Market Data

October 23, 2019

IMF: “Global Economy is in a Synchronized Slowdown”

Written by Peter Wright

The International Monetary Fund updates its World Economic Outlook in April and October each year. The IMF has increased its forecast of U.S. GDP growth in 2020, but decreased it in each year 2021 through 2023 with no change in 2024.

![]()

The opening statement of the IMF’s WEO, released Oct. 15, begins as follows: “The global economy is in a synchronized slowdown, with growth for 2019 downgraded again—to 3 percent—its slowest pace since the global financial crisis. This is a serious climbdown from 3.8 percent in 2017, when the world was in a synchronized upswing. This subdued growth is a consequence of rising trade barriers; elevated uncertainty surrounding trade and geopolitics; idiosyncratic factors causing macroeconomic strain in several emerging market economies; and structural factors, such as low productivity growth and aging demographics in advanced economies. Global growth in 2020 is projected to improve modestly to 3.4 percent, a downward revision of 0.2 percent from our April projections. However, unlike the synchronized slowdown, this recovery is not broad based and is precarious. Growth for advanced economies is projected to slow to 1.7 percent in 2019 and 2020, while emerging market and developing economies are projected to experience a growth pickup from 3.9 percent in 2019 to 4.6 percent in 2020. About half of this is driven by recoveries or shallower recessions in stressed emerging markets, such as Turkey, Argentina, and Iran, and the rest by recoveries in countries where growth slowed significantly in 2019 relative to 2018, such as Brazil, Mexico, India, Russia, and Saudi Arabia.”

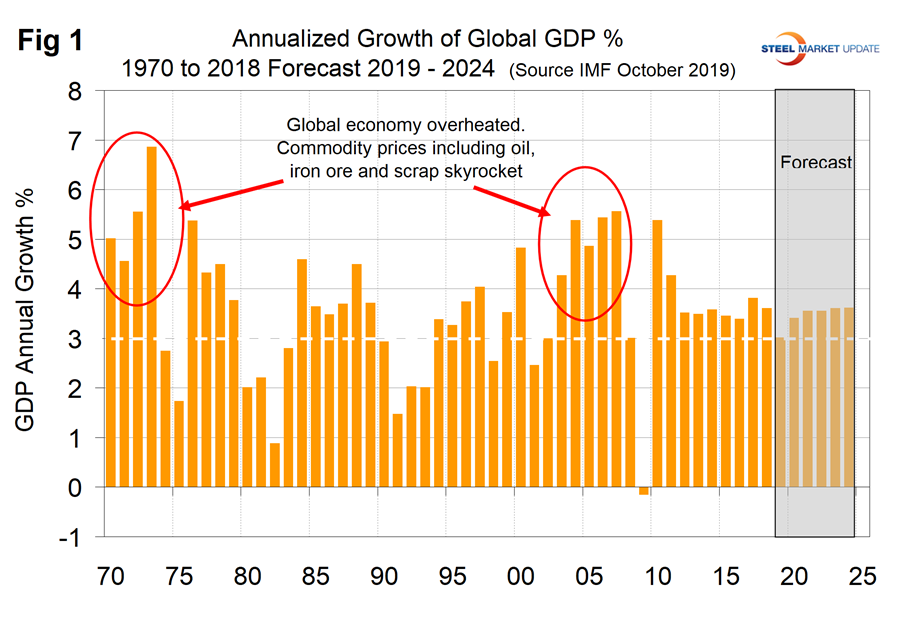

SMU Data Analysis: Figure 1 shows the growth of global GDP since 1970 with this month’s IMF forecast through 2024. We have highlighted the periods of the early 1970s and the mid-2000s when the commodity bubbles prevalent at those times were driven by unusually high and sustained global growth. The collapse of the commodity bubble in the last decade coincided with the U.S. banking and housing crisis setting up the perfect storm. After the rebound in 2010, global growth declined through 2016 and after a two-year improvement is forecast to decline again in 2019.

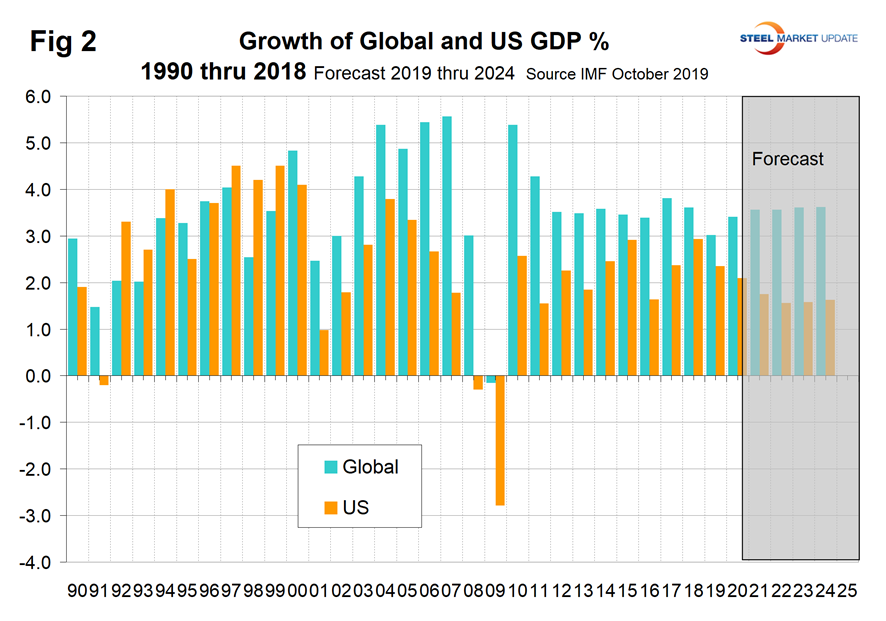

Prior to the 2001 recession, the U.S. held its own in the economic growth stakes, but between 2001 and 2008 growth in the U.S. averaged 1.84 percent less per year than the growth of the global economy as a whole (Figure 2). In the years 2011 through 2018 the gap narrowed to 0.68 percent. The difference is forecast to widen to 2.0 percent in 2024.

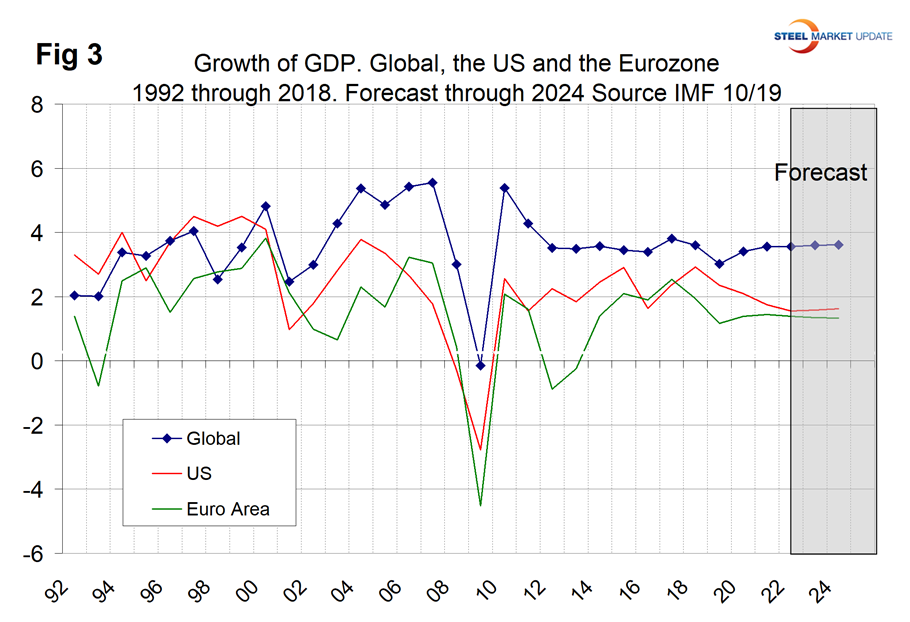

With the exception of 2016, the U.S. has outperformed the Eurozone since 2010 and in the October forecast will continue that trend though 2024 (Figure 3).

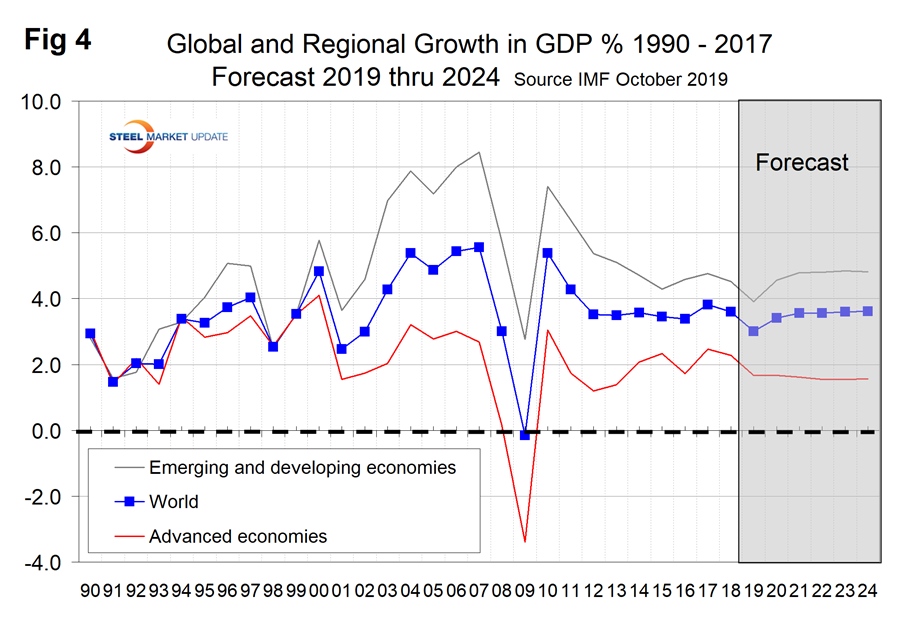

Figure 4 shows the growth comparison between emerging and developing economies and the advanced economies. The gap is projected to widen through 2024.

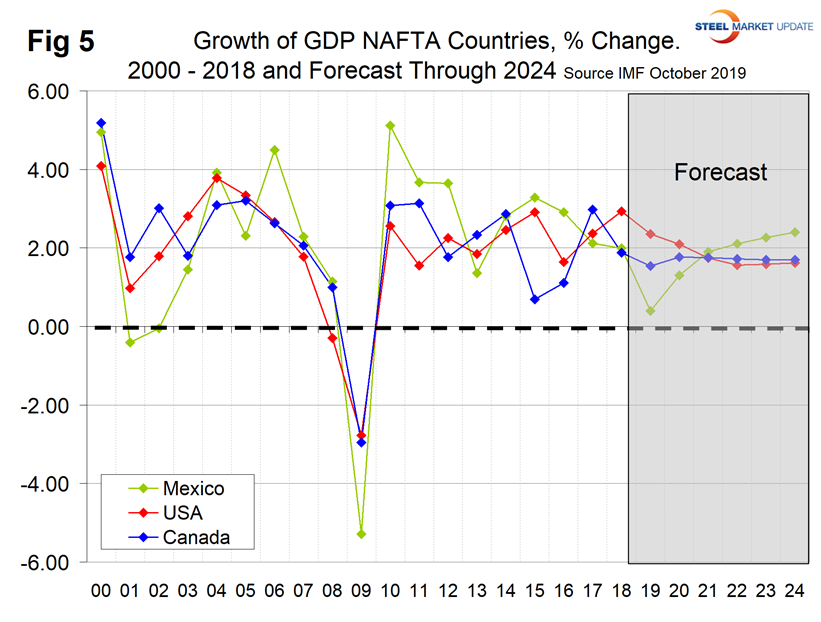

Within NAFTA, the U.S. had the highest growth rate in 2018, which is forecast to continue through 2020. In 2021 the three countries are forecast to have equal growth, then in 2022 Mexico will regain the lead and hold it through 2024 (Figure 5).

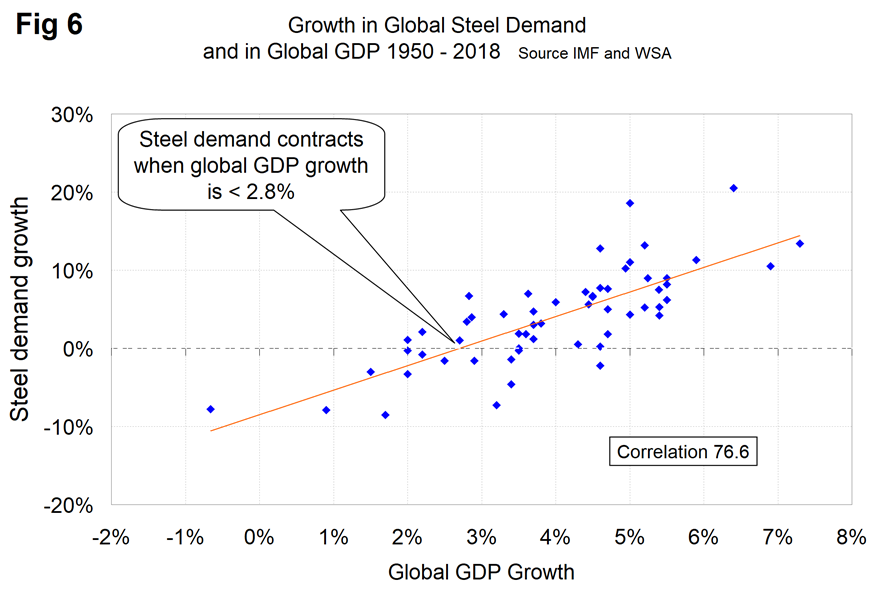

There is a relationship between the growth of GDP and steel demand at both the international and national levels, which also extends to other commodities such as cement. There are two interesting aspects to this relationship. First, the cyclical change in steel demand is vastly more volatile than the change in GDP, which we attribute to manufacturing industries in general being more fragile than service industries and the inventory response throughout the steel supply chain causes a snowball effect. Second, as discovered by our friends at “Steel Guru,” 1 percent growth in GDP does not result in 1 percent growth in steel demand. At the global level it takes a 2.8 percent increase in GDP to get any increase in steel demand (Figure 6). This is a long-term average over a period of 65 years and based on the added volatility of steel can be a predictor of the immediate future. For example, after the disastrous decline in steel demand in 2009 there was no doubt that a huge cyclical rebound would occur as inventory managers throughout the world began to react to the economic recovery. If the IMF forecast proves to be correct, then the growth in global steel demand will average around 3 percent annually through 2024.

The U.S. steel market requires about 2.2 percent growth in GDP to generate growth in steel demand, therefore if current forecasts are accurate, we can expect some growth of steel demand this year, followed by a decline through 2024.