Analysis

April 13, 2020

Final Thoughts

Written by John Packard

2020 is NOT 2008 all over again…

I vividly remember 2008 and what happened to the steel industry beginning in September of that year.

Why?

Because Steel Market Update began as a company in August 2008 and I was scrambling to get members, while at the same time reporting on the destruction of demand and its impact on the steel industry.

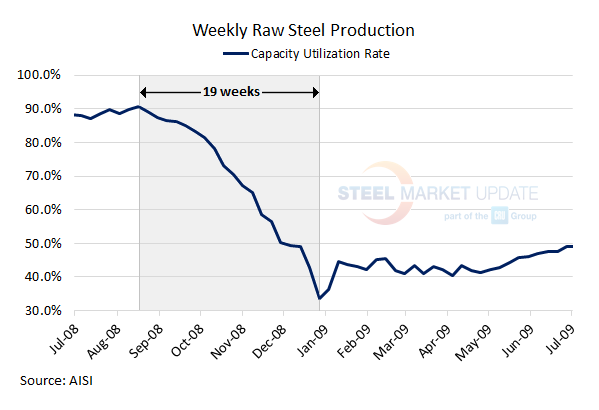

In my opinion, 2020 is not anything like 2008/2009. One key difference is the strength of the economy. In early 2008 we had a tremendous run up in prices (a ridiculous run up as benchmark hot rolled exceeded $1,000 per ton) and service centers built huge inventories. At the same time, the housing market had already begun to collapse in late 2007. As you can see by the graphic below, the domestic steel mills were pumping out high-priced steel like crazy in August.

The market crashed at the end of September 2008.

It took 19 weeks from the cycle peak in late August until the bottom in late December. We went from 90.8 percent operating rates the week of Aug. 16 down to 33.5 percent the last week of December (week of Dec. 27).

As the graphic shows, the market “bounced” back to rates just above 40 percent and remained there for the first half 2009.

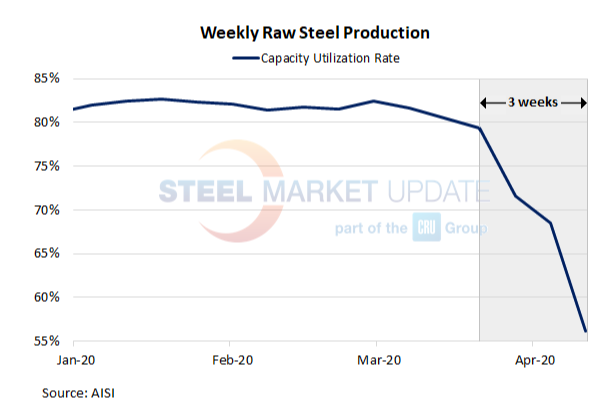

I don’t see that happening here. In the graphic below, you can see we are still early in the process having only seen declines in the capacity utilization rates over the past three weeks.

Why?

Service center inventories were in control prior to COVID-19 becoming an issue. Companies are already addressing potential inventory issues, and the steel mills are taking capacity offline rather than attempting to push tonnage into the spot markets.

The general U.S. economy, prior to COVID-19 and the rift between Russia and Saudi Arabia over oil production (which resulted in a crash of oil prices), has been quite steady in virtually all market segments. We were seeing a solid construction market, auto market and agricultural market, which comprise approximately 80 percent of the market prior to energy.

You will hear from Phil Raimondo of Behlen Manufacturing in tomorrow’s SMU Community Chat webinar (11 AM ET), who will discuss the various market segments they service (grain bins, livestock equipment, metal buildings, and miscellaneous sub-contracted fabricated parts). You might be surprised. You can register for the free webinar by clicking here. You are welcome to invite non-SMU members to our webinar. The idea is for it to truly be a community chat.

Scrap collection and pricing is much different today than what we saw in 2008. In 2008 people needed to collect scrap to make money, buildings were still being razed, collection was not an issue. This has changed. You can get $1,200 from the government to sit at home; why go collect scrap to make $150? Scrap prices are firming here since there are so few tons available.

Tighter scrap prices mean EAF mills can’t be quite as aggressive on the low side. We are hearing that the domestic mills are trying to “firm up” at $460 per ton ($23.00/cwt) and not move into the low $400s. The idea is with tighter scrap prices the spread is not there for low $400 hot rolled. We will see over the next few weeks if the mills are able to hold the line and not lose focus on pricing.

The following quote is from the head of commercial for a steel mill. The quote is from this afternoon: “Things are steadier on price this week vs. last. Demand is still tepid. But some buyers are coming off the sidelines looking to position themselves once industry is more open in May and June. I think they sense that production cuts have been aggressive, and furnaces will not restart until things are sustainably better.”

I spoke with the owner of a Midwest service center who also told me that he was no longer as bearish as he had been over the past couple of weeks. The scrap market firming up has gotten his attention. Much like the mill above, he spoke of perhaps looking to take a position in hot rolled if there truly were prices below the $460 per ton level.

The president is already talking about restarting the economy. The governors of each state will make the final determinations, but they are working together to make well-advised decisions. The governors in the Northeast and those on the West Coast are banding together to plan the re-opening of what were considered “non-essential” businesses.

Remember, most steel and manufacturing companies have been considered “essential” businesses and many continue to run.

We are still early in the process. The question now is how much short-term demand is going to go away? By that I mean, when ABC company eventually reopens, will they take the steel they were going to use during the shutdown or will that business be lost for good? Or will that inventory need to be worked through?

Then we need to look at longer-term demand to the economy. Will automobiles be selling at the rates they were prior to the COVID-19 lockdowns? Will people feel comfortable spending money in the same way as they did in January?

I am not an economist. I am going to go with Bill Gates on this one. In recent comments on CNBC, Gates said he believes colleges/schools will be back in operation in September if the U.S. government can get their act together so there can be meaningful testing on a large scale by this fall. (By large scale, this would include not only those who might be infected, but also those who had the virus and are free to move about.) With large scale testing, companies also would be secure in opening, having people travel, etc. Gates feels with testing there can be a “V” shaped recovery.

Speaking of travel and opening. I want to give you an update on the 2020 SMU Steel Summit Conference. We have not yet cancelled/postponed the conference. We are under quite a bit of pressure from the hotels and GICC to make a final decision, but we do not want to make a decision that might place any of our attendees at risk. Our preference is to wait until June 1, 2020, in order to better understand whether a conference of our size is reasonable or not. We are constantly interacting with our speakers, sponsors, exhibitors and past attendees to gather as much information as possible so we can make the best decision for everyone.

I can tell you just about every company with whom I interact wants us to host a conference, provided the conditions are “safe” to do so.

We are considering taking the conference to a virtual (online) medium at a much lower cost. We know the biggest part of an SMU conference is the networking, and we are looking for something that can replicate that online. If you have any suggestions, we are all ears: John@SteelMarketUpdate.com

Please stay tuned.

When it comes to our Steel 101 workshops, my opinion at this time is that the first one could be this summer or in September. We have one scheduled at ArcelorMittal Dofasco in September. We have had to postpone two others – one set for NMLK in Portage, Ind., and another that was going to be at SDI Butler. The dates for those two will be discussed with each mill and new dates selected once we get past the worst of COVID-19. Since the workshops are in smaller groups, we can control social distancing, provide masks and hand sanitizers, etc. as needed. No decision has been made, so please stay tuned.

The head of purchasing for a large service center group told me this morning how important it is right now to have a steady flow of quality information. There is a need for information about the industry, about what is happening in the rest of the world and about the economy. Steel Market Update and our parent company, The CRU Group, are well positioned to provide quality information and data.

If you would like information about renewing your membership, upgrading or adding new people to your membership or finding out how to become a new subscriber, please contact Paige Mayhair at 724-720-1012 or by email: Paige@SteelMarketUpdate.com

Here at SMU we will continue to host our weekly SMU Community Chat webinar, which is free to anyone who wants to register and watch us speak about a wide variety of subjects. I have already booked some interesting contributors including Timna Tanners, Metals and Mining Analyst for Bank of America Merrill Lynch; Ken Simonson, Chief Economist for the Associated General Contractors of America; Bernard Swiecki, Director of the Automotive Communities Partnership for the Center for Automotive Research, and more. You can register for tomorrow’s webinar featuring Phil Raimondo, President & CEO of Behlen Manufacturing, by clicking on this link.

As always, your business is truly appreciated by all of us at Steel Market Update.

John Packard, President & CEO