Overseas

January 12, 2020

CRU: Steel Sheet Prices Start 2020 Up; Demand Recovery's in Sight

Written by James Campbell

By CRU Analyst James Campbell, from the Steel Sheet Products Market Outlook

2019 was a bad year for the steel industry. Prices and margins collapsed and, outside of China, demand contracted. However, the combination of a new restocking cycle and reduced output in many markets allowed producers to raise prices and margins at the end of the year, although still below sustainable levels. The outlook for 2020 is brighter. Growth is forecast outside of China, but the improvement is not expected to take hold until the second half of the year. Capacity additions mean it is unlikely that we will see a prolonged period of high margins across the industry as supply additions are expected to outpace demand over the next few years. This is a problem for a steel industry where a drive towards investment intensive decarbonization is beginning.

Prices Find Support from Restocking and Reduced Output

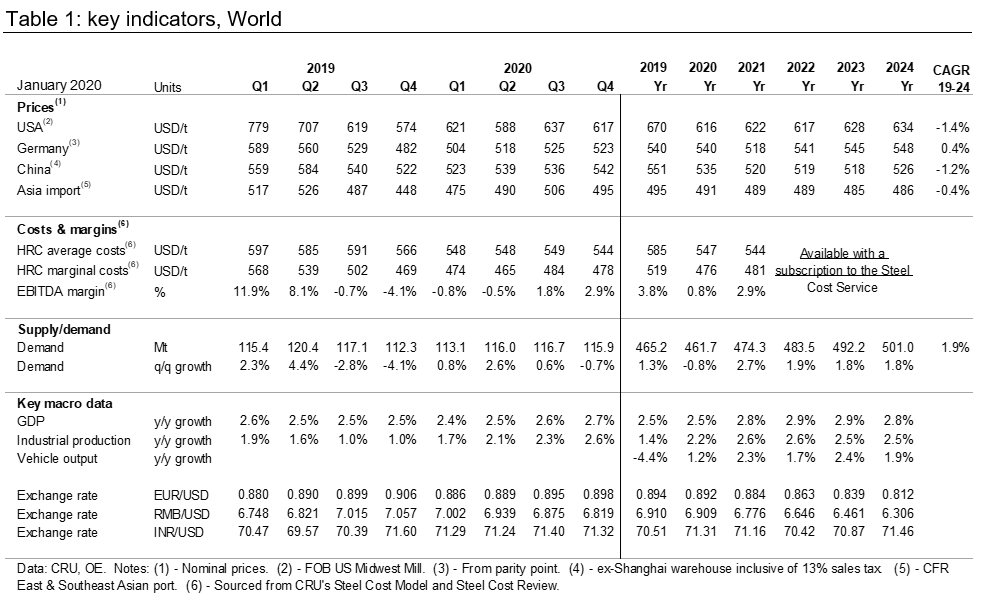

Although global GDP has been robust, growth of industrial production has consistently fallen as the U.S.-China trade war progressed; protectionism has proved to be bad for steel demand. Weaker industrial production and a prolonged destocking cycle have together resulted in lower demand for HR products for both 2019 Q4 and the whole year. In China, demand growth was positive overall, although demand for downstream products was similar to the trend seen in other regions.

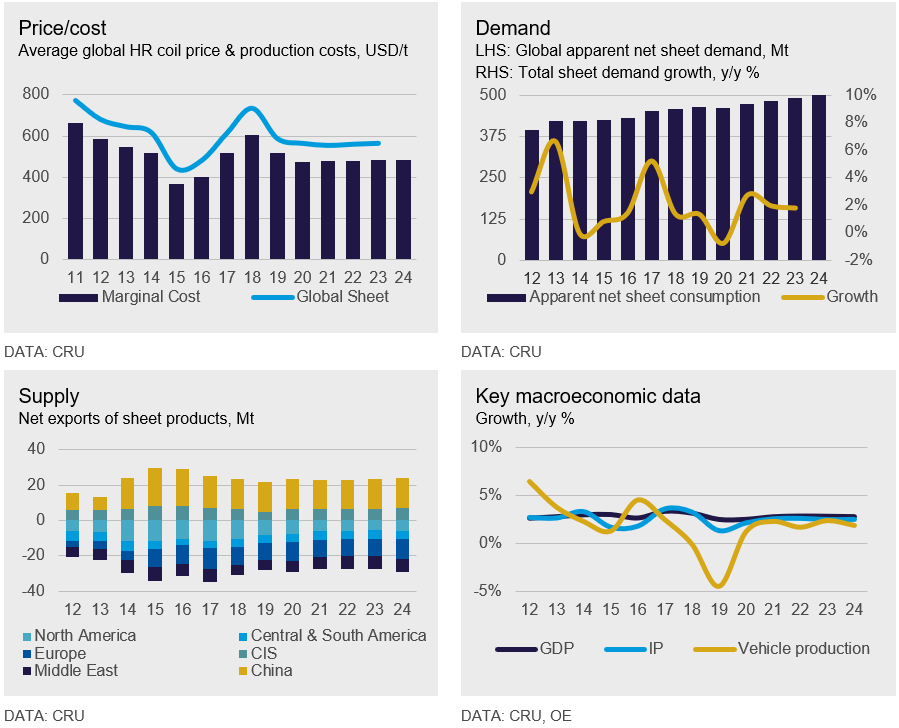

HR coil prices hit a cyclical low point in 2019 Q4, with internationally traded prices coming within $20-30 /t of the variable cost curve floor reached in 2015, before reversing trend in the USA, SE Asia and Europe during November. Prices increased as buyers started restocking. Weaker than expected demand in 2019 resulted in a prolonged destocking cycle. However, by Q4, stocks were too low to support the expected seasonal improvement in demand in 2020 Q1. At the same time, poor orderbooks forced many mills to reduce output during 2019, including the idling of blast furnaces. High cost regions and producers were affected most as they were frozen out of global export markets at a time when domestic demand was low. Several blast furnaces in Europe were idled this year, while other producers in the region reduced output. In South Africa, ArcelorMittal mothballed their Saldanha Bay facility

The combination of a new restocking cycle and reduced output in many markets allowed producers to raise margins, although they remain below desired levels. This has occurred even though underlying demand remains weak. Global industrial production has suffered, falling to growth levels of around 1 percent y/y in 2019 H2, compared with 4 percent y/y growth in 2018 Q1. Developed economies suffered more, with y/y IP changes negative for much of 2019.

Sheet Demand Recovery Expected in 2020 H2

The outlook for 2020 is brighter. Growth is forecast outside of China, but the improvement is not expected to take hold until the second half of the year. Further improvements to growth are forecast for 2021 as the recovery takes hold. In China, lower demand is forecast overall, as we do not expect HR coil demand to be as strong as in 2019. However, demand for downstream products in China is set to rise as output in manufacturing sectors recovers. In the medium-term, Chinese demand is expected to be zero-to-low-growth. We will be keeping a close eye on our medium-term forecast for China this year as 2021 marks the start of a new five-year plan, a key period as China’s economy slows down as it moves from being investment driven to consumption driven.

The recovery in demand during 2020 is coming from a lower base compared to our October outlook. We have downgraded our forecast for industrial production in 2019 and 2020, particularly in the U.S. and Eurozone compared to the previous outlook. For China, there is a small upgrade built into our base case as we expect an assist to mainly come via government spending – this is better for commodities than the tax cut led stimulus in 2019. The improvement in the overall industrial production during 2020 is heavily reliant on growth returning to the automotive sector, something we will cover in an upcoming special feature. Even so, it will take time for output to recover to previous highs.

One outlier in the demand story is India. Following the government stimulus measures last month, there was the announcement of the $1.4 trillion National Infrastructure Pipeline. This program is expected to increase infrastructure spending by 43 percent y/y in financial year 2020-21. With domestic demand prospects much stronger, Indian producers are refocusing on the domestic market, thus reducing the level of exports into the South East Asian markets.

Supply Additions Will Exceed Demand Growth

Industry demand growth is muted at a time supply is growing. Following a period of strong profitability in 2017-18, close to 200 Mt of investments have been announced. We expect capacity to grow faster than demand over the next few years, meaning any improvement to industry margins is going to be limited. Over this period, it is highly unlikely that we will see a prolonged period of high margins across the industry, as seen in 2017-18. A good example of this is in North America, where 7 Mt of new EAF capacity is expected to come onstream over the next five years. Some of this capacity is due to come onstream in 2020 H2. This is expected to intensify competition among domestic steelmakers, even though imports have come down and demand is expected to improve at the same time.

New lower cost capacity is expected, over time, to push higher cost facilities out of the market. Producers will likely reassess the viability of higher cost plants, especially when significant CAPEX is needed, e.g. blast furnaces relines. There is evidence of this already in the USA where U.S. Steel and ArcelorMittal have recently idled facilities that required expensive relines.

Steel Begins a ‘Low-Carb(on)’ Diet

Our outlook for low industry margins over the next five years creates a problem for a steel industry where a drive towards investment intensive is beginning. Climate change is moving up the political agenda and putting increasing pressure on heavy industry to reduce their CO2 emissions. As the largest producer of global industrial CO2 emissions, the steel sector has a clear role to play in meeting emission reduction targets. There are a variety of options available to steelmakers to reduce the CO2 intensity of their steelmaking, but investment, especially in breakthrough technologies, will be expensive.

At the moment, Europe is a hot spot due to carbon pricing and potentially a carbon border tax. Carbon pricing is now impacting the profitability and operating decisions of EU mills.

Global Macro Themes

Decarbonization is only one of the opportunities and challenges for the steel industry to be explored over the next year as part of CRU’s macro themes for 2020. The themes for 2020 are China rebalancing and reform, Environmental and Social Governance and foreign exchange movements.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com