Market Data

January 17, 2020

Currency Update for Steel Trading Nations

Written by Peter Wright

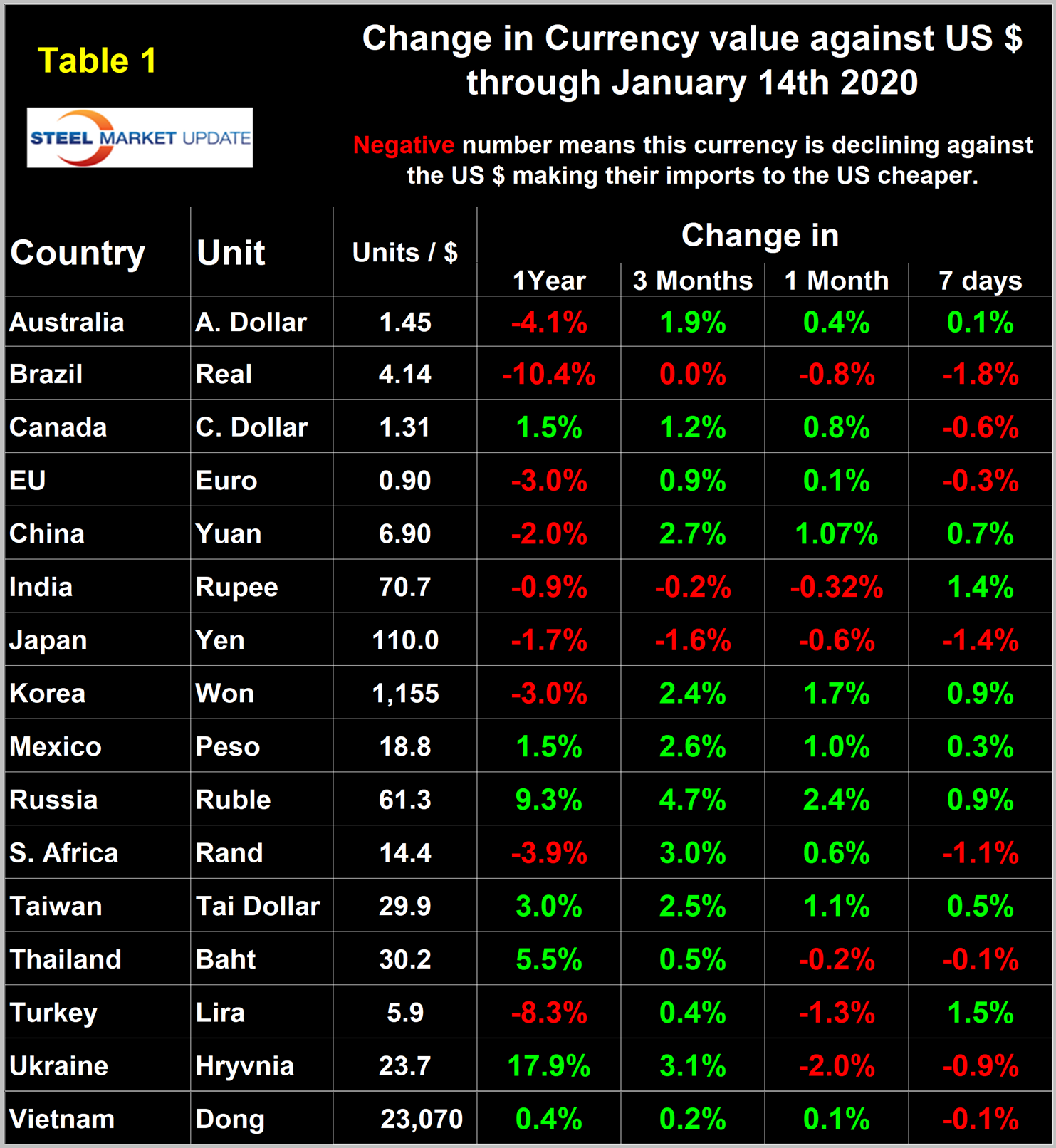

In January, we have replaced the British pound in this report with the Vietnamese dong in recognition that Vietnam is now a much bigger player in the global steel market than is the UK.

The U.S. dollar has strengthened against 13 of the 16 steel trading nation currencies in the last three months.

In this report, we examine the change in currency values of the 16 pre-eminent global steel and iron ore trading nations. The currencies of these 16 don’t necessarily follow the Broad Index value of the U.S, dollar. In fact, at any given time, some are always moving in the opposite direction. The latest value of the Broad Index as published by the Federal Reserve was Jan. 10. In the three months prior to that date, the dollar had weakened by 0.7 percent, therefore in this instance the currencies of the steel trading nations are not coincident with the Broad Index.

![]()

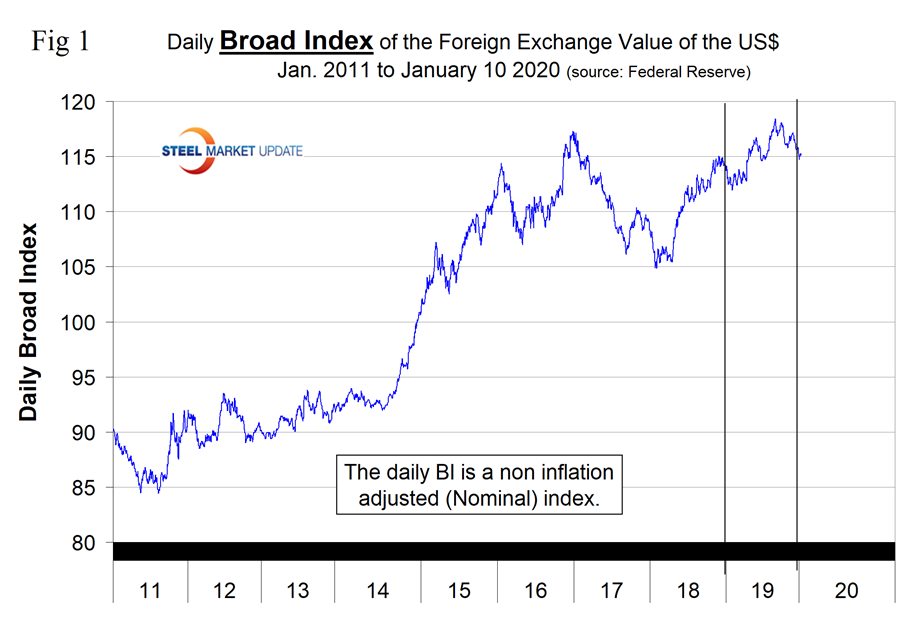

Figure 1 plots the daily Broad Index (BI) value of the U.S. dollar since 2011. The dollar appreciated erratically in 2019 through Sept. 3 when it began to decline, and since that date through Jan. 10 was down by 2.8 percent.

At Steel Market Update, we track the currencies of 16 steel trading nations. Table 1 shows the number of currency units that it takes to buy one U.S. dollar and the percentage change in the last year, three months, one month and seven days. The overall picture for the steel trading nations is that in the last year the U.S. dollar has weakened against nine of the 16. In the last three months, the dollar has strengthened against 13, in the last month has strengthened against 10, and in the seven days prior to Jan. 14 it strengthened against eight. Table 1 is color coded to indicate weakening of the dollar in green and strengthening in red. We regard strengthening of the U.S. dollar as negative and weakening as positive because of the effect on net imports. Figure 2 shows the extreme gyrations that have occurred at the three-month level in the last four years.

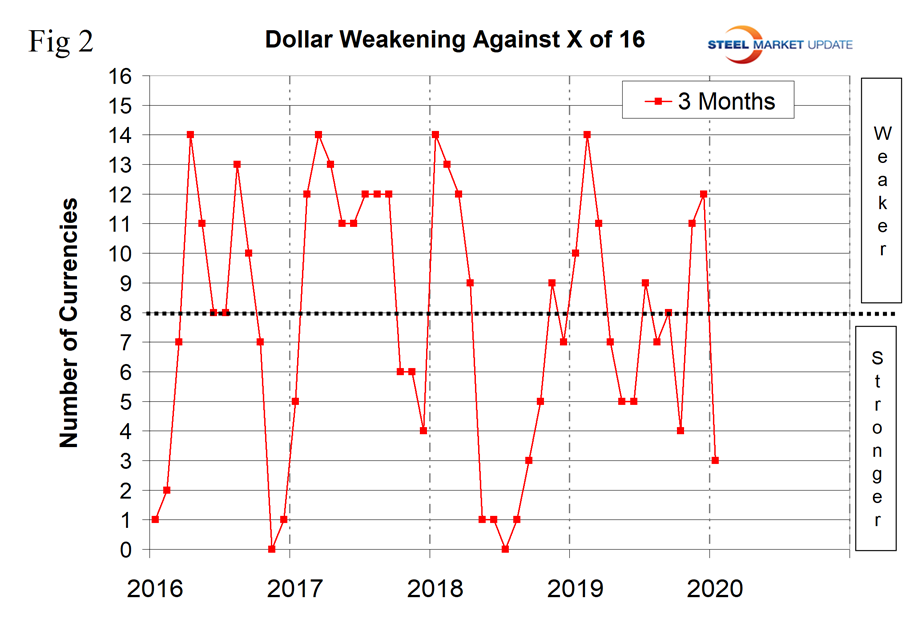

To try to get a less volatile look at the changes in value of the 16 currencies under examination here we have developed Figure 3. This shows the number of currencies against which the dollar was weakening on a year-over-year basis. In March and April, the dollar was strengthening against all 16, but by mid-January it was only strengthening against seven.

There were no wild gyrations of individual currencies in the last three months. The biggest gainer was the Russian ruble at plus 4.7 percent and the biggest loser was the Japanese yen at minus 1.6 percent. We present long-term charts of the value of these two currencies against the dollar in this update together with external comments on the Vietnamese dong, the Australian dollar and the euro (see the end of this report for details of data sources).

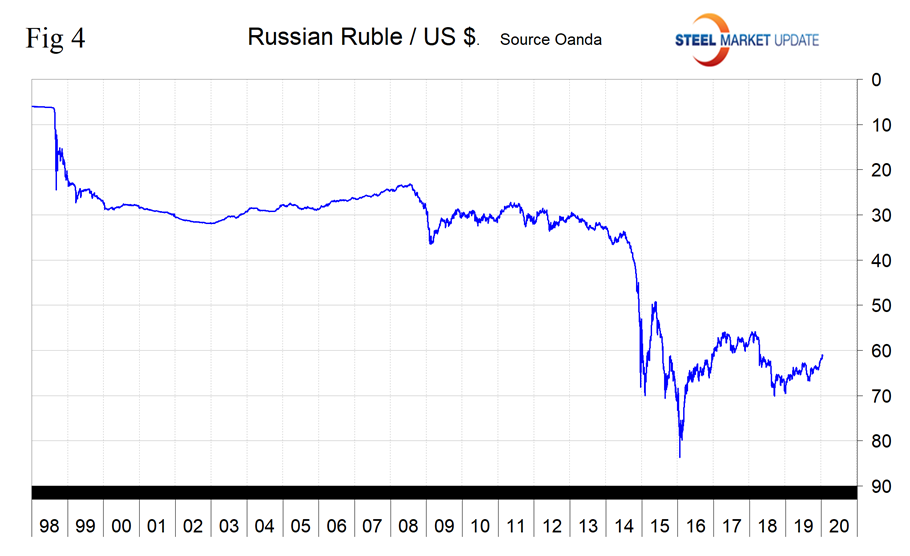

Russian Ruble

The Russian ruble has appreciated by 9.3 percent in one year, by 4.7 percent in three months and by 2.4 percent in one month. Figure 4 shows the history of the ruble valuation against the dollar since 1998.

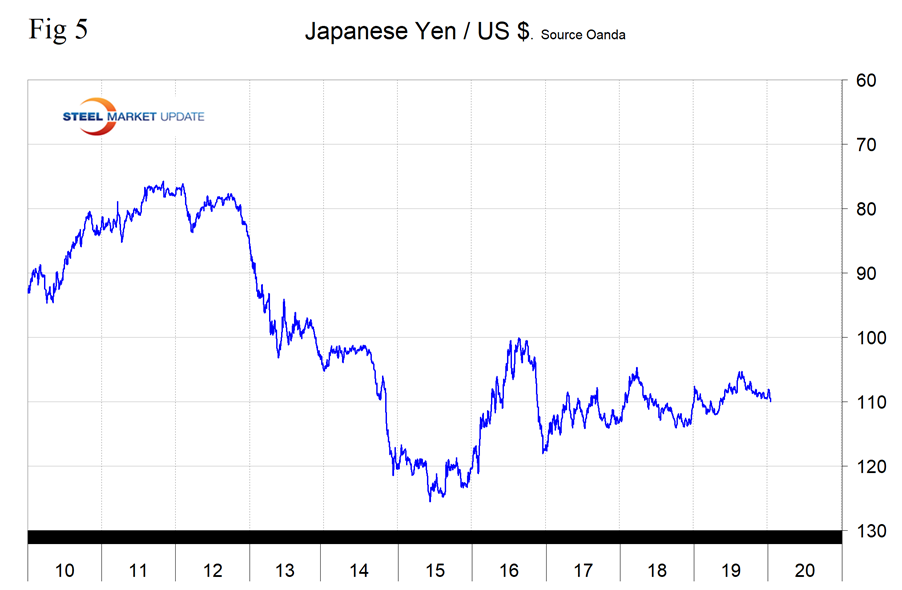

Japanese Yen

The Japanese yen has depreciated by 1.6 percent in the last three months and is 1.7 percent lower than on Jan. 14 of last year. Figure 5 shows the history of the yen value since 2010.

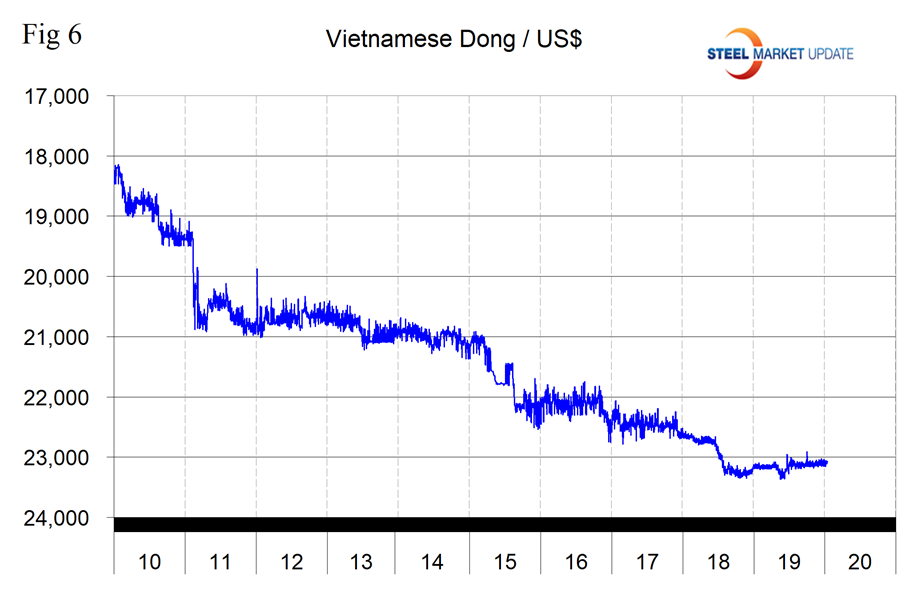

The Vietnamese Dong

Through November, Vietnam shipped over twice as much steel to the U.S. as did the UK. Steel exports generated US$1.93 billion in the first seven months of 2019, with the U.S. remaining the largest importer of Vietnamese steel products, NhanDan Online reports. The figure is up 14.7 percent compared with the same period of 2018, according to the General Department of Customs. Steel exports in July alone rose 4.7 percent after three consecutive months of declines. Steel exports to the world’s largest economy reached US$378.31 million, accounting for nearly one fifth of Vietnam’s total steel exports, followed by shipments to Japan, India, Thailand and the Republic of Korea. In addition to the U.S. and Asian countries, Vietnam’s steel exports to Europe also posted strong growth in the first seven months of 2019, with exports to Sweden shooting up by 206.85 percent. Exports to Norway and the United Kingdom also saw substantial gains. In the meantime, Vietnam’s steel exports to Myanmar recorded the largest decrease, plummeting 49.53 percent from the same period last year to US$33.39 million.

The Vietnamese dong has been very stable against the dollar for over a year. Figure 6 shows the history of the dong since 2010. In the last 12 months, the dong has appreciated by 0.4 percent and by 0.2 percent in the last three months.

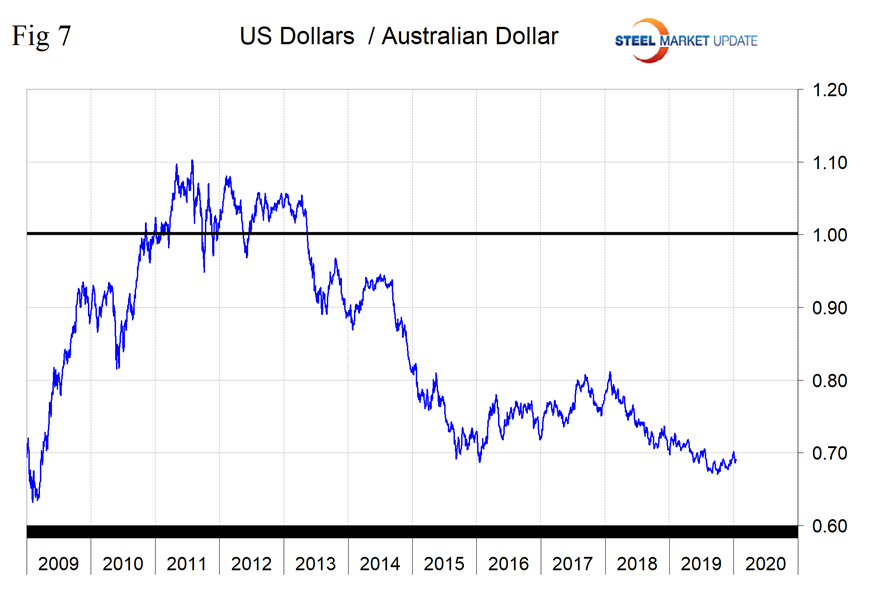

The Australian Dollar

On Dec. 12, the IMF published its Staff Concluding Statement of the 2019 Article IV Consultation Mission. An extract is as follows: “Growth should continue to recover at a gradual pace. Following growth of about 1.8 percent in 2019, the economy is expected to expand by 2.2 percent in 2020. Private domestic demand is expected to recover slowly, supported by monetary policy easing and the personal income tax cuts. An incipient recovery in mining investment is also expected to contribute to growth. Non-mining business investment is expected to take longer to recover. Over the medium term, growth is expected to reach the mission’s estimate of potential growth of about 2½ percent, supported by infrastructure spending and structural reforms. With continued labor market slack, underlying inflation will likely stay below the target range until 2021.”

The Australian dollar has appreciated by 1.9 percent in the last three months and by 0.4 percent in the last month. Figure 7 shows the history of the Ausie since 2009.

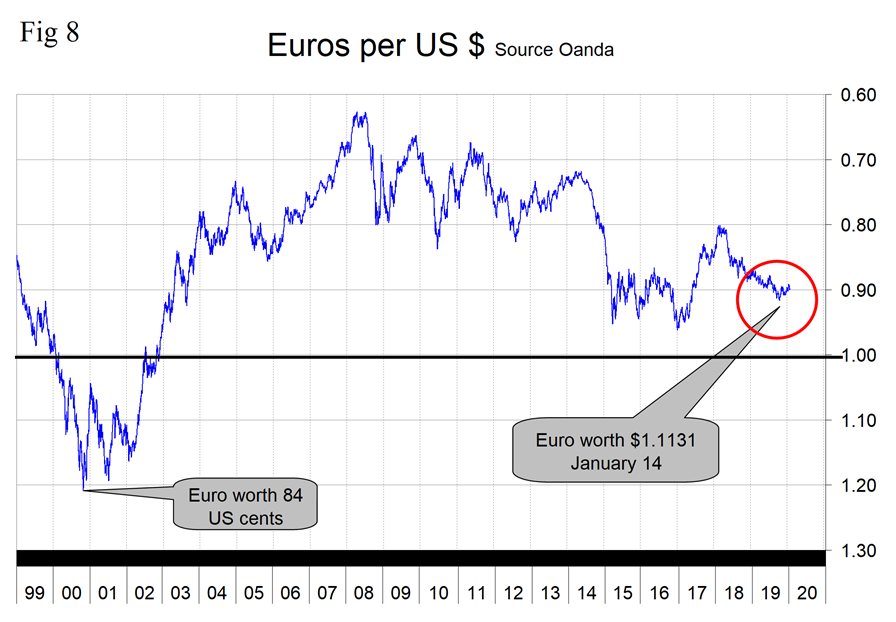

The Euro

On Jan. 10, Andrew Hecht of the Hecht Commodity Report wrote: “Prime Minister Johnson’s impressive victory in the UK election means he has enough support in the Parliament to finally meet a Brexit deadline, which is at the end of January. Brexit with a deal removes a great deal of uncertainty from both the UK and EU economies, which will take the pressure off the European Central Bank. At the same time, both the British pound and the euro have moved higher in the aftermath of the UK election. The price action in the currencies is a sign that calm has returned, and the threat of a hard exit is off the table for good. In his last months at the helm of the ECB, Mario Draghi cut the deposit rate by 10 points to the negative 50 level and restarted quantitative easing to the tune of 20 billion euros per month. At the end of his term in late 2019, he handed the ECB over to Christine Lagarde, the former managing director of the International Monetary Fund. While Mr. Draghi’s legacy is as a monetary policy dove, Ms. Lagarde recently said, ‘I’m neither a dove nor a hawk. My ambition is to be an owl.’ She noted that owls are associated with a little bit of wisdom. In some of her first comments at the end of 2019, it appears she will encourage the European Union to take steps to increase fiscal stimulus to replace some of the monetary policies followed by the ECB since 2008. However, time will tell if the political and economic landscapes in Europe allow her to be less of a monetary policy dove than her predecessor.”

The euro is down by 3.0 percent year over year, but in the last three months has appreciated by 0.9 percent. Figure 8 shows the history of the euro since its inception in 1999.

In this monthly analysis we show the trends we think have the most immediate significance, but all 16 steel trading nation graphs are available on request.

Explanation of Data Sources: The Broad Index is published by the Federal Reserve on both a daily and monthly basis. It is a weighted average of the foreign exchange values of the U.S. dollar against the currencies of a large group of major U.S. trading partners. The index weights, which change over time, are derived from U.S. export shares and from U.S. and foreign import shares. The data are noon buying rates in New York for cable transfers payable in the listed currencies. At SMU we use the historical exchange rates published in the Oanda Forex trading platform to track the currency value of the U.S. dollar against that of 16 steel trading nations. Oanda operates within the guidelines of six major regulatory authorities around the world and provides access to over 70 currency pairs. Approximately $4 trillion U.S. dollars are traded every day on foreign exchange markets.