Prices

September 19, 2019

CRU: Zinc’s Refined Market Edges into Balance

Written by Tim Triplett

By CRU Senior Analyst Helen O’Cleary

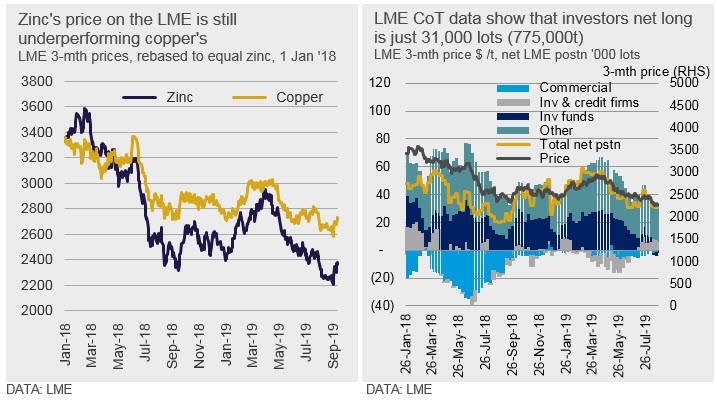

August ended on a bearish note as weak economic data from the USA signaled that the U.S. economy had slipped into contraction territory and European manufacturing data confirmed ongoing contraction. These data, coupled with ongoing rmb weakness, heightened concerns over metal demand going forward and helped push zinc’s price to a 2019 low of $2,203.5/t in early September, a loss of $745/t from its year-to-date high in early April.

Despite zinc’s price decline, the market remained in a modest backwardation even as it reached its year-to-date low due to critically low LME stock levels. The turnaround in zinc’s price was then swift as political developments lifted market sentiment on Sept. 3-4. First came news that Hong Kong’s legislative council was to fully remove the contentious extradition bill, boosting the Hang Seng index and commodities prices. This was swiftly followed by developments in the UK suggesting that a no-deal Brexit was less likely and the U.S. and China agreed to resume trade talks in October, all of which helped lift zinc’s price to $2,380/t on Sept. 13 (although it has since given up some of its gains). LME Commitments of Traders data show that investors still do not view zinc particularly favorably, with non-risk-reducing net longs (which we take to mean speculative) close to recent lows of around 31,000 lots (775,000t).

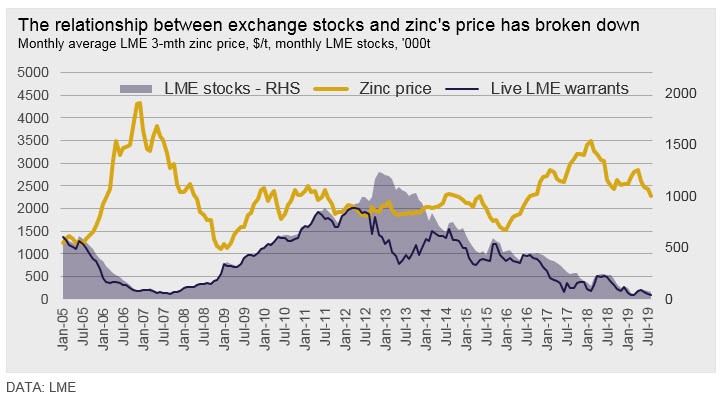

The relationship between exchange stocks and prices broke down early last year as zinc’s price began to slide on improved mine supply and lower TCs, leaving zinc’s forward spreads to reflect critically low stocks in the form of a wide and persistent backwardation. Although zinc’s price has partially recovered in recent months it has been more due to wider market sentiment than zinc’s own fundamentals and, with concentrate stocks already building and Chinese smelter output continuing to rise, we believe that zinc’s price will struggle to gain much ground in the coming months.

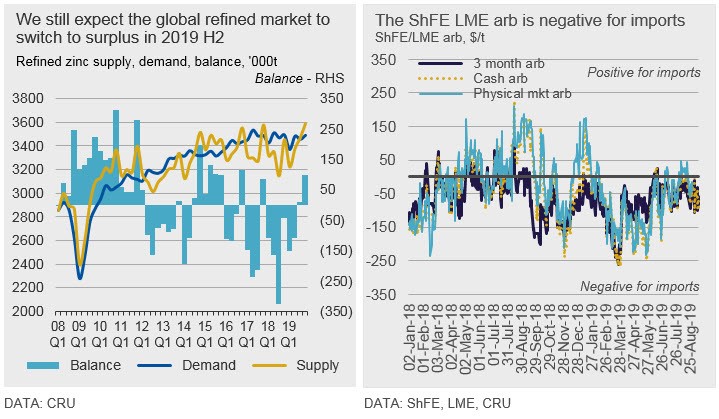

The Global Refined Market Will Switch to Surplus in 2019 H2

The refined market has remained tighter than we were expecting it to this year; ex-China mine supply and smelter output has disappointed, with slower than expected ramp-ups at projects such as New Century Tailings and Gamsberg and lower than expected smelter output in South Korea, Europe and India. Although we have also downgraded our refined demand outlook, supply-side issues have delayed the refined market’s return to balance. We still expect the global refined market to switch to surplus in 2019 H2, but it seems unlikely that it will be enough to offset larger than expected deficits in H1. However, increasing concentrate inventories and a strong pickup in Chinese smelter utilization rates against a backdrop of weak demand mean that market deficits will soon be a thing of the past, and we therefore remain bearish on zinc’s price outlook going forward.

Sentiment in the Chinese market has begun to improve, and we are still expecting demand to perform better in H2 than H1. However, the increase in smelter output and surprisingly high Chinese net refined imports in the first seven months of the year lead us to believe that the import arb is unlikely open in the short-term. Despite relatively low stocks in China, we have not yet seen anything to suggest that domestic demand will recover enough to force the arb to open, particularly as traders seem ready to sell any rallies on the ShFE.