Market Data

March 22, 2020

SMU Market Trends: Buyers Remain Hopeful About Demand, Pricing

Written by Tim Triplett

News on the spread of the coronavirus changes by the hour, which effects the outlook of steel buyers. But as of early this past week, based on Steel Market Update’s canvass of the market, the steel sector appears to have weathered the worst of the bad news so far.

Steel Prices

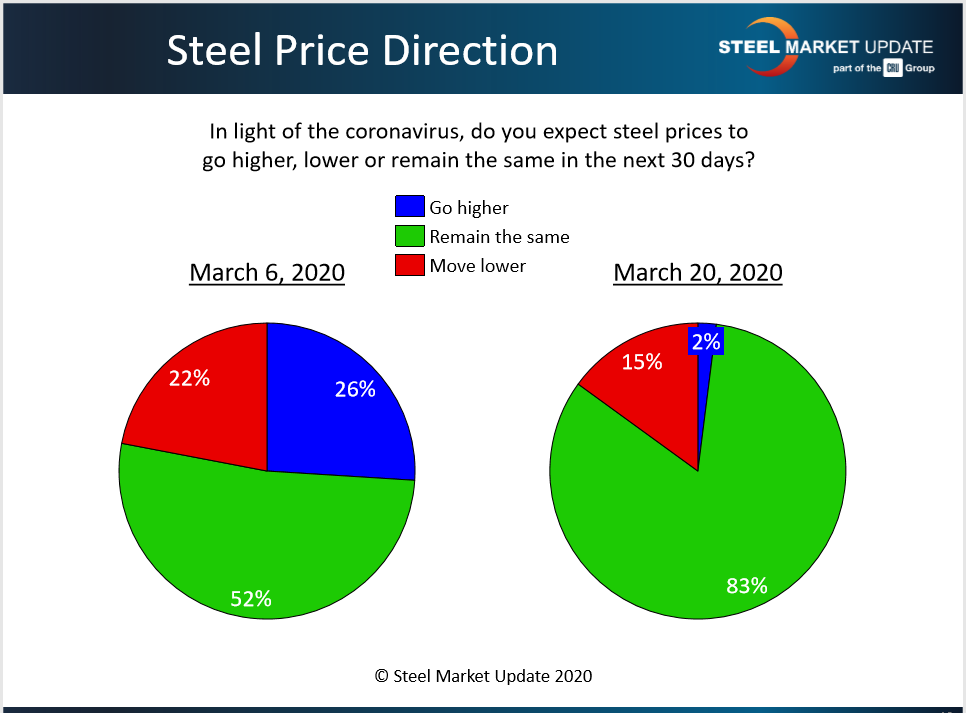

Most executives responding to SMU’s questionnaire this week said they expected steel prices to remain stable in the next 30 days.

SMU asked: Do you expect steel prices to go higher, lower or remain the same in the next 30 days? About 83 percent said they anticipate prices remaining the same, while just 15 percent predicted prices would decline in light of the coronavirus’ effect on the market.

Here’s what some respondents had to say:

“Prices will remain the same to slightly lower based on the market, but more importantly desperate ‘need-based’ selling by service centers.”

“Pretty easy answer on this one…lower!”

“Distribution inventories are beginning to get replenished only as per order receipt (i.e. one ton out = one ton in). Hedge buys are rare but may exist if pricing is lucrative.”

“I would think demand will decrease thus lowering prices.”

“Prices are supply/demand/raw material costs related. Raw material costs are flat to down. Supply will be stable or tighter with domestic cutbacks. Demand so far is stable, but we anticipate cutbacks. Uncertainty will slow buying and thus less demand and lower prices.”

“We think prices will move sharply lower if manufacturing is impacted.”

“Who really knows? So many different things could happen to send prices in either direction.”

“I’m surprised how resilient the global steel market has been.”

Steel Demand

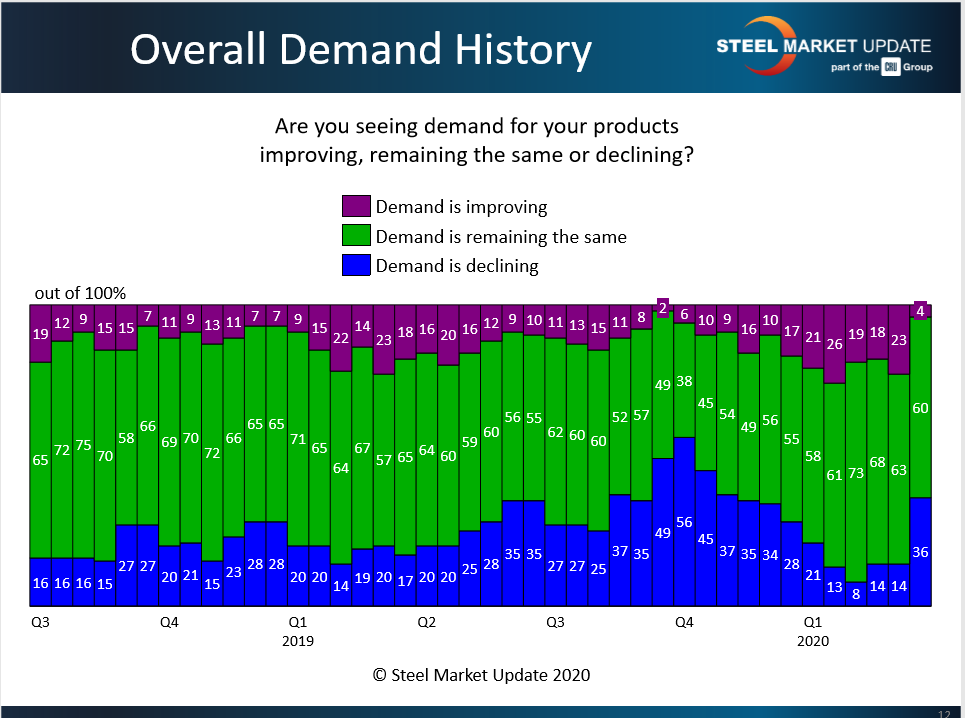

Despite the disruptions to commerce as a result of the virus, the majority of steel buyers polled by SMU this past week expect demand for steel products to remain about the same.

SMU asked: Are you seeing demand for your products improving, remaining the same or declining? About two-thirds expect the same or better, while only one-third see demand declining.

Here’s what some respondents had to say:

“Surprisingly, we have seen little to no change to our activity levels.”

“OK for right now, but we expect a decline to occur very soon.”

“So far we are staying steady.”

“As of right now we are having a great March, but I don’t expect that to last much longer.”

“At this time demand looks steady. Next week or so will be the telling tale.”

“March business is down 30 percent.”

“Fear of the unknown.”

Holes in Mill Order Books?

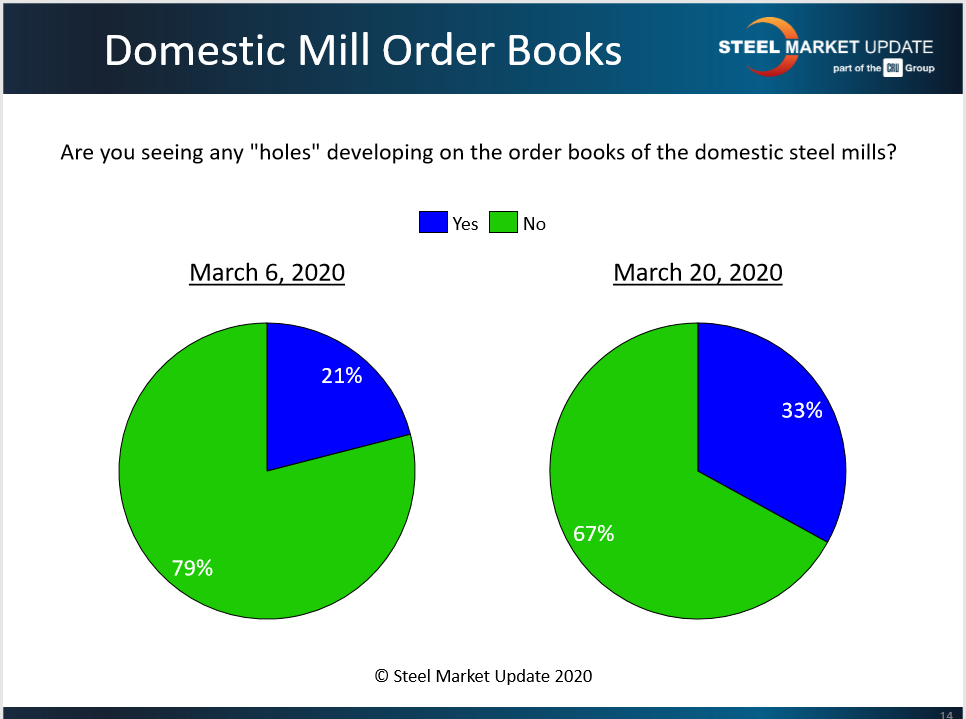

The latest AISI data shows domestic steelmakers still producing at more than 80 percent capacity. Steel buyers confirm the surprisingly robust production.

SMU asked: Are you seeing any holes developing in mill order books? Sixty-seven percent said no.

Here’s what some respondents had to say:

“No holes yet.”

“No holes yet but that will change quickly now that the UAW has forced a shutdown.”

“In the plate world, steel mills speak confidently, but there is a nervousness about the near future.”

“OCTG orders at mills are being cancelled.”

“JIT plate stock is dwindling quickly.”

“I see domestic mill order books strong. Maybe CRC is weaker, but not any holes so far.”

“Mills have not shown their hand, playing it close to the vest.”

“Through May is good; June and beyond is an unknown.”

“Some maintenance is being cancelled.”

“You’ll see more cancellations soon.”

Rethinking Inventory?

Steel buyers are taking a hard look at their inventory levels, though the unprecedented market conditions make future demand virtually impossible to predict.

SMU asked: Given the current market conditions are you rethinking your inventory strategy? About 56 percent are reconsidering their inventory and purchasing plans, while 44 percent are staying the course, at least so far.

Here’s what some respondents had to say:

“We’re expecting a slowdown for a couple of months.”

“Trying to clear the shelves in order to make room for cheaper steel.”

“Planning for lower prices.”

“We continue to focus on turns.”

“May hold less inventory.”

“About 6 to 8 weeks of inventory has always been the plan.”

“Will transition to running leaner.”

“We try to keep three months on hand. The market was shaky before this all started, it will be hard for the mills to hold up prices if things continue to digress, like scrap, iron ore and zinc. I only want to buy what I absolutely need. I felt the market would soften after the second quarter; I think it will be sooner now.”

“We’re holding off on placing any new orders and looking to see if it’s possible to cancel some.”

“If you aren’t rethinking your inventory, you won’t be around very long.”

Manufacturing Demand

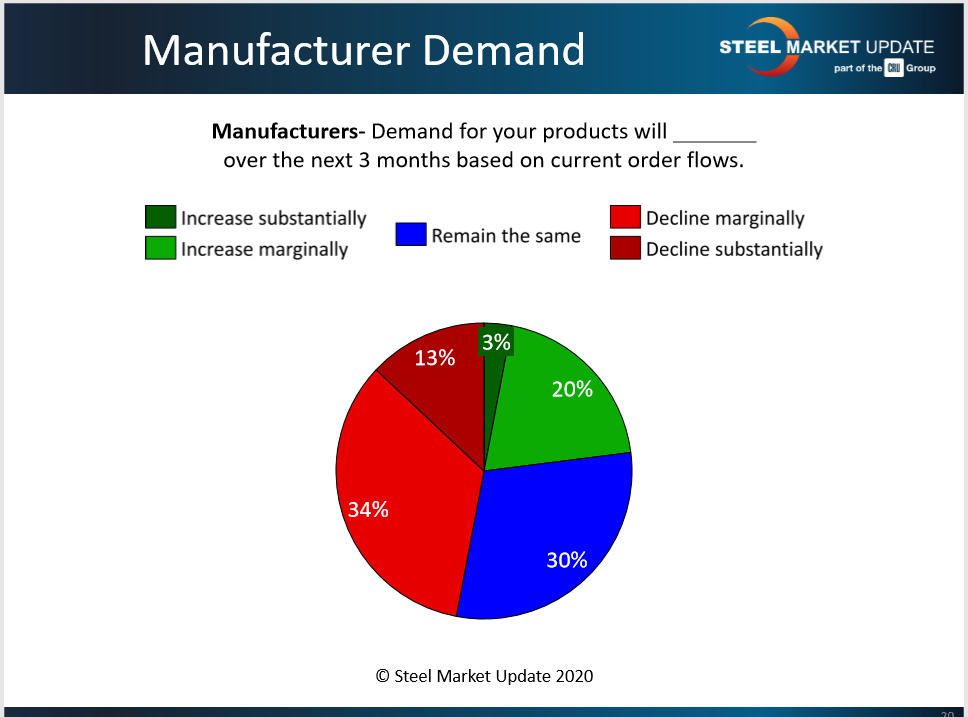

Steel prices moving forward will depend in large part on how well manufacturing survives all the measures taken to stem the spread of COVID-19. Manufacturers responding to SMU’s questionnaire this week were surprisingly positive, given all the negative headlines. Two out of three expect demand to remain the same or decline only marginally in the coming weeks. Another 23 percent predict demand to actually improve. Only 13 percent of manufacturers predicted a substantial decline in their business—at least as of March 16-17.

Here’s what some respondents had to say:

“We’re hoping for a marginal decline…and hoping against a 2008/2009 type of fallout.”

“We are a basic industry that the public can’t do without.”

“Normally our business increases from February through July. Orders have held up so far, but who knows what comes next if retail businesses shut down.”

“No idea.”