Prices

October 22, 2019

CRU Analyst: Price Volatility Here to Stay

Written by Sandy Williams

Steel price volatility was persistent in 2019, said CRU Principal Analyst Josh Spoores at the FMA/ASD Executive Networking Series held in Pittsburgh last week.

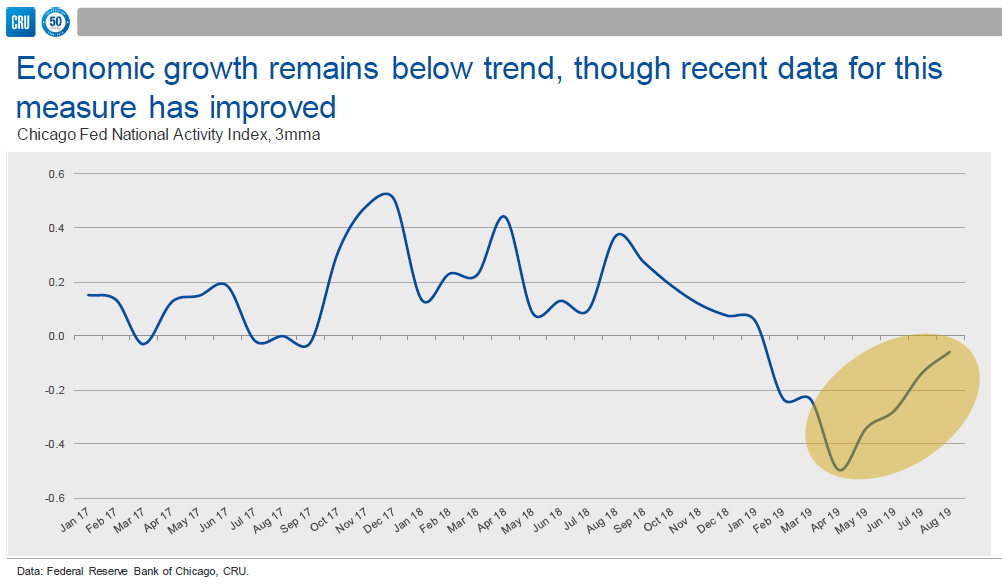

U.S. economic growth was below the historical trend throughout 2019, but has improved since April, according to the Chicago Fed National Activity Index.

Activity in two key steel sectors, fabricated metal products and machinery, showed structural weakness and volatility during the past year. Inventories at service centers have declined since January, but overall have been flat and generally adequate.

Activity in two key steel sectors, fabricated metal products and machinery, showed structural weakness and volatility during the past year. Inventories at service centers have declined since January, but overall have been flat and generally adequate.

Mill lead times for HR, CR and HDG began shortening early in the year with a mild uptick during the summer months before turning lower once again.

The combination of shorter lead times, weaker demand, lower scrap costs and adequate inventories were the drivers behind falling sheet prices in 2019, said Spoores.

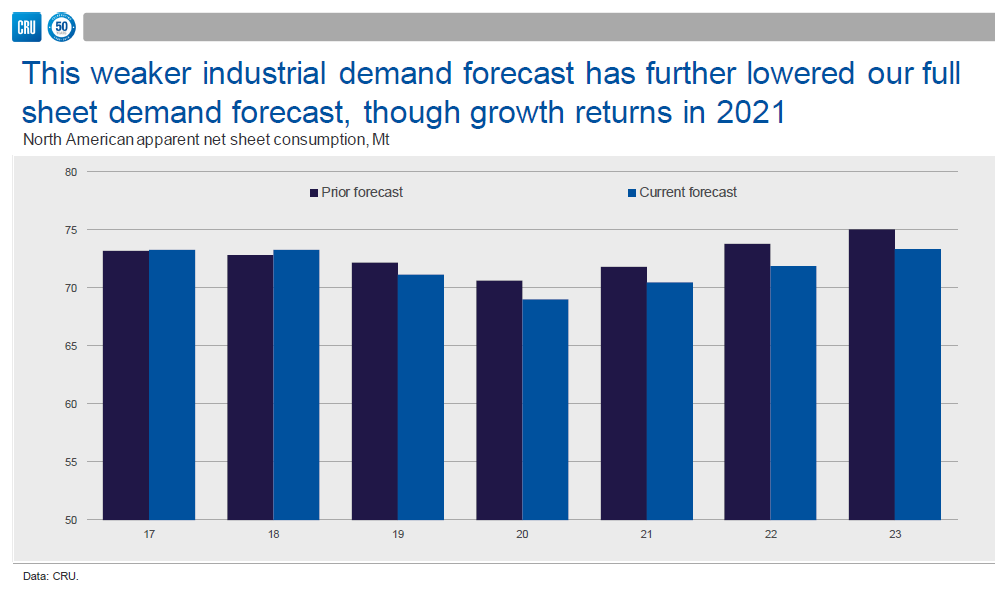

The forecast for industrial production was revised lower by CRU since their Q3 forecast. Lower sheet demand is predicted for this year mainly in the manufacturing and automotive sectors. Demand from the construction sector is still positive and expected to improve in 2020, with all three sectors showing improvement in 2021.

The revised sheet demand forecast calls for a 2.9 percent decline in 2019 and 3 percent in 2020. The good news, said Spoores, is that the industry will see sheet demand bottom in 2020 with a sustained growth rate of about 2 percent starting in 2021 and continuing for 4-5 years.

New capacity is likely to restrain sheet prices from 2021 onward. About 7 million tons of cumulative new EAF capacity is coming online at Big River Steel, Nucor, Steel Dynamics and North Star Bluescope during the next five years. Steel prices are expected to fall with new capacity, but are predicted to remain at a slight premium over global prices.

Factors behind continued price volatility include:

• Slower growth rate of industrial production and increased chance of a recession

• Increased North American HR coil capacity

• Increased competition among steel producers

• Evolution of Section 232 for steel consumers as well as specific countries

• Black Swan (the extreme impact of rare and unpredictable outlier events)

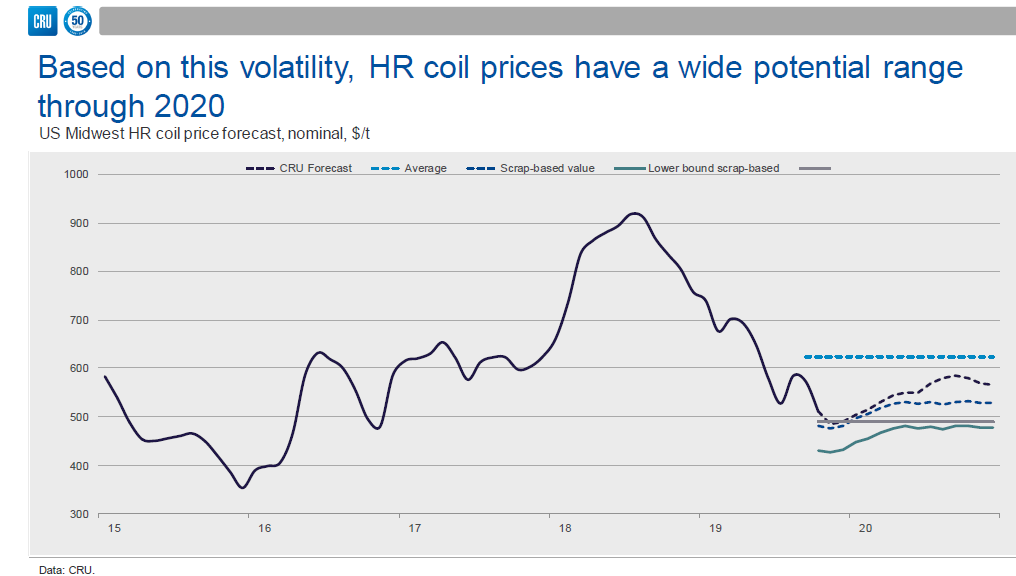

Continued volatility will benefit those companies using CME Futures. CRU’s average annual price for HR coil was $831 in 2018 and 2019 will be closer to $601, said Spoores. CME Futures was pricing in $730 for a period of mid-December 2019. Users of CME Futures could have locked in sales of HR coil at the $730 price rather than selling at the CRU average price of $601.