Market Data

April 23, 2020

SMU Market Trends: How Long Will Business Take to Recover?

Written by Tim Triplett

Companies are being affected to varying degrees by the coronavirus depending on their market and geography, so it’s no surprise their opinions range widely on how long it will take business to return to pre-COVID levels. Some hope for activity to rebound as soon as this summer, while others fear it won’t be until next year or even 2022. Fourth-quarter 2020 seems to be the dividing line, with half predicting recovery before then and half after.

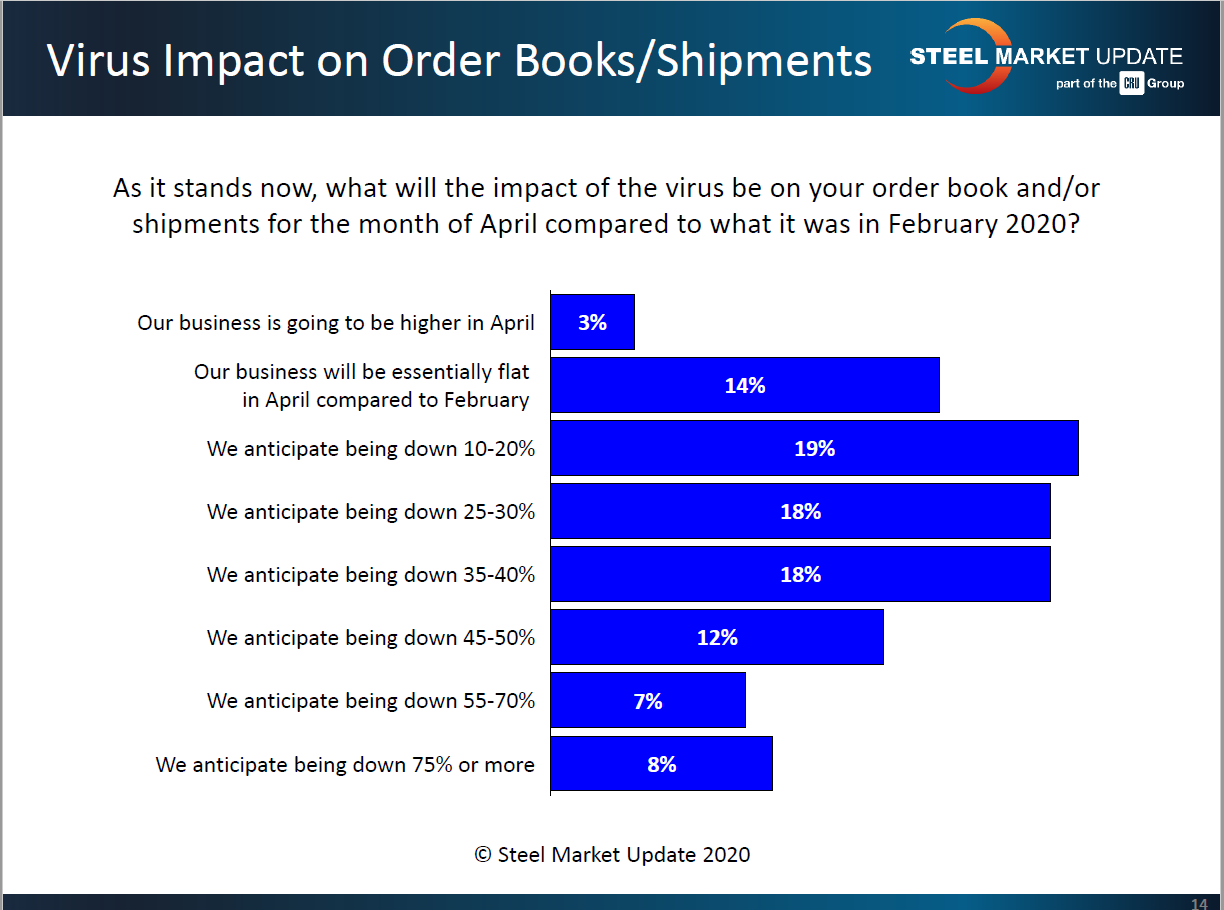

Steel buyers—service center and OEMs—estimated their business will be down anywhere from 10 to 70 percent in May, with an average drop-off of nearly 40 percent. Industry executives shared the following thoughts (anonymously) during Steel Market Update’s canvass of the market this week:

Those Who See Recovery by Q4

“We will probably be down by a minimum of 60 percent in May. Our plants are open, but many of our end-users are closed. August 2020 for business to recover.”

“I think May and June will be similar down 30-40 percent, with July off 25 percent, August and September off 15 percent and October looking almost normal. That may be optimistic, but I have faith in the resiliency of the USA and our people. There is a chance that 4Q 2020 will be OK, but ‘normal’ demand is 1Q 2021 at the earliest.”

“Our demand has been impacted by 60-70 percent. The shutdown of auto and energy manufacturing facilities, along with retail stores that sell steel-intensive products being labeled “non-essential,” continues to weigh on our overall customer demand. We look for things to improve as we get into the middle of May.”

“More than 50 percent of our customer plants are closed. We believe it will be October before business volumes return to pre-February levels. However, we believe steel prices will start to move upward once all of the major auto manufacturers are operating, even if at a lower capacity than just three months ago.”

“We’ll be down 30 percent in May. A number of customer plants are closed, some as much as four weeks. We expect improvement in July and August, but likely will not see pre-February levels until 4Q.”

“Our volume is off about 30 percent. About 15 percent of our key customer base had been closed, but each week more are opening.”

“Our May outlook is better than April. A few customers are closed due to lack of work, but none of our facilities are closed. Fourth-quarter to return to previous business levels.”

“Our business will be at 70 percent in May. Many automotive-related customers are closed. Our plants are running at reduced capacity. September for return to pre-virus levels.”

“Demand is off about 10 percent from what we would expect in the first few months of the year. I feel there will be an opportunity in the next one to one and a half months to take advantage of low prices before this price cycle reverses and starts to head up. It will take some guts to pull the trigger in light of all that is occurring on both the supply and demand fronts.”

“Yes, demand is lower due to COVID-19 and we are forecasting May 2020 to be 25 percent below May 2019. None of our customer plants are closed, but some construction jobsites have been closed. Fourth-quarter 2020 at best for recovery. Depends on the pace and rules associated with getting back to ‘normal.’”

Those Who See Recovery After Q4

“I am hopeful May improves from April, but we still could be looking at a 20 percent reduction from 2019. We estimate 25-30 percent of our customers are closed. It’s going to take a while before business returns to pre-February 2020 levels. Maybe not until Q1 or Q2 2021. Hope I am wrong.”

“May will be much worse than May 2019. We have customers closed, but we are open and fully operational. The return to pre-February 2020 levels depends on how much longer this insanity continues. Every day we keep the economy shut down is going to make it that much worse. Right now, it will be first quarter next year at best.”

“We expect May to be down 30-40 percent year over year. We have seen more customer closures in the South than in the Midwest. Things change daily, so it’s hard to put a value on it. Fourth quarter at the earliest for recovery, most likely 2021.”

“We expect May business levels to be down 40-50 percent from May last year. We are canceling or reducing orders. Several of our OEM customers are taking shutdowns. Recovery not until 2021.”

“May will be down 20 percent. We’re pushing out orders. We did close one paint line, but the virus only expedited the decision. Personally, and without any data to support it, I don’t think we will have a full return until next spring. But I do believe we will see growing demand throughout the third and fourth quarters.”

“May will be down 15 percent. We are ordering only for customer PO’s. A few of our customers are closed, but luckily most large ones are still open. We are operational. The longer this drags on, the more damage will be done and, in my view, the longer the recovery.”

“Down 50 percent in May. Some customer plants are closed, but starting to come back online this week and next. Return to pre-February levels not until Q2 2021.”

“We’ve had every major OEM we serve close, save one ag company. A couple are returning this week following two-week shutdowns, and we expect (hope) that the others will return in the next week or two, as is their plan. So, we’re now moving into a transition period and the issue will be whether the re-opened companies can remain open. Assuming most or all are back up and running, our early guess is that May will probably be about 70 percent of what we saw last year. Earliest back to pre-Feb levels is 2H21, but more likely into 2022. Unless and until a vaccine is available and in wide use, it would appear to be impossible to reclaim those levels.”

“We’re looking at forecasts from customers ranging from down 15-55 percent depending on the individual account, the industry they’re in, and geography. We’ve had various customers closed for lengths of a couple days up to three weeks or more. Recovery not until 2021. We think volumes will come back gradually and inconsistently throughout most of 2020.”