Prices

May 1, 2018

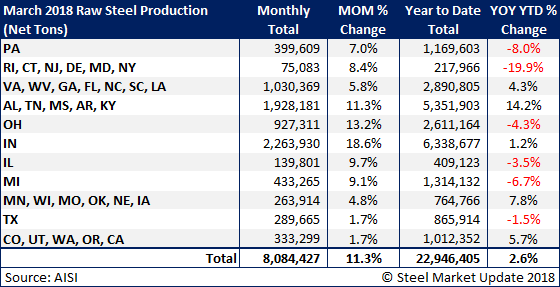

March Raw Steel Production Hits 3.5-Year High

Written by Brett Linton

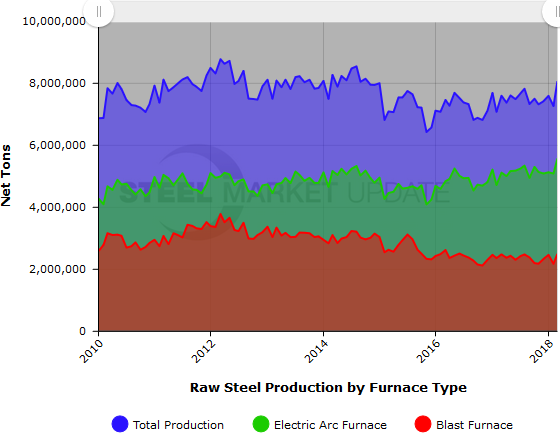

Total raw steel production for the month of March was 8,084,427 net tons, the highest production level since October 2014 when 8,147,661 tons were produced. The production method breakdown was 5,578,866 tons produced by electric arc furnaces (EAFs) and 2,505,561 tons produced by blast furnaces. March raw steel production was 818,072 tons or 11.3 percent higher than February, and 485,074 tons or 6.4 percent higher than the same month last year, reports the American Iron and Steel Institute (AISI) in Washington. AISI’s monthly estimates are different than the weekly estimates we report; the monthly estimates are based on over 75 percent of the domestic mills reporting versus only 50 percent reporting for the weekly estimates.

As seen in the table below, all of the 11 state groups reported an increase in month-over-month production, but just five of the 11 state groups reported an increase in production compared to the same month last year.

The chart below shows total monthly steel production (blue) broken down by electric arc furnace production (green) and blast furnace production (red).

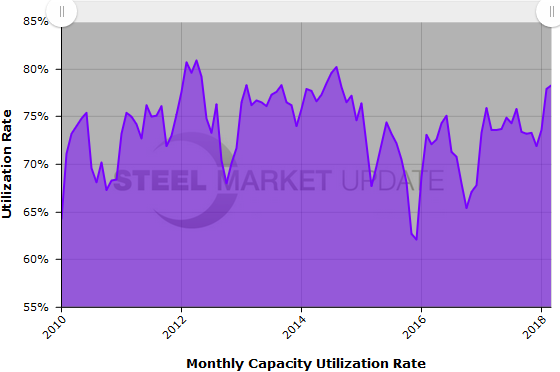

The mill capacity utilization rate for March 2018 was 78.3 percent, up from 77.9 percent in February, and up from 73.6 percent one year ago. This is the highest rate since August 2014, back when 8,546,303 tons were produced at a capcity utilization rate of 80.2 percent.

SMU Note: Interactive versions of the raw steel production graphics above (and more) can be seen in the Analysis section of our website here. If you need assistance logging in to or navigating the website, contact Brett at 706-216-2140 or Brett@SteelMarketUpdate.com.