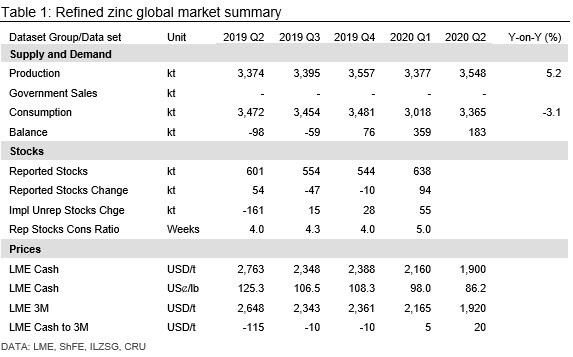

Prices

March 19, 2020

CRU: Zinc’s Price in Freefall as Covid-19 Lockdowns Spiral

Written by Helen O’Cleary

By CRU Senior Analyst Helen O’Cleary, from CRU’s Zinc Monitor

The LME is preparing to move from trading in the ring to electronic settlement pricing as the UK ramps up Covid-19 restrictions on all but essential activities and LME prices continue to take a hammering. While Chinese demand is gradually recovering from the Q1 shock of virus-related lockdowns, the worst impact of demand destruction in most of the rest of the world will be felt in Q2.

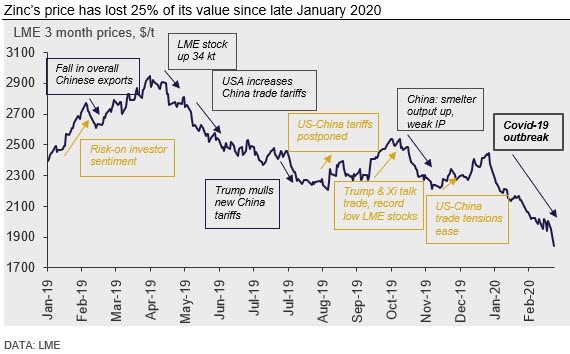

Zinc’s price has fared slightly worse than the average of the rest of the LME metals, losing more than $600/t (25 percent of its value) by March 18 since hitting a year-to-date high of $2,450/t on Jan. 22.

We are now seeing price levels that we were not expecting to see until 2022, when we were forecasting very low prices to bring about supply-side cutbacks necessary to rebalance surplus markets. Investors are now punishing zinc for its weak market fundamentals amid fears that the demand destruction witnessed in China in Q1 will hit much of the rest of the world in Q2.

Zinc’s price had already been pressured lower at the end of 2019 as it became clear that the majority of Chinese smelters were able to sustain operations at high utilization rates against a backdrop of weak demand growth. This gave credence to forecasts of a decisive switch from a refined deficit to surplus in 2020. As Chinese smelters generally build raw material stocks ahead of the New Year holiday, many were able to continue operating even as the Covid-19 outbreak began to prevent manufacturers from restarting. As a result, reported stocks and stocks in other warehouses and at smelters have surged. Although we expect Chinese demand to rebound in Q2, we have revised down our full-year demand forecast. We therefore expect the Chinese market to require less refined metal imports this year, suggesting that more of the global metal surplus will remain in the world ex-China.

The impact of the outbreak on economic activity is not limited to China. Neighboring countries with the closest trade links are being hit not only by the knock-on effects of demand destruction in China but by their own Covid-19 quarantines. While infection rates are stabilizing in South Korea, they continue to rise in Europe and North America, with governments taking action to try and slow the spread of the virus and mitigate the economic shock. Given that Chinese refined demand accounts for 48 percent of global demand, signs that it is beginning to recover would normally be positive for prices, but the unfolding crisis in the rest of the world will act as a drag. Our revised expectation for prices to average $1,920/t in Q2 could be over-optimistic if fundamentals continue to be overwhelmed by mass panic.

The Global Financial Crisis Gives Some Clues as to Market Impact

Our initial downgrade of Chinese refined demand in response to the Covid-19 outbreak was looking at China in isolation, with the proviso that knock-on effects could disrupt economies elsewhere. The World Health Organization started referring to the outbreak as a pandemic earlier this month and the fallout is only now becoming clear as countries across the world impose drastic restrictions on movement and interaction which, quite apart from the social cost to the most vulnerable, will have a devastating economic impact. In such cases we generally look to previous economic shocks to try to assess how markets might behave, but we are in uncharted territory with Covid-19.

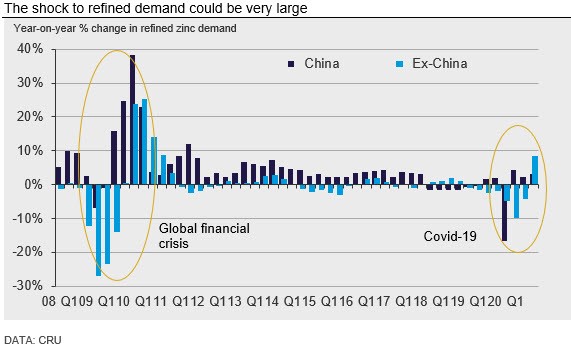

China played a crucial role in the recovery of the zinc market following the global financial crisis as it was on a double-digit growth path and able to absorb much of the world’s excess metal (China’s net refined zinc imports surged from 111kt in 2008 to 641kt in 2009). China still requires refined net imports, but we were expecting it to become less reliant on imports this year and going forward even before the Covid-19 outbreak led to a surge in refined stocks and downward revisions to our 2020 demand forecast. The current crisis follows a year of marginal demand growth in China in 2019 and the expectation of only modest growth going forward. With China’s focus now on economic rebalancing and environmental issues, we cannot expect a rebound in activity there to have the same impact as it had after the global financial crisis. Activity is already beginning to pick up in China and the government continues to announce measures to kick-start the economy after the demand destruction caused by the lockdown. However, the government has so far resisted large-scale stimulus and recently said that it will not be offering any short-term stimulus to the real estate sector.

The impact on the rest of the world is only just beginning to be felt, but we are currently factoring into our forecasts a demand shock in Q2, followed by a more modest contraction in Q3 and a rebound in Q4. On the supply side we are expecting the impact to be less severe, but news this week of a two-week shutdown at several zinc mines in Peru and a reduction in output at Nexa’s Cajamarquilla smelter of 50 percent in reaction to this suggests that we will be revising refined output numbers lower in the coming weeks and months.

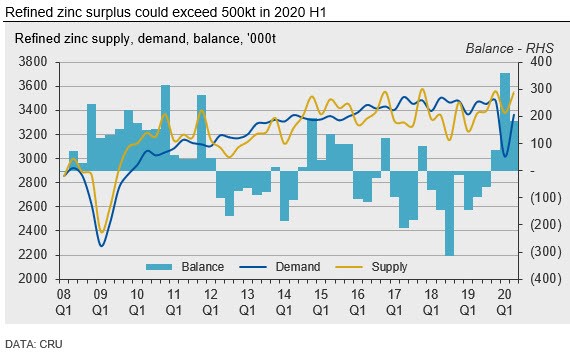

China’s Refined Market Surplus Surged in 20 Q1

China’s refined output swamped demand in 20 Q1 as smelters continued to operate in the face of the collapse in demand. Despite the slump in zinc’s price, high TCs enabled producers to continue operating profitably. This inevitably led to a surge in China’s refined stocks and a large surplus in Q1. We believe that the impact of the outbreak in the world ex-China was smaller in Q1 (with the exception of China’s close neighbors) but expect a similar pattern to emerge in ex-China in Q2. The impact of lockdowns in Europe and the USA has yet to be fully felt and the scale and speed of the disruption to come is hard to define. We are currently assuming that we will see declines in ex-China demand in Q2 of a similar magnitude to those in China in Q1, but expect to make significant revisions in the coming months.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com