Prices

April 9, 2020

CRU: Global Metallics Prices Fall Amid Decline in Steel Demand

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Metallics Monitor

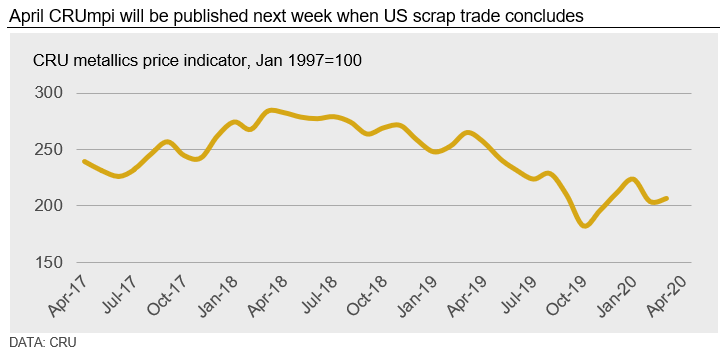

The CRU metallics price indicator (CRUmpi) will be updated following the conclusion of trade in the U.S. However, we expect the indicator to move substantially lower following price decreases across every market we track.

Metallics prices in nearly every market came under substantial pressure in April from evaporating steel demand caused by the Covid-19 pandemic. Price declines in Europe and the U.S. were somewhat mitigated as measures to control the spread of the virus crimped supply. In Turkey, this supply squeeze resulted in buyers lifting imported prices in early April. China was a market with one of the most notable price decreases as processors sought to liquidate inventories, while prices elsewhere in Asia fell as lockdown measures hampered manufacturing and construction activity.

In Europe, scrap prices fell by €20–30 /t m/m. In the south, the Italian market came to a standstill as stringent pandemic countermeasures shut down the economy and trade became illiquid. In contrast, areas like Germany continued to operate more normally, and mills were able to increase margins with the decline in competition by reducing scrap prices while raising prices for finished steel products. In the U.S., trade negotiations have dragged out as dealers try to resist attempts from mills to lower prices by $30-50 /l.ton given supply limitations. As a result, we have delayed our price assessment for scrap in the country.

Tightness in both the U.S. and European markets was exposed by rapidly increasing scrap import prices in Turkey. After Turkish buyers managed to secure material at just below $210 /t CFR for HMS 80:20 in late-March and early-April, it soon became apparent that supply was dwindling. With exporters rejecting prices at that level amid limited availability, Turkish buyers eventually increased import prices by $20-30 /t. This uplift has both created somewhat more bullish sentiment among scrap sellers in Europe and deterred some U.S. dealers from entering a down domestic market.

In Russia, a domestic price decrease was brought about by seasonal factors given the limited impact of Covid-19 on the country so far. With the weather becoming more mild, domestic mills in all regions were able to lower prices given their ability to maintain sufficient material flows.

Ample supply also led Chinese scrap prices to fall substantially m/m, as processors and traders began to liquidate inventories that had built up prior to the Chinese New Year holiday. Even as EAFs restart, some mills were able to lower their buying prices five or six separate times throughout April as businesses returned to normal and the market loosened.

In other parts of Asia, the pandemic continues to smother steel demand and scrap prices along with it. A notable decrease in billet trading throughout Southeast Asia was one sign of the significant slowdown in demand. Meanwhile, increased competition among U.S., Russian and Japanese exporters helped accelerate the decline in scrap prices.

Pig iron prices were also impacted by a reduction in global steel output. While Chinese buying activity has helped raise pig iron prices in recent months, these buyers are now stepping away from the market in favor of lower-priced domestic scrap. Even so, constrained prime grade scrap availability in the U.S., and to a lesser extent Europe, may help buoy pig iron demand.

Outlook: Subdued Demand to Continue in the Near Term

With international steel output hampered by the pandemic, we expect demand weakness for metallics to persist in the near term. For markets like the U.S. and Europe, the direction of scrap prices will be dictated by whether supply reductions outpace swiftly declining demand. Either way, risks mostly remain to the downside for metallics in both markets until their economies return to a more normal state, and any potential price upswings will be limited.

As businesses resume operations in parts of Asia, the downside risk for steel prices comes from depressed demand elsewhere in the world. By extension, should economies like China recover slowly and steel demand be weaker-than-expected, metallics prices could languish for at least another quarter.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com