Market Data

September 16, 2018

August PPI Shows Competitive Position of Steel vs. Other Products

Written by Peter Wright

This article is regularly published for our Premium users, but we decided to share it with our entire readership this month. If you are interested in upgrading to a Premium subscription, contact us at info@SteelMarketUpdate.com or 800-432-3475.

Carbon steel tubular products have a rate of price escalation much higher than plastic products. This is also the case for pre-fabricated metal buildings compared to wood buildings. Truck transportation prices are rising faster than rail, but the gap is closing, according to the latest data from the Bureau of Labor Statistics. Using this information, Steel Market Update provides subscribers with a view of the competitive position of sheet steel, aluminum and plastic, as well as downstream products including beverage cans, metal buildings, pipe, and truck and rail transportation.

![]() Last week, the Bureau of Labor Statistics (BLS) released its series of producer price indexes (PPIs) for more than 10,000 goods and materials through August. For an explanation of this program, see the end of this piece. The PPI data are helpful in monitoring price direction, though there may be a lag between the BLS reports and spot prices for steel products. We have also concluded that the actual index values of the PPIs of different products cannot be compared with one another because they are developed by different committees within the BLS. We believe that this data is useful in comparing the direction of prices in the short and medium term, but tell us nothing about the absolute value.

Last week, the Bureau of Labor Statistics (BLS) released its series of producer price indexes (PPIs) for more than 10,000 goods and materials through August. For an explanation of this program, see the end of this piece. The PPI data are helpful in monitoring price direction, though there may be a lag between the BLS reports and spot prices for steel products. We have also concluded that the actual index values of the PPIs of different products cannot be compared with one another because they are developed by different committees within the BLS. We believe that this data is useful in comparing the direction of prices in the short and medium term, but tell us nothing about the absolute value.

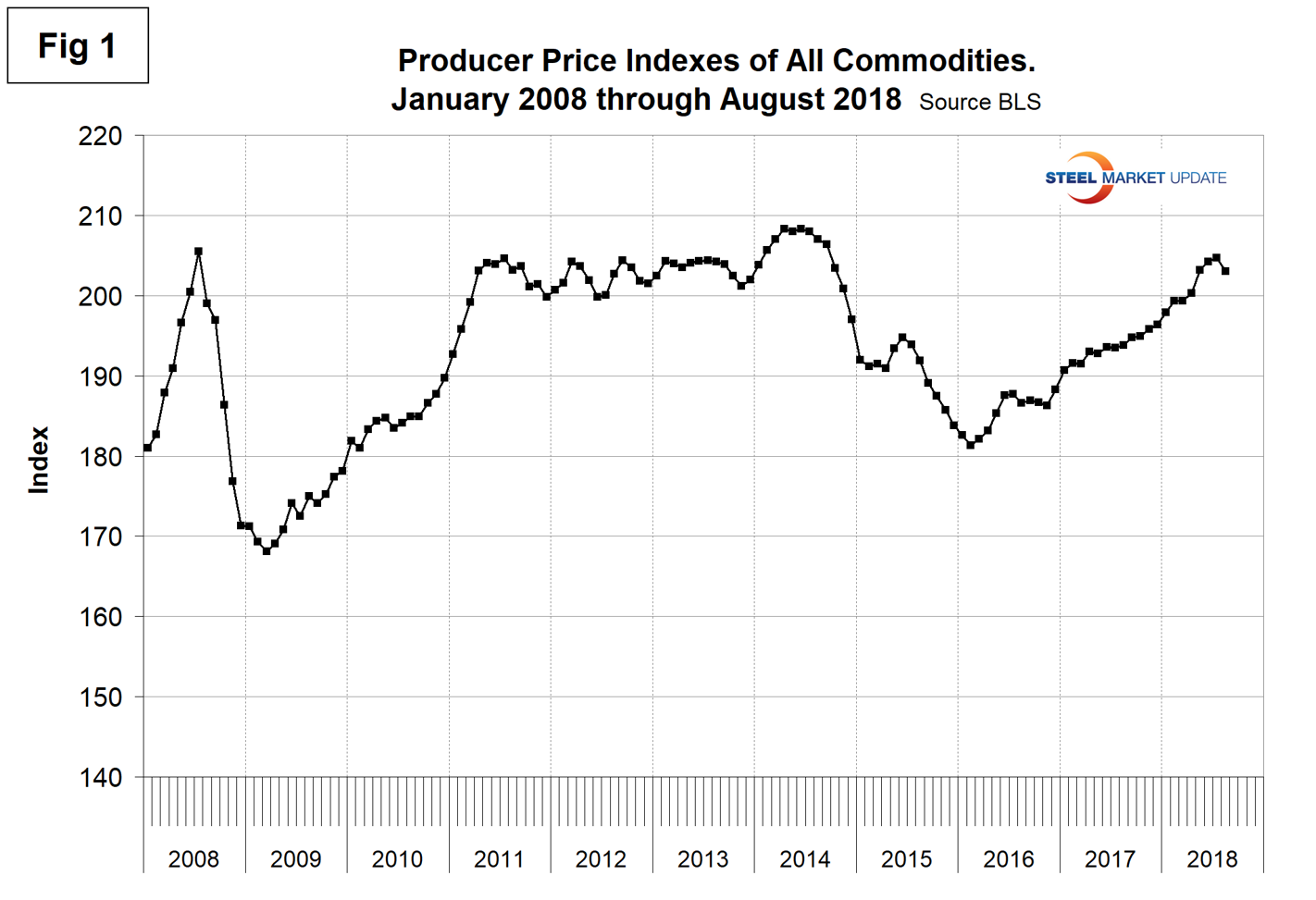

The headline summary from the BLS was as follows: “The Producer Price Index for final demand declined 0.1 percent in August, seasonally adjusted. Final demand prices were unchanged in July and increased 0.3 percent in June. On an unadjusted basis, the final demand index rose 2.8 percent for the 12 months ended in August.” Figure 1 shows the composite PPI of all commodities since January 2008. The index has risen steadily for 2 1/2 years, but is still not back to where it was in 2014.

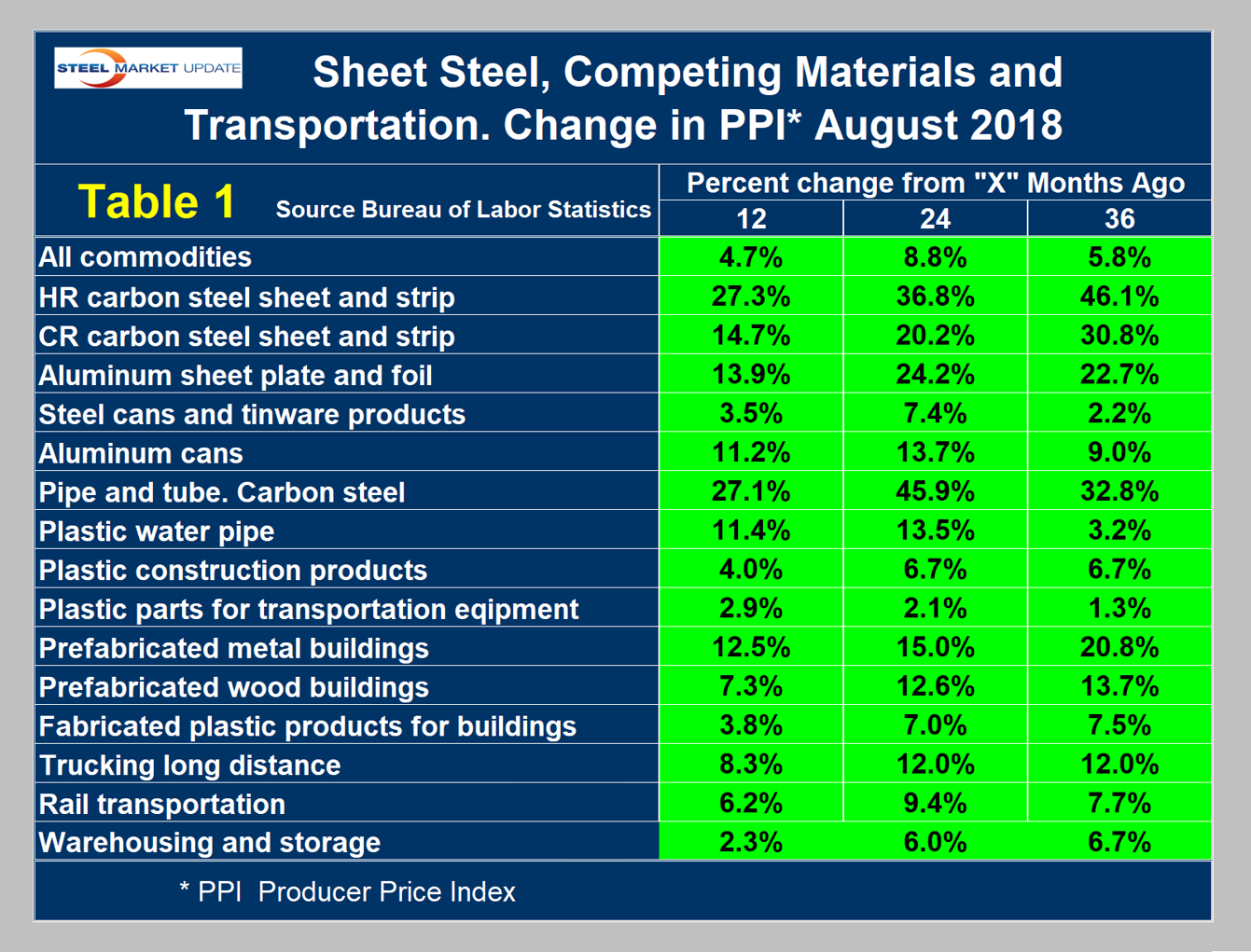

Table 1 is a summary of each category on a year over one-, two- and three-year basis. The gain/loss pattern is shown by the color codes; we interpret rising prices as positive. We began this bimonthly analysis in January 2016, and June and August 2018 were the first times that the whole table was green. The table includes some other plastic products for which there is no direct steel comparison and a measure of price changes for warehousing and storage.

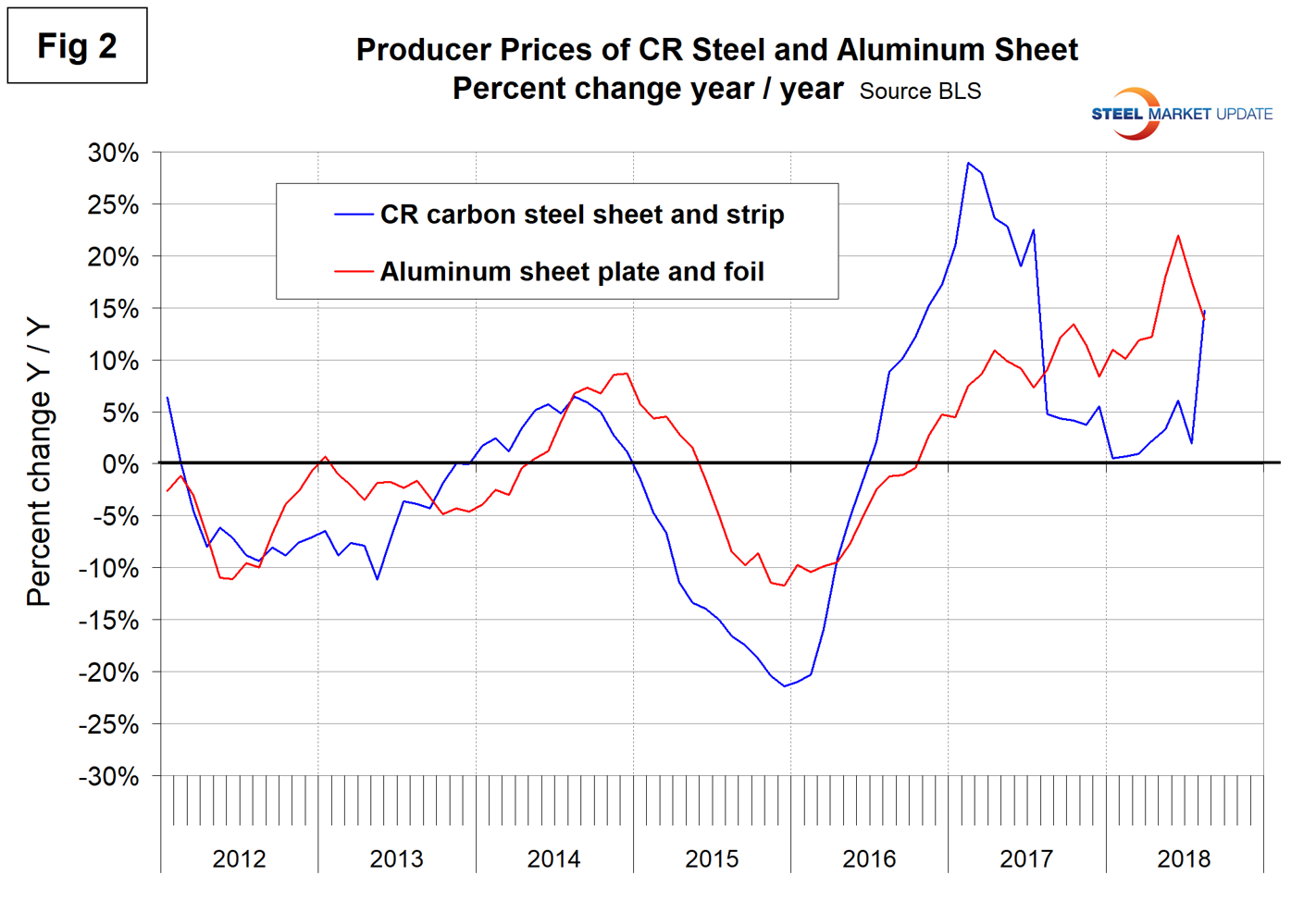

Some specific comparisons of steel and steel products with their competition are as follows. Please note the Y axis scales are not the same.

Figure 2 shows the year-over-year comparison of the price change of cold rolled steel sheet and flat rolled aluminum. The price of aluminum sheet has escalated faster than cold rolled steel since Q3 last year, but August was catch-up time and the present rates of price inflation are almost exactly the same.

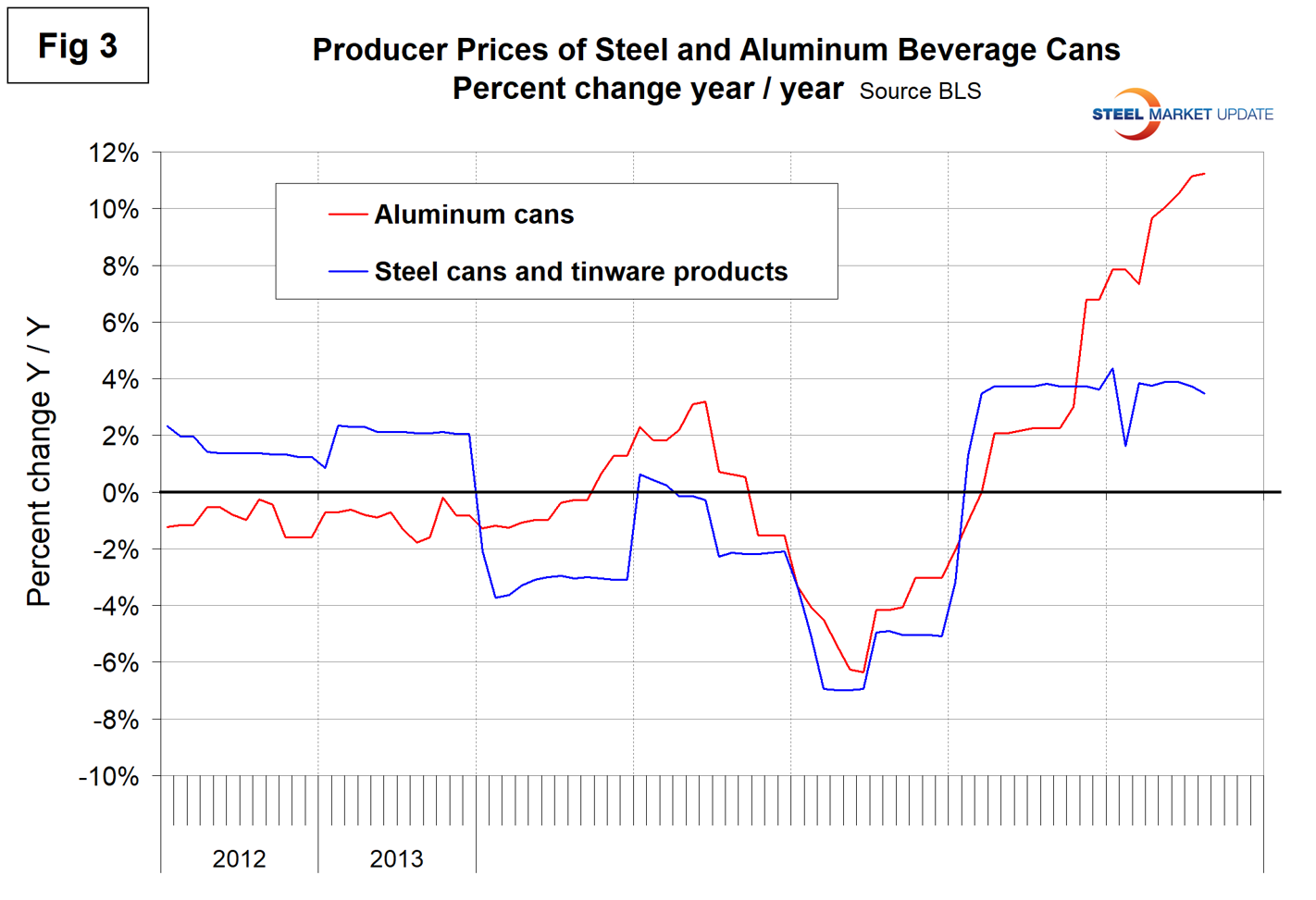

Figure 3 shows the same comparison for steel and aluminum beverage cans. Evidently the escalation in steel prices has not yet percolated down to the can level. Steel’s competitive position has improved since Q3 2017, but that is probably about to change.

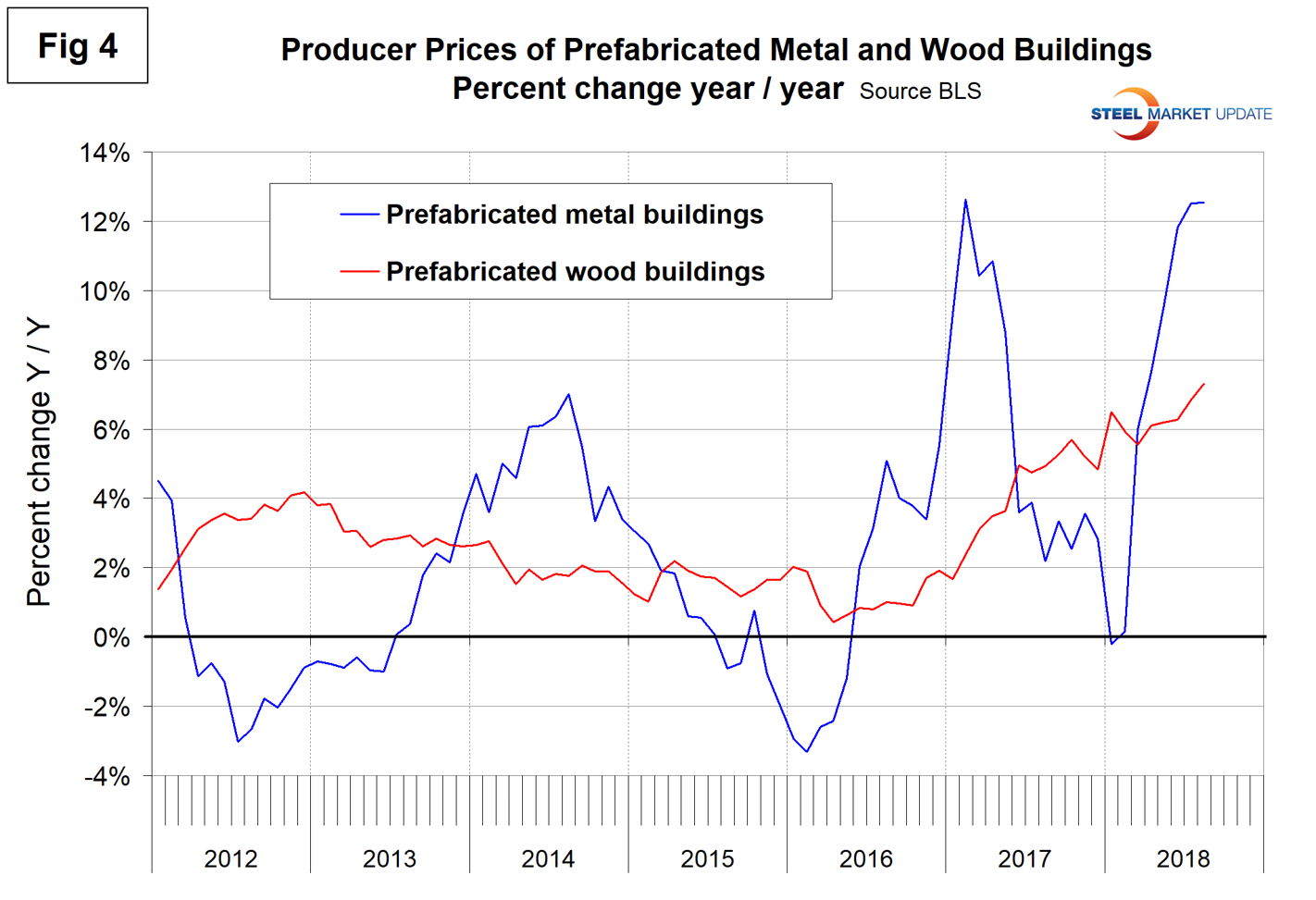

Figure 4 compares prefabricated metal with prefabricated wood buildings. From mid-2017 through February 2018, the price of wood buildings escalated faster than steel, but since then there has been an abrupt change to the detriment of steel’s competitive position.

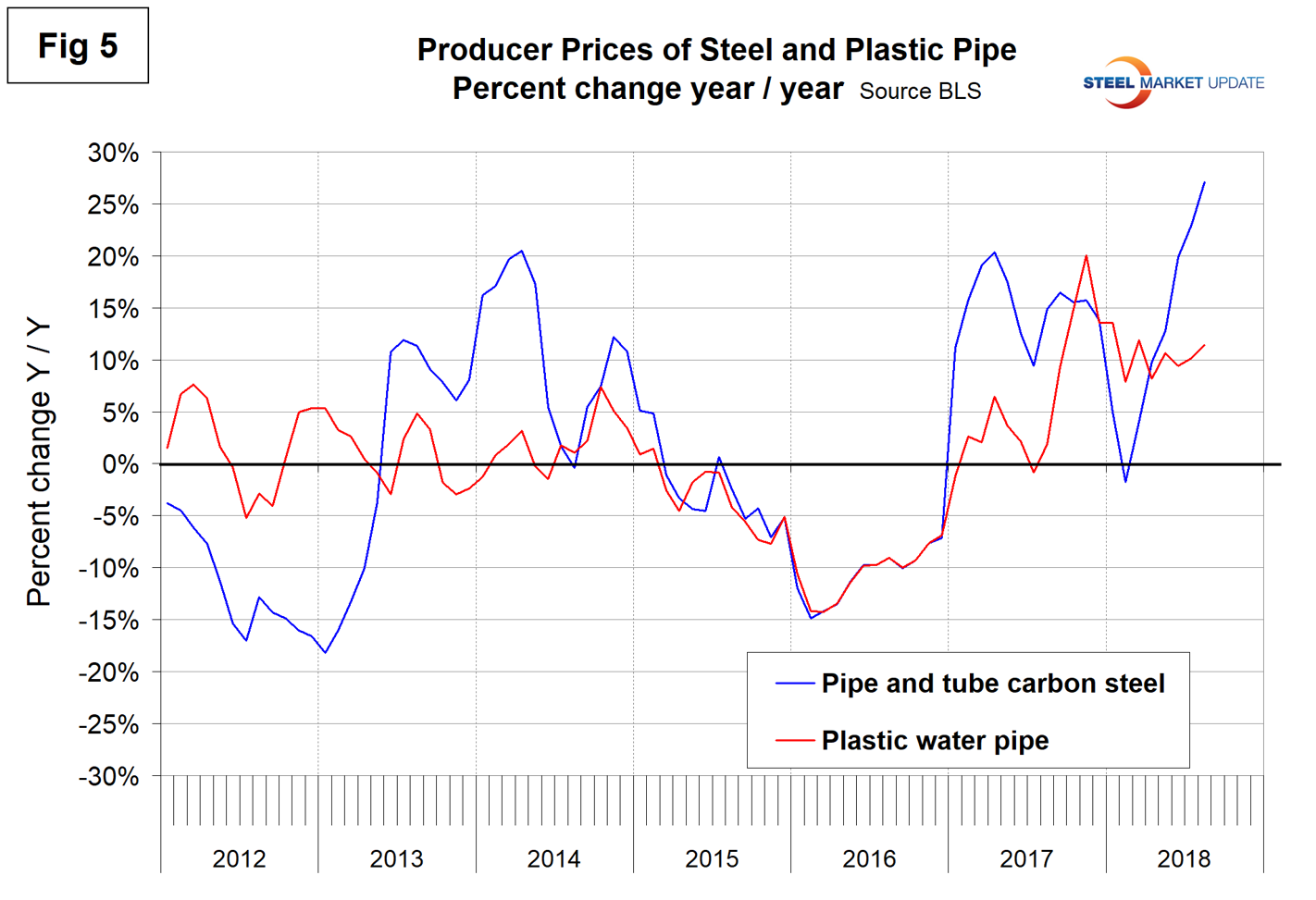

Figure 5 compares steel and plastic pipe. Carbon steel pipe is currently experiencing a high rate of price escalation, but plastic pipe has been trending down in 2018.

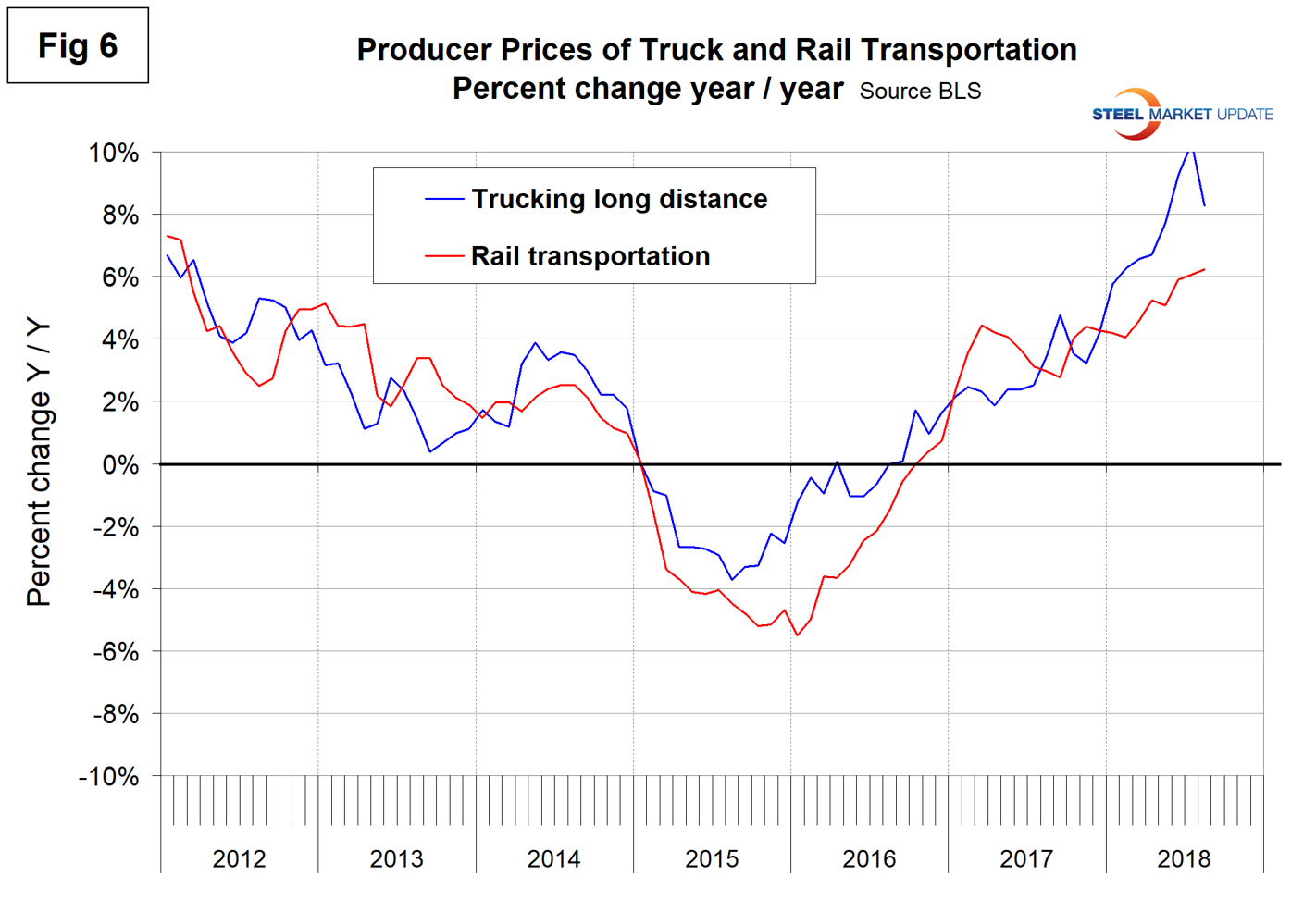

Figure 6 compares the changes in the price of truck and rail transportation. Trucking price increases through July have outpaced rail since last December. The gap closed in August when truck transportation was up by 8.3 percent year over year and rail was up by 6.2 percent.

Explanation: The official description of this program from the BLS reads as follows: “The Producer Price Index (PPI) is a family of indexes that measure the average change over time in the prices received by domestic producers of goods and services. PPIs measure price change from the perspective of the seller. This contrasts with other measures, such as the Consumer Price Index (CPI). CPIs measure price change from the purchaser’s perspective. Sellers’ and purchasers’ prices can differ due to government subsidies, sales and excise taxes, and distribution costs. More than 10,000 PPIs for individual products and groups of products are released each month. PPIs are available for the products of virtually every industry in the mining and manufacturing sectors of the U.S. economy. New PPIs are gradually being introduced for the products of industries in the construction, trade, finance, and services sectors of the economy. More than 100,000 price quotations per month are organized into three sets of PPIs: (1) Stage-of-processing indexes, (2) commodity indexes, and (3) indexes for the net output of industries and their products. The stage-of processing structure organizes products by class of buyer and degree of fabrication. The commodity structure organizes products by similarity of end use or material composition. The entire output of various industries is sampled to derive price indexes for the net output of industries and their products.