Plate

November 12, 2017

Analysis of Sheet, Plate Imports by District of Entry, Source through September 2017

Written by Peter Wright

This Steel Market Update analysis breaks down the imported tonnage of six flat rolled steel products by district of entry and source country through September 2017. We believe that misinformation (or a lack of) about regional import volumes is often used to influence purchase decisions. Our intent with this analysis of tonnage by district of entry is to describe in detail what is going on in a company’s immediate neighborhood and thus provide a negotiating advantage for our premium subscribers.

![]() Premium members will find reports in the Imports/Exports section of our website that break down the import tonnage through September into the port of entry and country of origin in metric tons. Products analyzed in this way are hot rolled, cold rolled, hot-dipped galvanized sheet, other metallic coated sheet, cut to length plate and coiled plate. This dataset is large; therefore, we make no attempt to provide a commentary. Each reader’s interest will be different and he or she simply needs to select one of the six products, then find the nearest port or ports of entry to see how much came into the region each month and from where. It is clear from these detailed reports that the change in tonnage entering a particular district in many cases is completely different than the change in volume at the national level.

Premium members will find reports in the Imports/Exports section of our website that break down the import tonnage through September into the port of entry and country of origin in metric tons. Products analyzed in this way are hot rolled, cold rolled, hot-dipped galvanized sheet, other metallic coated sheet, cut to length plate and coiled plate. This dataset is large; therefore, we make no attempt to provide a commentary. Each reader’s interest will be different and he or she simply needs to select one of the six products, then find the nearest port or ports of entry to see how much came into the region each month and from where. It is clear from these detailed reports that the change in tonnage entering a particular district in many cases is completely different than the change in volume at the national level.

Some examples to illustrate why this information can be actionable are as follows. Examples are for 2017 through September:

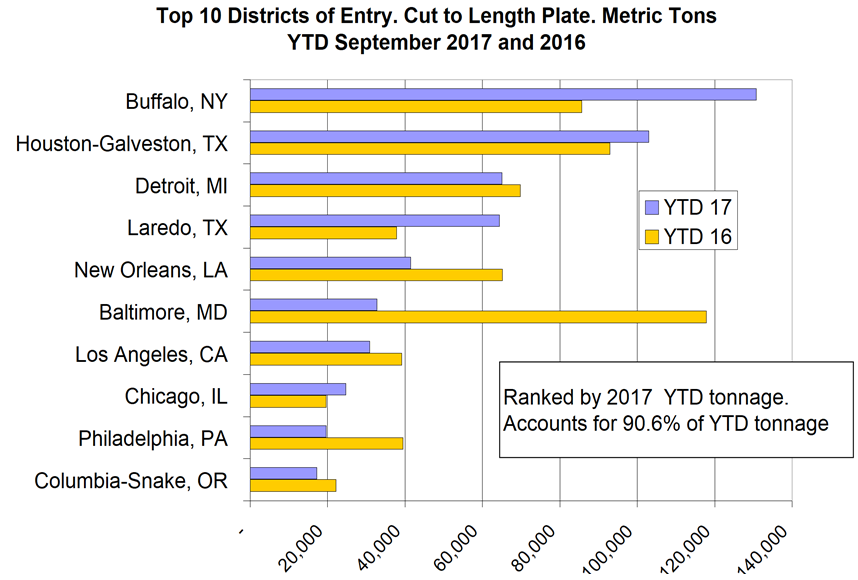

· Total cut-to-length plate imports are down by 32 percent, but Tampa has been shut out in 2017 after receiving 206,000 metric tons through September last year. In 2017, Buffalo was up 53 percent through September and Baltimore was down by 72 percent.

· Total HRC imports were down by 30 percent through September, but San Francisco was down by 91 percent from 456,000 metric tons in 2016 to 42,000 in 2017.

· The total of other metallic coated, mainly Galvalume, was up by 27 percent year to date through September, but Savannah was up by 93 percent and Houston was up by 54 percent.

The discrepancy between the change in the national total and the individual regions is why we think it’s important for both market understanding and negotiating position to know what’s going on in your own backyard.

The table included here (click to enlarge) is a small part of the detailed analysis of discrete plate tonnage, and the bar graph shows the tonnage that entered the top 10 districts year to date in September for 2016 and 2017 ranked by 2017 tonnage. These 10 districts account for 90.6 percent of the grand total in 2017. Buffalo received the most tonnage through the first nine months of this year followed by Houston, Detroit and Laredo.

The data in these detailed reports is compiled from tariff and trade data published by the U.S. Department of Commerce and the U.S. International Trade Commission. Our other import reports are sourced from U.S. Department of Commerce, Enforcement and Compliance, aka the Steel Import Monitoring System. In the development of these reports by district and source country, we have discovered that the SIMA data for HRC and CRC contains some high alloy steels such as stainless and tool steel, which have been misclassified at the ports. These alloy steels are not included in our detailed reports, which results in a small discrepancy between the two datasets, for CRC in particular and for HRC to a lesser degree.