Analysis

October 22, 2019

Existing Home Sales Slide in September

Written by Sandy Williams

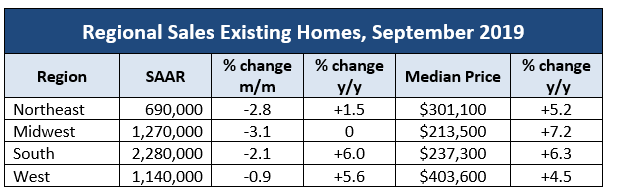

Existing home sales fell 2.2. percent from August to a seasonally adjusted annual rate of 5.38 million in September, says the National Association of Realtors. The decline followed two consecutive months of gain. Sales in the Midwest fell the hardest but all four regions saw declines. Higher home prices due to insufficient inventory was partially to blame, said NAR Chief Economist Lawrence Yun.

“We must continue to beat the drum for more inventory,” said Yun. “Home prices are rising too rapidly because of the housing shortage, and this lack of inventory is preventing home sales growth potential.”

Inventory at the end of September was 1.83 million, unchanged from August and down 2.7 percent from a year ago. Inventory at the end of September stood at a 4.1-month supply at the current sales rate. A healthy inventory supply is considered to be six months.

Single-family home sales fell 2.6 percent from August to a SAAR of 4.78 million, but were 3.9 percent higher than a year ago. Median sales price rose 6.1 percent year-over-year to $275,100 in September

Existing condominium and co-op sales rose 1.7 percent from the previous month to an annual rate of 600,000 units and were 3.4 percent higher than a year ago. The median existing condo price was $248,600, an increase of 4.5 percent from September 2018.