Prices

August 3, 2017

Hot Rolled Futures: Continued Price Consolidation

Written by Jack Marshall

The following article on the hot rolled coil (HRC) steel and financial futures markets was written by Jack Marshall of Crunch Risk LLC. Here is how Jack saw trading over the past week:

Steel

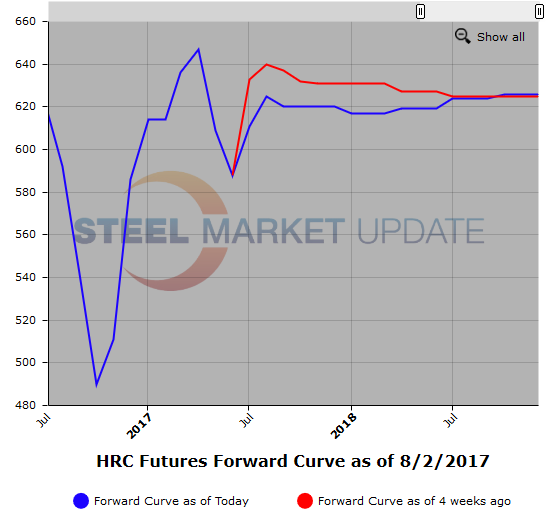

This week HR futures markets experienced continued price consolidation along the curve as HR futures prices continued to retrace lower from the recent highs in the mid 640s.

Higher volumes this week have been due to more hedger interest at these lower levels ($620/ST). With the flattened futures curve, hedgers can buy futures at a much smaller premium to spot versus just a week ago. In the last eight trading days, we have seen spot index rise by $11 and the modestly backwardated futures curve (Q4’17 to Q4’18 -$11/ST) shift back to a slight contango (Q4’17 to Q4’18 +$6/ST). The net result is the differential between spot and the spot month future ( AUG’17) contracted from $38 to $4 on a settlement basis. Spot index versus Q4’17 contracted from $35 to minus $1, and the spot index versus Q1’18 contracted from $34 to minus $4. Spot having aligned with the bulk if the futures curve has more hedgers showing interest.

This past week two noteworthy items for HR futures:

1) 67,100 ST of HR futures traded, which is a nice pickup from recent trends.

2) The HR futures market absorbed 13,000 ST of HR futures at a single price for a nearby month (650 contracts)

HR

Q4’17 618

Q1’18 618

Q2’18 620

Q3’18 624

Below is a graph showing the history of the hot rolled futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact our office at 800-432-3475 or info@SteelMarketUpdate.com.

Scrap

Rising global steel prices continue to support raw materials prices and export scrap prices. Specifically, Turkish demand continues to pull export scrap prices higher. Today we had spot month SC (LME scrap) trading above $340/MT and Q4’17 trading around $320/MT. The sharp move higher in spot cargoes has pushed the curve into a modest backwardation. Heard some recent booking this week on 80/20 @ $329, which is up from the $319-$321 range heard last week.

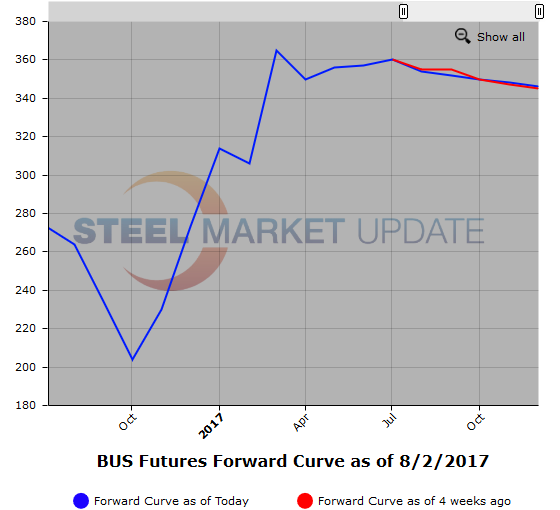

Concern around supplies of U.S. prime scrap have kept the BUS contract well bid. Latest has the balance of 2017 BUS curve around $355/GT. The chatter has August index coming in up $10-15/GT over July ($366/GT) for BUS. The BUS futures curve remains slightly backwardated, but is starting to flatten slightly based on the latest metal margin interests.

Below is another graph showing the history of the busheling scrap futures forward curve. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact our office at 800-432-3475 or info@SteelMarketUpdate.com.