Market Data

April 2, 2018

ISM PMI: High Prices, Strong Demand vs. Tariff Concerns

Written by Sandy Williams

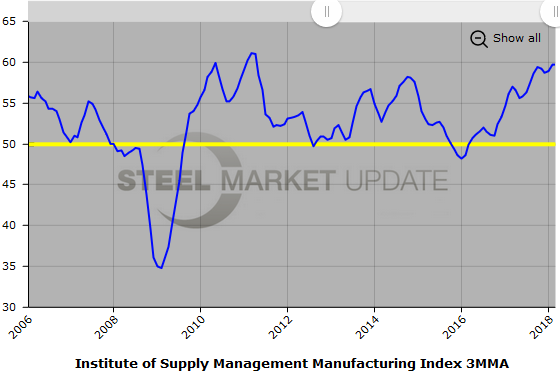

Manufacturing activity expanded in March, though at a slower rate than February, reports the Institute for Supply Management. ISM’s March PMI registered 59.3 percent, down from 60.8 percent in the February survey of corporate purchasing managers. Any reading above 50 indicates growth. New orders continued to expand in March, although slowing 2.3 percentage points from February to a reading of 61.9 percent. Production dipped one percentage point and inventories of raw materials slipped 1.2 points. The customer inventories index, at 42.0 percent, was at its lowest level since July 2011.

The combination of low inventories and high backlogs foretells strong demand in the coming months, despite slower new orders in March, said ISM.

“Consumption, described as production and employment, continues to expand, with indications that labor and skill shortages are affecting production output,” said ISM Chairman Timothy R. Fiore. “Inputs, expressed as supplier deliveries, inventories and imports, were negatively impacted by weather conditions; Asian holidays; lead time extensions; steel and aluminum disruptions across many industries; supplier labor issues; and transportation difficulties due to driver and equipment shortages.”

Employment in the sector remained strong and firms continued to express difficulty in finding skilled workers to replace natural attrition and turnover.

The prices index for raw materials jumped 3.9 points to 78.1 percent in March. Higher prices were noted for all steels, steel components, aluminum and copper. The price index was at its highest level since April 2011 when it registered 82.6.

Indices for new export orders and new import orders showed some slowing last month. The exports index was down 4.1 points, although still in expansion territory. Imports inched down 0.8 percentage points to 59.7. Firms continued to seek foreign materials to support production demand, but were concerned about tariffs and logistics.

Following are comments from survey respondents:

• “Supply constraints, extended lead times, capacity constraints [and the like], particularly in the electronics components markets, continue to frustrate and drain needed resources, have delayed production schedules and, in some cases, caused missed or delayed sales opportunities.” (Computer & Electronic Products)

• “International demand is strong for our products in all regions. We are seeing constraints in multiple chemical supply chains due to increased global demand. We are concerned about the impact of tariff and trade wars on demand, but at this time, [there are] no signals that global demand is slowing.” (Chemical Products)

• “Production targets continue to be a struggle due to shortages of globally sourced components. Many subtier components are in short supply for multiple OEMs.” (Transportation Equipment)

• “Much concern in the industry regarding the steel and aluminum tariffs recently [imposed]. This is causing panic buying, driving the near-term prices higher and [leading to] inventory shortages for non-contract customers.” (Machinery)

• “New tariffs are causing concern across the supply chain. Full impact will take a few weeks to reveal itself.” (Miscellaneous Manufacturing)

• “Significant price increases in the steel commodity due to 232 [the tariffs]. The price increases will begin to impact our company’s performance.” (Primary Metals)

• “Hiring continues to slowly increase from February into March and capital spending was allowed a small increase. Oil market conditions have improved and continue to stabilize.” (Petroleum & Coal Products)

Below is a graph showing the history of the ISM Index on a three month moving average. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at 706-216-2140 or Brett@SteelMarketUpdate.com.