Overseas

June 27, 2019

CRU: U.S. Sheet Prices Crash, Forcing Mills to Raise Prices

Written by Tim Triplett

By CRU Principal Analyst Josh Spoores

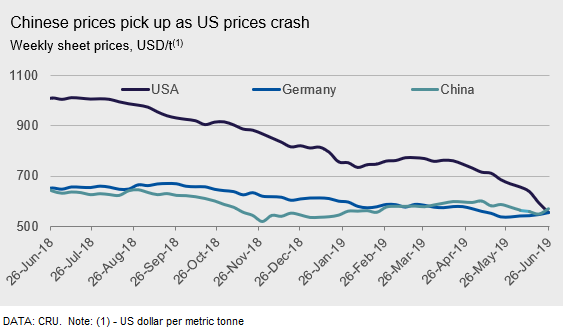

Sheet prices in the U.S. have continued to fall with HR coil making a significant decline. For HR coil, CRU’s price assessment fell $34 /s.ton w/w to $505 /s.ton, the lowest price recorded since mid-November 2016.

North America

Our index is a volume-weighted average of actual transactions from last week. While we noted a wide range of transactions (~$100 /s.ton), actual volume was increased notably, back to the highs seen in late January/early February of this year. Anecdotally, we heard some buyers were even limited by mills in placing all the orders they wanted. With that said, around 85 percent of volume was submitted for prices below $525 and just 15 percent above that price level. While we had multiple data points in the $550-$560 range, the size of orders here were so small, that they didn’t balance out the significantly larger, lower priced transactions. In the past, price moves of this nature of significant volume and aggressively low prices often led to new price increase announcements. So, it comes as no surprise to see Nucor announce a $40 /s.ton increase. The question is not only what will scrap do, but how will other EAF mills react? Current steel prices, even as low as they currently reside, are well within a historical range of a “scrap-plus” fair value. However, with this fall, U.S. HR coil is the same price as HR coil in Germany and now below domestic Chinese prices.

On the West Coast, sheet prices appear near the bottom, which prompted some buyers to place orders at lower prices. USS-POSCO Industries followed Nucor’s $40 /s.ton price increase announcement on Tuesday, and market sources believe that California Steel Industries will also announce an increase for its August bookings. Demand for HDG coil has been relatively strong, and market sources believe that mill price increases will stop prices from sliding further.

Europe

European HDG coil prices are unchanged this week, and German CR coil is €2 /t higher, but HR coil prices are slightly lower in both Germany and Italy. Market activity is reported to be quite subdued this week, reflecting a combination of some holidays, industry events and widespread uncertainty about the next price direction. CRU’s analysis indicates that HR coil prices are close to breakeven on a full cost basis for German mills, which would lend further support to the thesis that there is some near-term upside to come for prices. However, for now that upside remains elusive and uncertain.

China

Chinese domestic sheet prices saw a RMB20-120 /t increase w/w. While demand remains weak, the market was buoyed by easing supply as Tangshan orders more production curbs. Tangshan’s decision comes at a time when city officials were being blamed on unsatisfying air quality conditions in recent months. This cut will need 34 local steel mills to cut blast furnace capacity by up to 50 percent for a month. Lifting of the restrictions will depend on air quality conditions on Aug. 1. The most traded HR coil futures in Shanghai gained 3.7 percent on Monday and 1.7 percent on Tuesday as such a move is expected to provide some strength to sheet prices, especially at a time when many sheet producers are struggling to make money. Indeed, CRU’s cost model shows that current HR coil profitability is below zero considering current high production cost, and some mills are starting to react by carrying out maintenance to ease supply. We doubt the longevity of such a price rebound due to limited supply restrictions in Tangshan given current policy coverage.

Asia

The imported sheet market in Asia has had an active week with many deals heard concluded before offers started rising again.

A major Chinese mill was heard to have sold out their allocation for HR coil SAE1006 at $505 /t CFR Vietnam. Most Chinese mills were heard to have raised their offers on Monday by $5-10 /t. For this grade, offers from Indian mills were at $505/t CFR Vietnam early last week and then raised to $510 /t CFR Vietnam on Friday.

For SS400, several deals were reported at $493-495/t CFR Vietnam for end of July/August shipments. Some were booked by end users and some were booked by traders who previously signed short-selling deals.

CRU assessed HR coil prices at $500 /t, CFR Far East Asia, flat w/w. CR coil prices were assessed at $540/t CFR Far East Asia, unchanged w/w, while HDG prices were assessed at $580 /t CFR, flat w/w.