Government/Policy

April 13, 2017

OCTG from Korea - The Particular Market Situation Case

Written by Lewis Leibowitz

The following article on the recent OCTG ruling from the Republic of Korea is from trade attorney Lewis Leibowitz. We will provide his contact information at the end of the article:

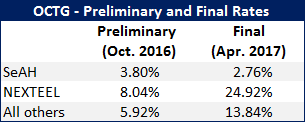

Last Tuesday, the US Commerce Department published its final determination on antidumping duties for the first administrative review period on oil Country tubular goods from the Republic of Korea. Commerce reversed its preliminary determination of last October, deciding that a “particular market situation” (“PTMS”—PMS was already taken :-)) existed in Korea concerning the cost of hot-rolled steel coil (“HRC”). Commerce adjusted the “normal value” of the subject OCTG for the mandatory respondents (SeAH and NEXTEEL). The rates went up for NEXTEEL, but they did not increase for SeAH.

The preliminary and final rates in the review were:

This determination appears to be the result of intense political pressure. The steel industry has a number of officials in the Trump Administration, both present and prospective. In March, Peter Navarro, the Chairman of the President’s National Trade Council, sent a memorandum urging Commerce to use the new PTMS standard as the only way to get antidumping margins above single digits. The PTMS standard is entirely undefined in the statute, giving Commerce enormous discretion in interpreting the statute. Under the Chevron Supreme Court case, the courts must give deference to “expert” agency interpretations. While this determination may well be appealed, the courts will have to find the agency’s legal interpretation “unreasonable” to overturn it. Both Commerce and the steel industry are hoping that the determination will be sustained.

The 130-page Commerce decision does not provide information sufficient to determine precisely how these margins were calculated. It is remarkable that the application of PTMS resulted in a significant increase for one respondent but an actual decrease for the other. More likely, the small decrease for SeAH was due to factors other than the PTMS.

The reason for the difference may be the type of “normal value” that Commerce used for each mandatory respondent. NEXTEEL had no home market sales and no third country sales, so that company’s normal value was based on “constructed value”. Constructed value (“CV”) is the sum of the cost of manufacture (including cost of materials such as HRC), general and administrative costs and overseas packing costs. In addition, Commerce adds an allowance for profit based on one of several formulas. Perhaps with a touch of irony, Commerce used the figure for SeAH’s profits on its Canadian sales. NEXTEEL argued strenuously against using that figure, but Commerce rejected the arguments. SeAH’s profit was not disclosed, but it likely was substantial, effectively increasing NEXTEEL’s normal value and thereby its dumping margin, while SeAH’s was not affected.

The petitioners tried to knock out SeAH’s questionnaire responses on the ground that they failed to disclose certain material facts. Commerce evaluated the petitioners’’ arguments and gave SeAH a clean bill of health. Thus, the SeAH margin is based on the information SeAH itself provided.

The elevated costs for HRC did not affect SeAH’s Canadian sales, probably because few of those sales were below cost. Canadian prices are not very different from US prices, the SeAH margin was low.

Not so NEXTEEL. Their normal value was entirely based on constructed value. HRC costs are 80 percent or so of the total costs for welded OCTG, so when Commerce elevated the costs by the countervailing duty margins based on domestic subsidies, NEXTEEL’s margin was increased substantially.

The impact of this decision could be significant. No doubt NEXTEEL will appeal the result to the courts; however, the Commerce determination will apply to future entries, which will have to post a 24.92 percent cash deposit until the court decision is finished, which could take two years or more. The use of PTMS was a first for Commerce. No doubt, there will be litigation over the meaning of the PTMS standard, which has essentially no guidance from Commerce. Given the current controversy in Congress about the degree of judicial deference to agency decisions, this case could provide the occasion for some rethinking of the Chevron doctrine.

Lewis Leibowitz, The Law Offices of Lewis E Leibowitz, 202-776-1142