Product

April 19, 2020

SMU Steel Buyers Sentiment Index: Future Appears Brighter

Written by Tim Triplett

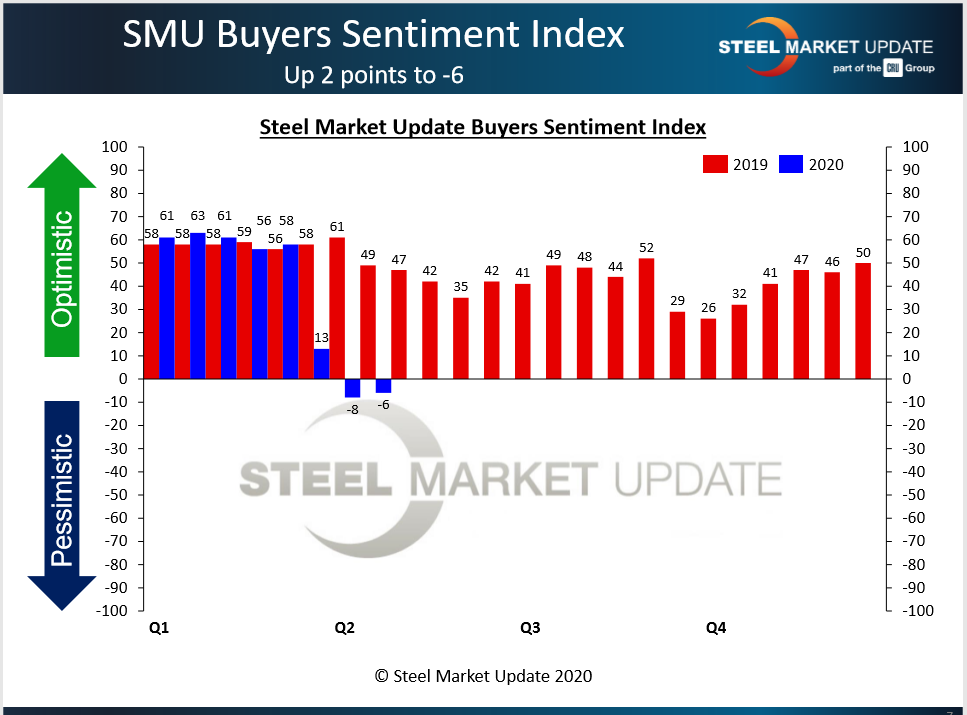

Steel Buyers Sentiment remained in pessimistic territory in mid-April as steel demand was stifled by the government restrictions on commerce to control the spread of COVID-19. Future Buyers Sentiment was notably more optimistic, however, which suggests service center and manufacturing executives anticipate better days ahead.

Steel Market Update asked steel buyers how they view their company’s current prospects for success, as well as their chances for success three to six months in the future. This week’s Current Sentiment reading was -6, a slight improvement from -8 in early April. To put that figure in perspective, Current Sentiment has not been in negative territory since November 2010. The index spent two years in the pessimistic half of the range from late-2008 to late-2010 as the economy slowly recovered from the Great Recession. During the month of April 2020, Sentiment saw the sharpest one-month decline in the 11-year history of SMU’s index, dropping 66 points from a reading of +58 in the beginning of March.

Future Sentiment

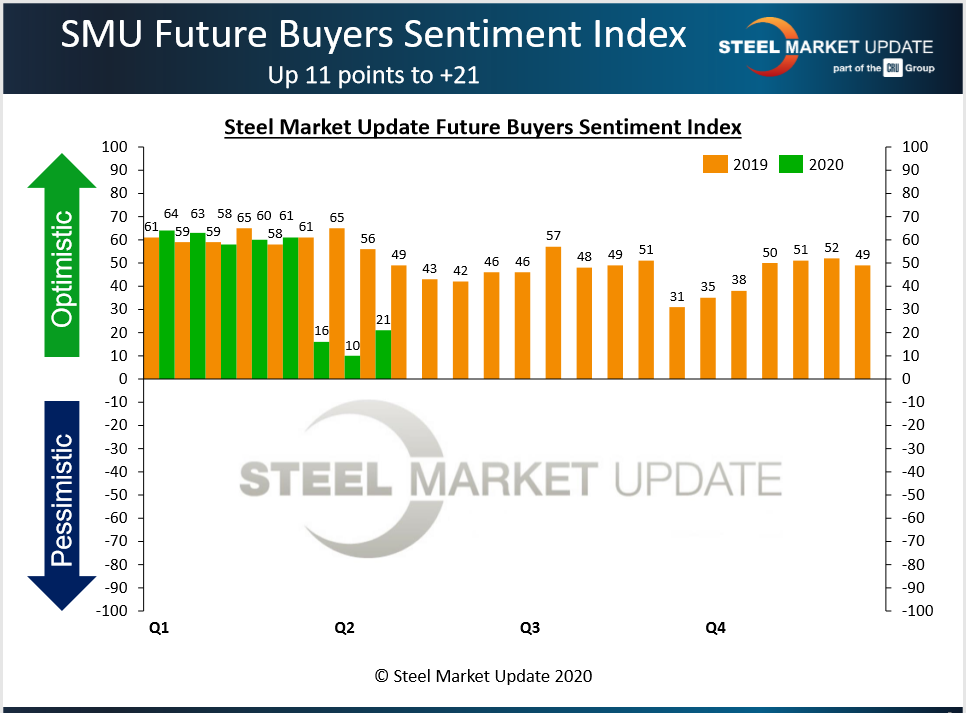

SMU’s Future Sentiment Index registered +21 in the latest canvass of the market, up 11 points over the last two weeks. Still far below the more typical +56 reading at this time last year, the uptrend is positive and suggests some steel execs are hopeful the virus will run its course in the next few months.Looking back on the Great Recession, we saw our Future Sentiment Index bounce from negative (pessimistic) into positive (optimistic) territory during the months of May through November 2009. It was not until December 2009 that Future Sentiment stayed firmly planted in the optimistic portion of our index, and has remained that way, including now. Future Sentiment has not dropped into the pessimistic area (unlike Current Sentiment, which is now at -6).

SMU also asked readers this week how quickly they could rebuild their businesses back to pre-virus levels if the government “opened” commerce back up by May 1. The majority said they could rebound by the end of July.

Results from SMU’s market trends questionnaire are posted as both single data points and as three-month moving averages (3MMAs) to smooth out the trend. Both Current and Future Sentiment measured as 3MMAs saw big declines in the past two weeks The Current Sentiment 3MMA declined to +29.00, down from +40.50 in early April. The Future Sentiment 3MMA dipped to +37.67 from +44.67.

ARTICLE CONTINUES BELOW

{loadposition reserved_message}

What Respondents Had to Say

Comments from service center and manufacturing executives responding to SMU’s April 13 survey reflect the weight of their worry over the coronavirus crisis:

- “NYC area customers are more likely to be closed than open.”

- “Business is steady, but there is a lot of uncertainty on the national economic level.”

- “Declining a little more each week.”

- “COVID-19 restrictions are different in each state in regard to construction.”

- “Demand appears to be a moving target as OEMs struggle with keeping plants running and understanding what their order intake will be.”

- “When the majority of your customer base is closed due to government mandates, you cannot be successful.”

- “We will hold our own, but we are experiencing some stiff headwinds.”

- “State government has us shut down due to COVID-19.”

- “April shipments are expected to be about 45 percent below what was forecast at the start of the year.”

- “Prices are dropping. Inventory values are dropping. It will be difficult to recover with limited demand for our products.”

- “The outlook looks very negative as most economists are calling for recession and reduced demand. It depends on how long this lockdown lasts and how quickly we can recover. But this year does not look very promising.”

- “Once the economy opens back up, and consumer confidence returns, there should be some pent-up demand for our products.”

- “When the virus-related situation returns to some facsimile of normal, there will be a lot of pent-up demand and business levels will ramp up quickly. But I don’t think that will happen in the next three months, and may only be beginning six months from now.”

- “We’re doing fair compared to competitors. No matter what, we all have a rough row to hoe.”

- “A lot of jobs have been shelved for at least 3-6 months, so I do not see demand coming back until August or September.”

- “Once the government finally opens the economy back up, it will take several months to recover.”

- “Maybe this is false hope, but I think the U.S. government, among other major economies, has provided enough liquidity/incentives to kickstart demand within the next 4-6 months.”

- “April and May will be extremely difficult. After that it’s really hard to estimate, but we think the recovery will be gradual and uneven.”

About the SMU Steel Buyers Sentiment Index

SMU Steel Buyers Sentiment Index is a measurement of the current attitude of buyers and sellers of flat rolled steel products in North America regarding how they feel about their company’s opportunity for success in today’s market. It is a proprietary product developed by Steel Market Update for the North American steel industry.

Positive readings will run from +10 to +100 and the arrow will point to the righthand side of the meter located on the Home Page of our website indicating a positive or optimistic sentiment. Negative readings will run from -10 to -100 and the arrow will point to the lefthand side of the meter on our website indicating negative or pessimistic sentiment. A reading of “0” (+/- 10) indicates a neutral sentiment (or slightly optimistic or pessimistic), which is most likely an indicator of a shift occurring in the marketplace.

Readings are developed through Steel Market Update market surveys that are conducted twice per month. We display the index reading on a meter on the Home Page of our website for all to see. Currently, we send invitations to participate in our survey to more than 600 North American companies. Our normal response rate is 100-150 companies; approximately 40 percent are manufacturers, 45 percent are service centers/distributors, and 15 percent are steel mills, trading companies or toll processors involved in the steel business. Click here to view an interactive graphic of the SMU Steel Buyers Sentiment Index or the SMU Future Steel Buyers Sentiment Index.