Overseas

February 14, 2019

CRU: Global Sheet Prices Start to Turn Higher, Iron Ore to Add On

Written by Tim Triplett

Editor’s note: The following is excerpted from the Feb. 13 CRU Steel Sheet Monitor; editing by CRU Principal Analyst Josh Spoores.

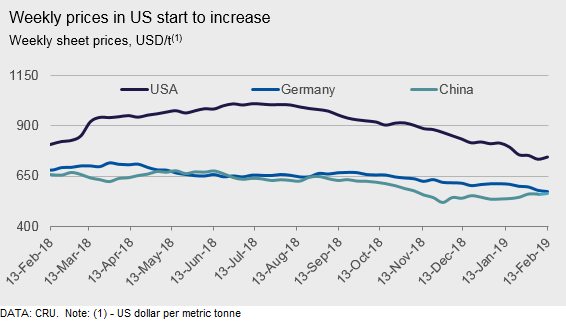

In our Steel Sheet Products Monitor last month, we asked if the market was near an inflection point. That report was published on the sixth working day of the year and, at that point, global sheet prices were consistently lower in all regions from December. It is now five weeks later, and current data suggests that most markets have reached a price bottom, or they are about to.

CRU’s sheet price assessments for February reflect this hypothesis. While some markets have continued to fall such as Germany, India and the U.S., we have seen some markets steady while others, such as Asia, CIS and Turkey, have seen prices surge higher by 9-12 percent. These markets with significant m/m gains are reflective of export or import prices, though these prices are leading indicators that global sheet prices are turning higher.

Regional sheet prices are reflected in the Global Flat Products Price Indicator (CRUspi flats), which is a weighted average. Due to the regional makeup, the February reading of this indicator fell for the seventh consecutive month to 163.5, a m/m decline of 1.0 percent.

The fundamentals of each regional market do vary, though a trend is starting to appear as some prices rise while others look to be at or near a bottom. Due to the overall price declines seen over the past several months, prices for some regions have approached production costs. This convergence is not sustainable over the longer term, and due to a recent disaster in Brazil we are now seeing notably higher steelmaking costs.

On Jan. 25, the world’s largest iron ore producer, Vale, saw one of its tailing dams collapse in Brazil. This tragic accident will result in higher iron ore prices for some time to come. Even for markets such as the U.S. where domestic pellets are used, the price of these pellets are tied to not only global iron ore prices but also a pellet premium, reflecting the price of Vale’s pellets. Brazil’s slab exports are already rising in price due to this issue and gains can also be seen for metallics as well. Further details can be found in our recent CRU Insight.

Outlook: Higher Sheet Prices to Come on Stronger Fundamentals and Cost-Support

We expect near-term price strength to emerge across most regions. However, this uptrend will be limited in duration. Stronger seasonal demand and higher costs due to the aforementioned situation with iron ore is a key trend for multiple regions. In Europe, recent safeguards add to this supply pressure.

However, our attention is focused on China, where expectations are rising for new stimulus measures to directly support sheet demand. This is covered in more detail in the China section of this report. The synopsis of this stimulus, though, is for new subsidies to emerge in support of new consumer purchases of vehicles, as well as home appliances. Overall, we expect higher near-term prices for global sheet due to improved demand as well as higher steelmaking costs.