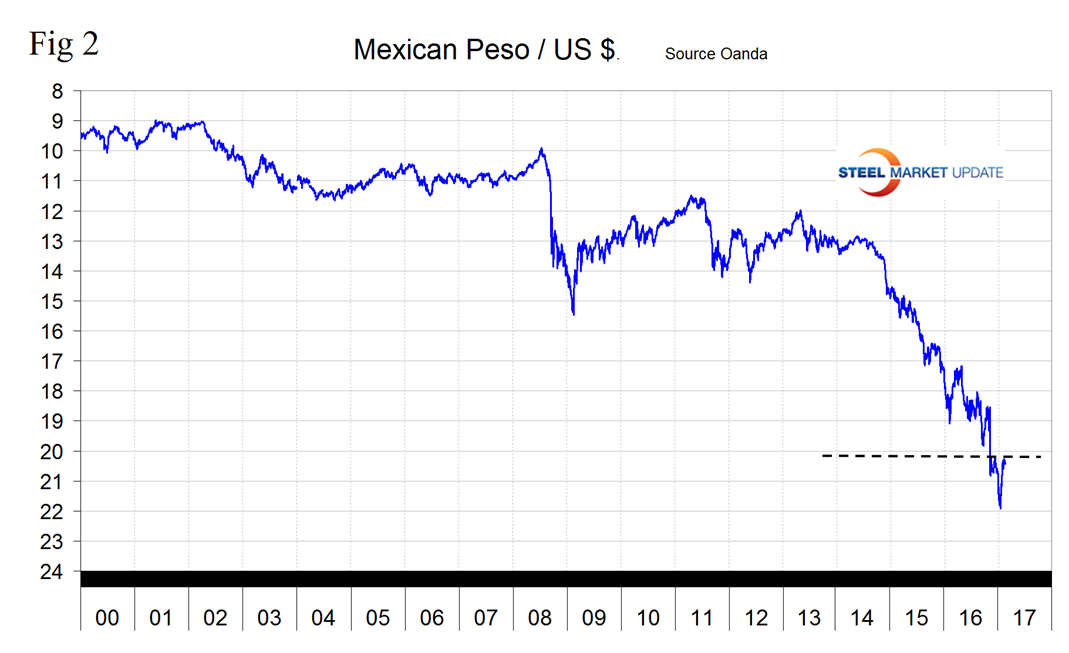

The Mexican Peso

Two days after the US election the peso broke through the 20/US $ level for the first time ever and continued to decline until January 19th when it reached 21.9211/US $. Since then the peso has recovered to reach 20.3762/$ on February 21st (Figure 2.)

The Peso has declined by 11.1 percent in the last twelve months but has recovered by 5.8 in the last month. On January 1st 1994, when the NAFTA was initiated it took only 3.5 pesos to buy one US dollar.

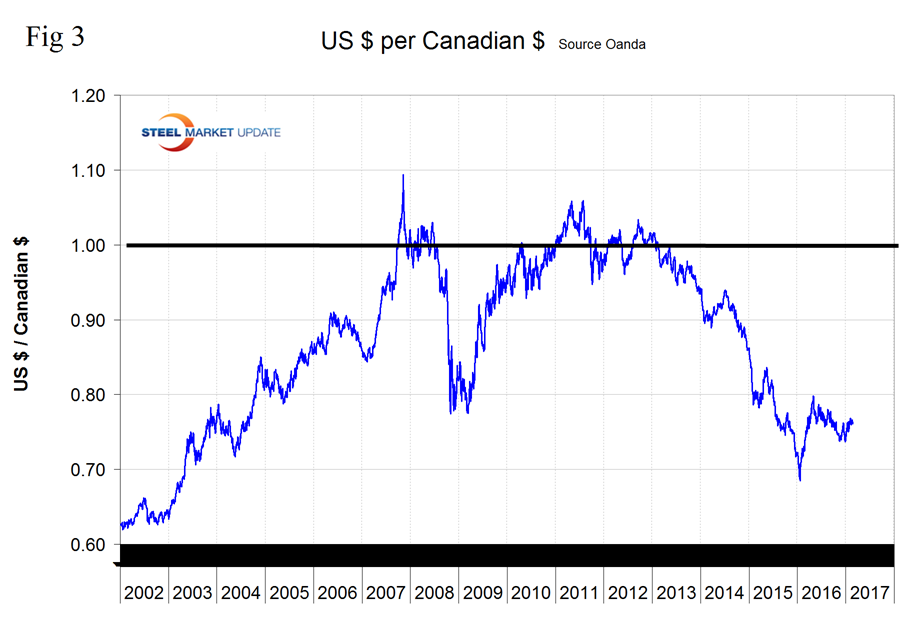

The Canadian Dollar

From Macro Investing, February 21st. Much like the rest of the world’s currencies, the Canadian dollar was directly impacted by Donald Trump’s victory in the U.S. election. During his campaign, Trump talked up his plans to make America great again with a trillion-dollar splurge on infrastructure projects, a cut to the corporate tax rate, and a tariff on foreign goods. Doing so would almost certainly cause inflation to rise rapidly, resulting in at least three rate hikes by the Federal Reserve in 2017, in our opinion. This is because if Trump does follow through on his infrastructure plans as we think he will, then it will almost certainly be funded through debt. By bringing more money into circulation, this will lead to general prices going up due to there being more money chasing the same quantity of goods. This in turn leads to inflation rising. Furthermore, we believe a tariff on foreign goods is likely to result in further price increases, once again causing inflation to rise.. As we mentioned earlier, the inflation that these policies generate is likely to require several rate hikes by the Federal Reserve, possibly as soon as next month. Especially after U.S. Federal Reserve Chair Janet Yellen said last week, it may be appropriate for the central bank to raise interest rates sooner rather than later as “waiting too long to remove accommodation would be unwise, potentially requiring the FOMC to eventually raise rates rapidly, which could risk disrupting financial markets and pushing the economy into recession.”

At present, the market has only priced in a 26.2 percent probability of three rate hikes in 2017, according to CME Group. Once the market starts to price in three rate hikes in 2017, we expect the U.S. dollar to surge higher against all major currencies due to the potential yield differentials. We expect the loonie will fall to the $0.72 level it tested at the start of 2016. This is approximately 5.2 percent lower than the current exchange rate.

The Canadian $ has risen 2.1 percent in the last 3 months and 1.4 percent in the last month. Figure 3.

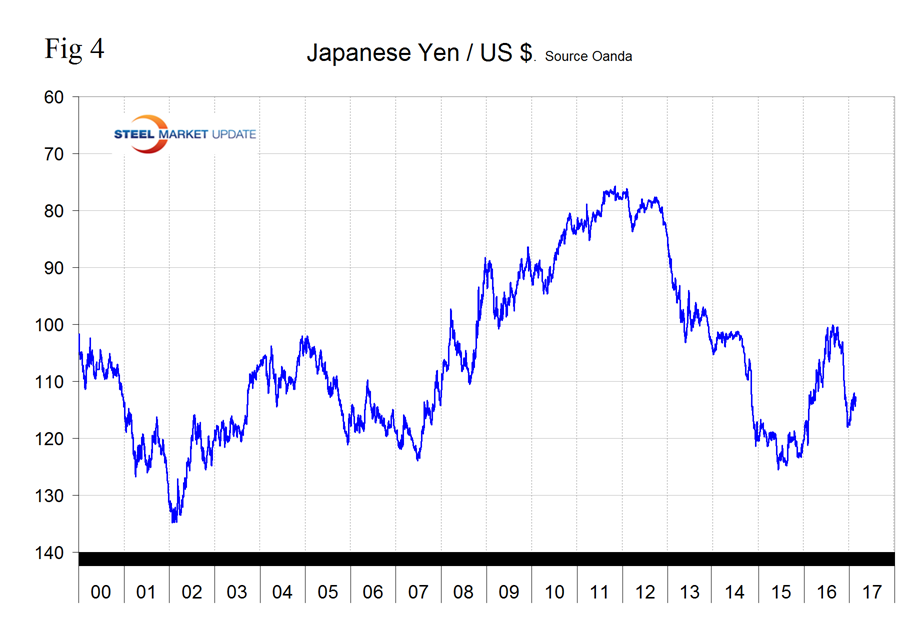

The Japanese Yen

From Dean Popplewell, February 22nd. I think we see a classic case of pre-Fed Speak and FOMC minutes jitters. We saw this play out before with recent USD bull runs running into serious resistance at the 114.50-115/Yen/US $ zone. Some traders are heading for the outside chance the Feds will wax hawkish. However, if history tells us anything about this sitting Fed, they are more likely to obfuscate than flip the rate hike switch early. While the Fed is grabbing headlines this week, EU politics are still a major play, and the threat of a French election risk aversion will likely cap USD/JPY topside momentum in the absence of any definitive economic policy moves from the US administration.

The Yen has declined by 2.3 percent in the last 3 months but recovered by 0.9 percent in the last month, Figure 4.

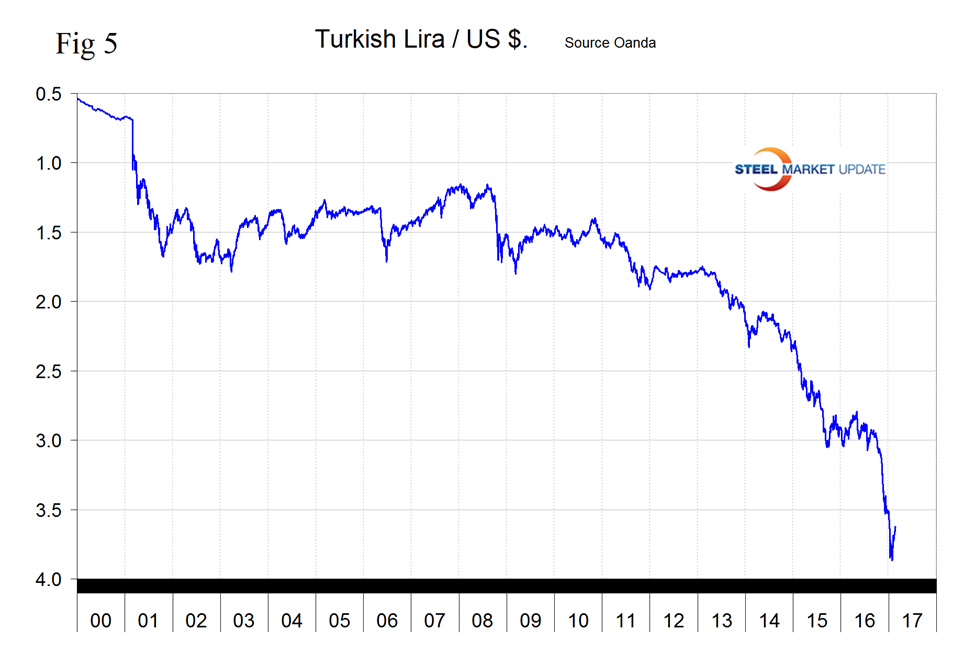

The Turkish Lira

The Turkish Lira was in free fall since September last year until it bottomed out at 3.869 on January 27th. Since then it had recovered to 3.625 on February 21st. The Lira is down by 21.5 percent in one year but has recovered by 3.7 percent in the last month, Figure 5.

ON Feb 3rd 2017 the IMF reported in their Article IV Consultation-Press Release: Staff Report: and Statement by the Executive Director for Turkey. “After robust growth through Q1 2016, the expansion has slowed. Growth is projected at 2.7 percent in 2016 and 2.9 percent in 2017 with considerable downward risks. Domestic consumption is the main growth driver, supported by a large increase in public expenditure and a hike in the minimum wage. However, political uncertainty, weakened corporate profitability, anemic credit growth, and a sharp fall in tourism have taken a toll on investment and net exports. The monetary stance and macro prudential measures were loosened, but credit growth continues to slow. A negative output gap is opening, but sticky expectations are keeping inflation above target. External imbalances persist: the current account deficit remains large and the NIIP is projected to become more negative. External financing conditions were favorable in the first semester, helping the rollover of large financing needs and supporting the Lira. However, political uncertainty after the failed coup attempt and a less favorable external environment are weakening the Lira and increasing the cost of external financing.”

Reading between the lines of this IMF report we see more pressure to increase steel exports in 2017.

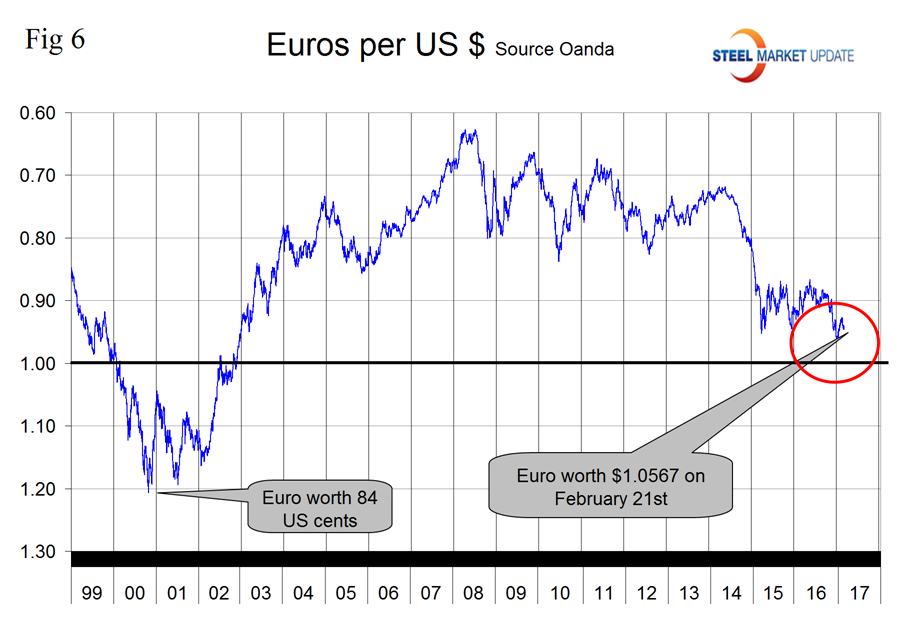

The Euro

Andrew Hecht wrote on February 21st. When it comes to the euro, the pan-European currency that is less than twenty years old, the chances are that we will see a continued deterioration over the course of 2017. Meanwhile, the dollar index traded to the highest level since 2002 in early January and then corrected lower. The dollar had been making higher lows and higher highs since May 2014 and it appears that the latest correction has ended with yet another higher low.

John Mason wrote on February 22nd. Of course, all bets are off the table if Ms. Le Pen or other major candidates in Europe win the elections. If this were to happen, the European Union, it appears, would be history as we know it now. The value of the US dollar against the Euro should strengthen significantly further. If no “populist” party in Europe wins, the value of the dollar would stay, I believe, around $1.05, if not a little lower, but then we would have to re-evaluate the whole situation. It still seems to me that Europe remains much weaker than the United States and that the European Union has cracks in it that need to be closed with a political union and other reforms that members have been reluctant or unable to put into place. These alone will continue to keep the currency on the weak side relative to the dollar. Again, I think if President Trump attempts to weaken the dollar within this framework he would only be causing a currency war and it would not be good for others, or for the United States.

The Euro has declined by 4.6 percent in the last twelve months and by 1.3 percent in the last month (Figure 6).

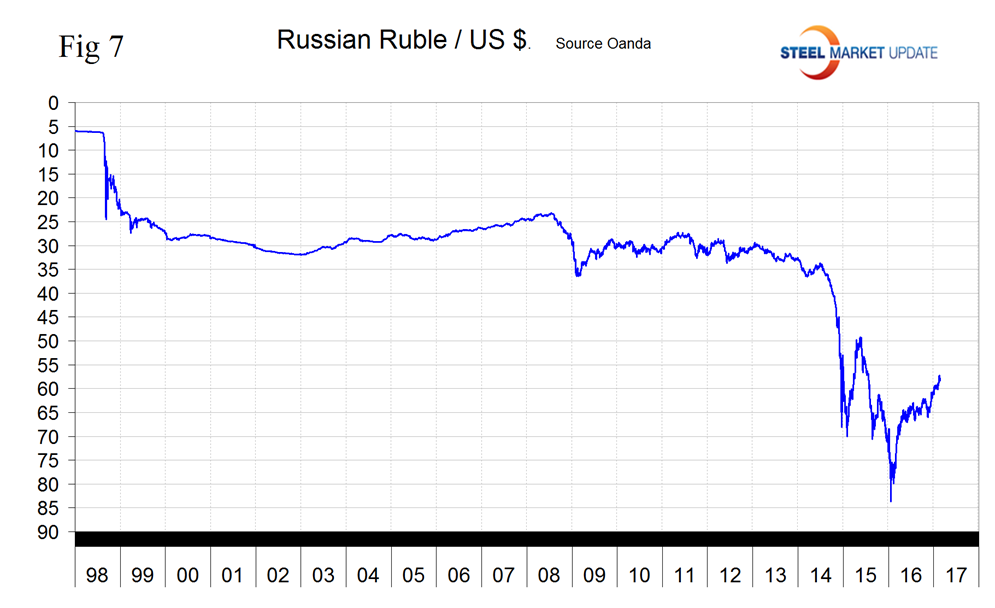

The Russian Ruble

The Ruble bottomed out at 83.67/US $ on January 21st last year. Since then it has gained 30.97 percent to reach 57.7522/US $ on February 21st this year (Figure 7).

On February 20th, Zareena Sayeedova wrote: renewed expectations could spark a bullish reversal in USD/RUB by late February or early March. I guess that the euphoria on the part of ruble bulls really looks overblown and is fed merely by hopes about economic growth in 2017. It’s also noteworthy that the Russian government is not exactly interested in a strong ruble, thus leading to further measures from the Finance Ministry. While the ministry’s foreign currency purchases have not yet pushed the ruble lower in recent days, this mechanism could yield fruit later when risk sentiment subsides. Oil prices are not expected to exceed the USD 50-60/bbl band any time soon, so the ruble will not see a reason to extend gains.. Another upside driver for the ruble is an increase in the Bank of Russia’s international reserves since early 2017. In the week through February 3, the country’s international reserves grew $1.6 bn, adding another $6.6 bn a week earlier. Meanwhile, the Russian regulator’s currency purchases have not yet led to a weaker ruble, on the contrary, the Russian currency has been able to log decent gains despite the fact that foreign investors closed, in part, their long positions in the ruble after the finance ministry announced a foreign currency purchase program. Meanwhile, the greenback has shown resilience to Donald Trump’s remarks which sometimes look like bombs for the currency market. Market participants now know how to react calmly to unexpected twists and turns in the newly elected president’s policy. This means more upside for the U.S. dollar in the medium term. I suggest that it is a game changer for USD/RUB in addition to the Fed’s recent hawkish comments.

Explanation of Data Sources: The broad index is published by the Federal Reserve on both a daily and monthly basis. It is a weighted average of the foreign exchange values of the U.S. dollar against the currencies of a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares and from U.S. and foreign import shares. The data are noon buying rates in New York for cable transfers payable in the listed currencies. At SMU we use the historical exchange rates published in the Oanda Forex trading platform to track the currency value of the US $ against that of sixteen steel trading nations. Oanda operates within the guidelines of six major regulatory authorities around the world and provides access to over 70 currency pairs. Approximately $4 trillion US $ are traded every day on foreign exchange markets.