Market Data

August 12, 2018

Summer Doldrums Affecting Service Center Spot Prices?

Written by John Packard

Flat rolled and plate steel distributors, as well as the manufacturers who purchase spot material from the distributors and wholesalers, are reporting a softening of spot pricing. That is the spot pricing service centers are offering their manufacturing customers.

Last week, Steel Market Update conducted our early August flat rolled and plate steel market analysis. We invited approximately 630 people representing about 610 companies to participate in our questionnaire. The invitations are intentionally stacked so service centers and manufacturing companies combined equal at least 80 percent of the total responses. In last week’s survey, 54 percent of the respondents were service centers and 33 percent manufacturing companies.

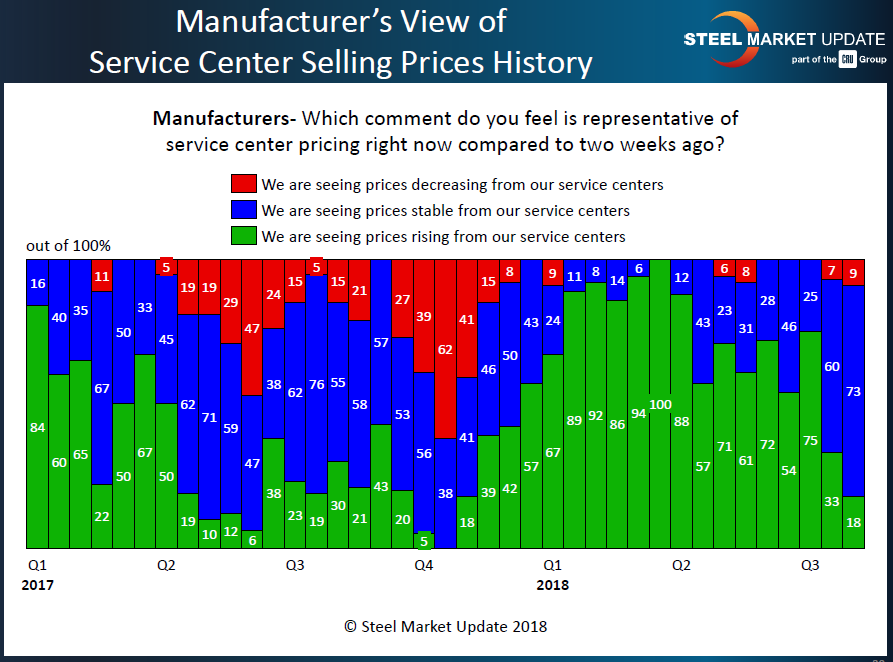

Over the past six weeks, the manufacturers have changed their view of spot pricing. At the beginning of July, 73 percent of the manufacturers responding to our inquiry reported distributors as raising spot pricing. Last week, those reporting higher spot prices dropped to 18 percent. Nine percent of the manufacturers are now reporting spot prices as being lower than they were just two weeks prior.

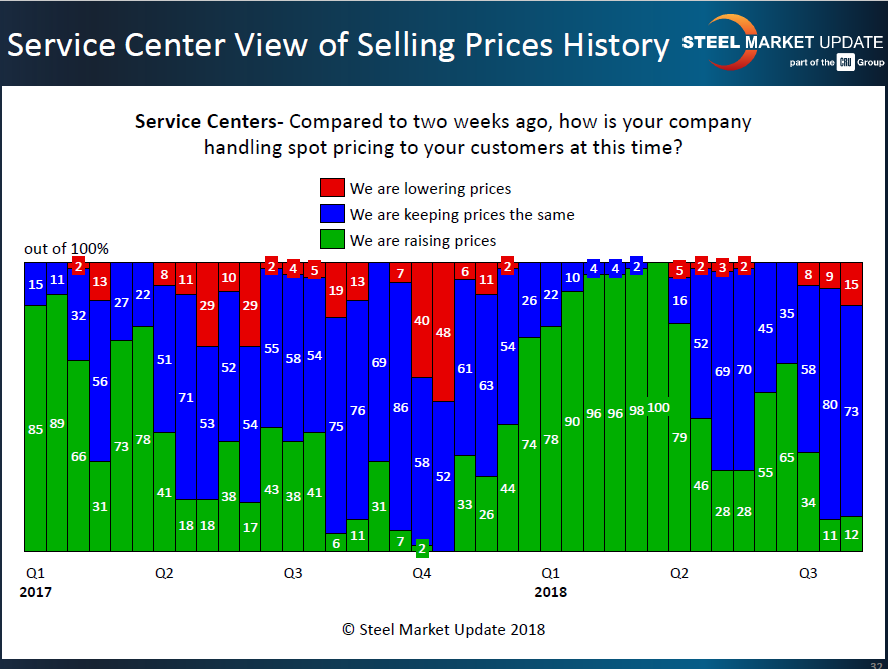

Service centers have been reporting a weakening or softening spot market for a number of weeks. Distributors have been reporting a see-saw spot market coming off of strength in early second-quarter 2018, weakening for a period of six weeks before showing some strength, and now distributors are reporting much weaker spot pricing. In the most recent spike and decline, we saw a majority of service centers reporting high spot prices during the month of June 2018. Since then, spot prices between service centers and their spot customers have dropped off dramatically. Last week, only 12 percent reported a rising spot market, while 15 percent reported spot numbers as falling.

The service center spot market is important to understanding the strength or weakness associated with spot pricing coming out of the domestic steel mills. Based on the results shared in the graphics above, there will be a tremendous amount of pressure on the domestic mills to negotiate lower spot prices.

However, our analysis was done prior to President Trump announcing that tariffs on Turkish steel and aluminum exports to the United States will be doubled to 50 percent for steel and 20 percent for aluminum. We expect, when we go out for our next survey on Aug. 20, that there could be an upward bounce, or there may be no movement at all. We will continue to watch the market carefully to see what impact the new tariffs will make on steel prices.