Prices

April 4, 2017

SMU Price Ranges & Indices: Prices Adjust to Mature Market Conditions

Written by John Packard

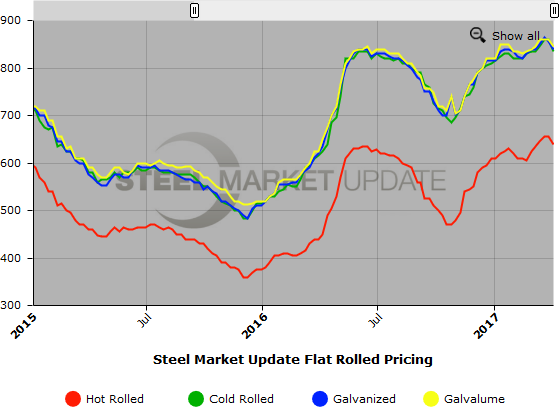

Flat rolled steel prices are showing themselves as being in a “mature” market having been on the rise for most of the 24 weeks since prices began their climb at the end of October 2016. We peaked out on hot rolled at $655 per ton over the last two weeks. This week we moved off that number and drifted lower with our new HRC average being down $15 per ton.

But, I think it is important for our readers to know we are not seeing any signs of panic out of the steel mills. Yes, we have found evidence that some mills on some products (like cold rolled) may be a little weaker than what was seen a few weeks back. The drop in prices was mostly due to a widening of the spread.

We also haven’t seen blood-thirsty steel buyers expecting to feed on much lower-priced spot flat rolled in the coming weeks.

A service center executive told us, “I think the current coated and CR prices are too high compared to foreign markets and it’s tough to not draw in more imports if the spread continues, plus we’re starting to see the markets in Asia weaken at least recently. I think the HR price here has been weaker than normal (but still high compared to Asia) due to demand. With energy, construction, and equipment markets beginning to pick up and imports declining, it appears to be the place the domestics can move up with little resistance. We’ve also seen a mill or two have trouble closing out April on coated. Just in a couple of instances as most mills are doing quite well on coated, but the guys that rely mainly on spot seem to be having a little more trouble as the pricing has the spot market still scared.”

A large cold rolled buyer told us, “Domestic mills just seem more sensitive to foreign offers and are more willing to work with buyers who have legitimate opportunities. Not tire kickers! This varies mill to mill. Some have little to sell and aren’t negotiating, but others are willing to discount where the opportunity makes sense.”

There has been much discussion among buyers that the wide spread between hot rolled and cold rolled/coated base prices may begin to shrink due to foreign competition and perhaps a slowing order book on those products while, as the executive pointed out above, the hot rolled market is strengthening. We will have to see what, if any, lower scrap prices will have on the spot markets come next week…

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $620-$660 per ton ($31.00/cwt-$33.00/cwt) with an average of $640 per ton ($32.00/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $10 per ton compared to one week ago while the upper end declined $20 per ton. Our overall average is down $15 per ton compared to last week. Our price momentum on hot rolled steel is pointing to Higher which means we expect prices to increase over the next 30-60 days.

Hot Rolled Lead Times: 3-6 weeks

Cold Rolled Coil: SMU price range is $810-$860 per ton ($40.50/cwt-$43.00/cwt) with an average of $835 per ton ($41.75/cwt) FOB mill, east of the Rockies. The lower end of our range decreased $30 per ton compared to last week while the upper end declined $20 per ton. Our overall average is down $25 per ton compared to one week ago. Our price momentum on cold rolled steel is pointing to Higher which means we expect prices to increase over the next 30-60 days. However, we are evaluating cold rolled momentum and there could be a change in the coming days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $40.50/cwt-$43.50/cwt ($810-$870 per ton) with an average of $42.00/cwt ($840 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $20 per ton compared to one week ago while the upper end declined $10 per ton. Our overall average is down $15 per ton compared to last week. Our price momentum on galvanized steel is pointing to Higher which means we expect prices to increase over the next 30-60 days. We are evaluating galvanized momentum and there could be a change in the coming days.

Galvanized .060” G90 Benchmark: SMU price range is $888-$948 per net ton with an average of $918 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 5-10 weeks

Galvalume Coil: SMU base price range is $40.50/cwt-$44.00/cwt ($810-$880 per ton) with an average of $42.25/cwt ($845 per ton) FOB mill, east of the Rockies. The lower end of our range decreased $30 per ton compared to last week while the upper end remained the same. Our overall average is down $15 per ton compared to one week ago. Our price momentum on Galvalume steel is pointing to Higher which means we expect prices to increase over the next 30-60 days. We are evaluating Galvalume momentum and there could be a change in the coming days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1101-$1171 per net ton with an average of $1136 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-8 weeks

Plate: SMU price range is $740-$810 per ton ($37.00/cwt-$40.50/cwt) with an average of $775 per ton ($38.75/cwt) FOB delivered. The lower end of our range increased $10 per ton compared to one week ago while the upper end rose $40 per ton. Our overall average is up $25 per ton compared to last week. Our price momentum on plate steel is now pointing to Higher which means we expect prices to increase over the next 30-60 days.

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. We will add plate prices to this graph once we have gathered a few months of data. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.