Product

June 4, 2020

HRC Futures Quiet While Busheling Breaks Lower and Iron Ore Attempts to Rally

Written by David Feldstein

SMU Contributor David Feldstein is president of Rock Trading Advisors (davidfeldstein@rocktradingadvisors.com, twitter @TheFeldstein). In addition to market analysis, RTA provides price risk management not only for ferrous products, but also base metals, energy and interest rates. RTA also trains sales staff and creates the infrastructure necessary for firms to offer their customers fixed pricing on physical sales.

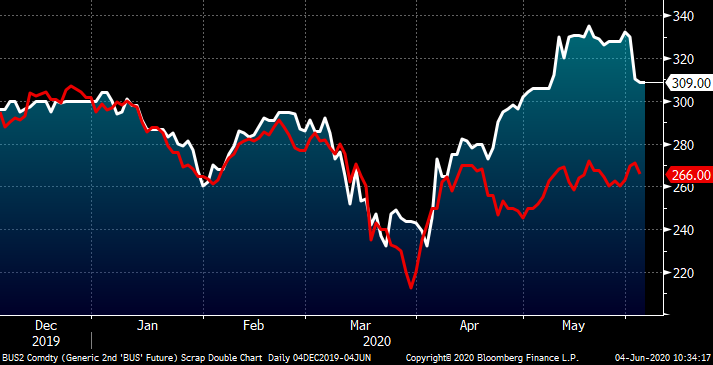

Due to a shortage of scrap creation resulting primarily from the shutdown of the automotive industry in April, Midwest busheling experienced a supply shortage, which drove its price higher while most other commodity markets were in freefall. June and July busheling had been trading in the $330-$340 range since mid-May until Tuesday when aggressive selling pushed the curve $15-$20 lower. With a week to go until the June scrap settlements, the expectations of a $10-$20 increase for Midwest busheling looks to have adjusted lower, pointing to a flat to $10 MoM increase.

LME Turkish scrap remains range bound trading between $260 and $270. The spread between busheling and Turkish scrap has narrowed to around $45 from as high as $80.

Rolling 2nd Month CME Busheling Future (white) & LME Turkish Scrap Future (red)

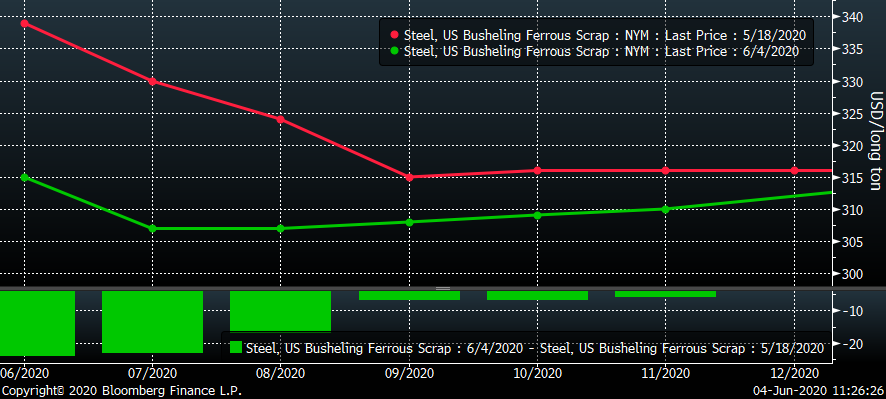

This week’s selling has flattened the CME busheling curve.

CME Busheling Futures Curve

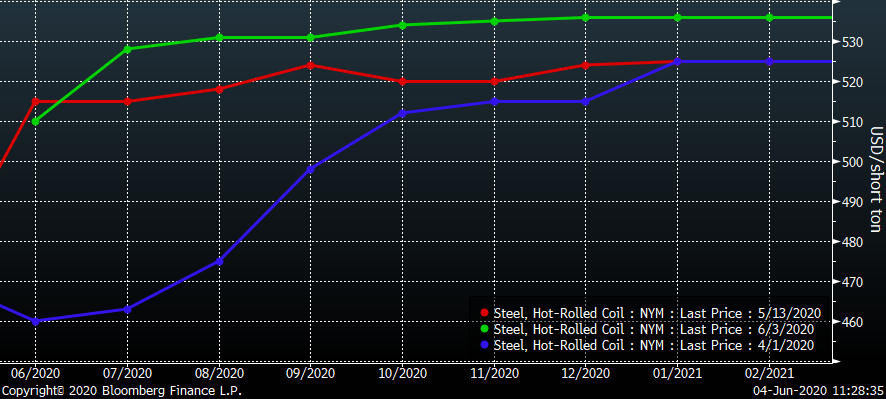

The rally in Midwest HRC has stalled out with the rolling 2nd Month CME Midwest HRC futures, now July, remaining range bound between $520 and $540 since early May. The futures priced in full acceptance of not only the first price increase from $460 to $500, but also anticipated a second $40 price increase being fully accepted that would bring the HR indices to $540. Currently, HRC base indices remain in the $500 to $510 range.

In the commercial marketplace, it is a story of the haves and the have-nots. The service center “haves” purchased large tonnages down at recent lows ($440ish) and the have-nots, buying off index and spot, have been struggling to compete. With less than desirable utilization rates, the EAFs continue to seek orders pricing tons at a discount (to BOF pricing) despite inflated scrap prices, while the BOFs have extended their lead times due to idled capacity effectively squeezing them out of the spot market. The entire space is on edge anticipating the return of additional capacity while the manufacturing industry continues to recover from the virus induced shutdown/slowdown.

Rolling 2nd Month CME Hot Rolled Coil Future $/st

Except for June trading between $510 and $520, the CME Midwest HRC futures curve has remained flat and in a tight range between $530 and $540 for the past couple of weeks. The front of the curve rallied sharply ($35-$60) since the lows seen in April. Busheling scarcity and the resulting higher price action, as well as significant integrated capacity reductions, have been the main catalysts behind the rally. With scrap poised to fall and the inevitable return of idled capacity, what will drive flat rolled prices higher? I am curious to see the market’s reaction to the first headline of a restarted BOF. In the same way many expected the busheling rally would peter out once automotive OEMs restarted creating scrap (something that has abruptly happened just this week), will we look back at today wondering what were all those $535 futures buyers thinking knowing additional idled supply is due to come back online? Or will the return of integrated furnaces be considered bullish, that is an indication of a pick-up in mills’ order books?

CME Midwest HRC Futures Curve

Iron ore has been on a wild ride as it has broken above the top of its multi-year range. While the Australian miners have been producing at full tilt, concerns that the COVID outbreak in Brazil will slow or stop Vale’s iron ore mining operations have created concerns of tighter supply.

Rolling 2nd Month SGX Iron Ore Future $/mt

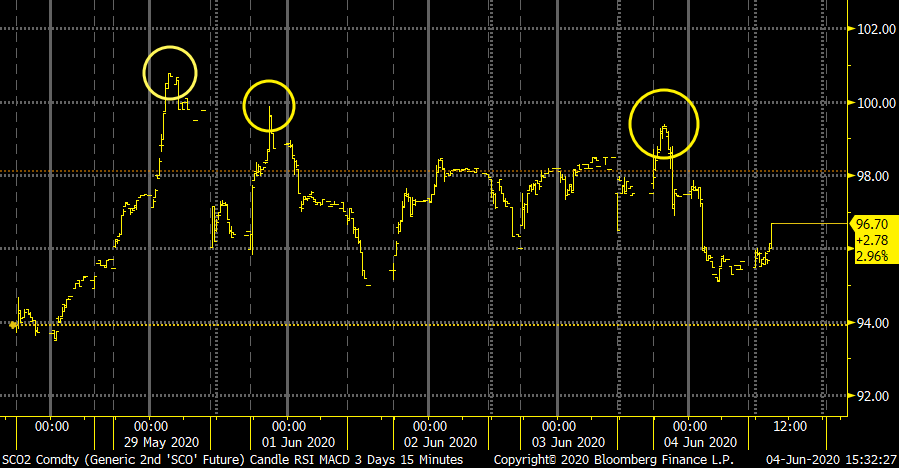

However, iron ore has failed to sustain a rally, failing at sequentially lower highs only to trade back down to $96 three times over the last five trading sessions.

Rolling 2nd Month SGX Iron Ore Future $/mt – Intraday

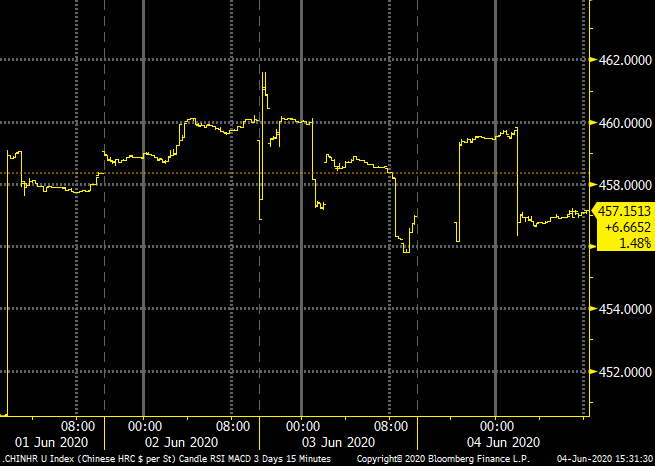

Similar resistance was seen in the July SHFE Chinese HRC future at $460/st, but also take note that Chinese HRC has gained $20 since the end of last week following the National People’s Congress annual meeting.

Rolling 2nd Month SHFE Chinese HRC Future $/st

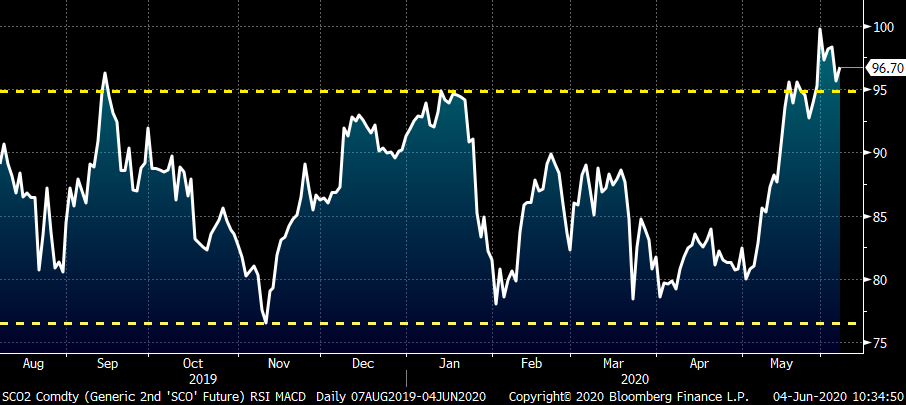

After remaining range bound since April, the U.S. Dollar Index has sold off sharply in recent days to its lowest level, around 96.75, since early March. A weaker dollar typically boosts commodity prices.

U.S. Dollar Index

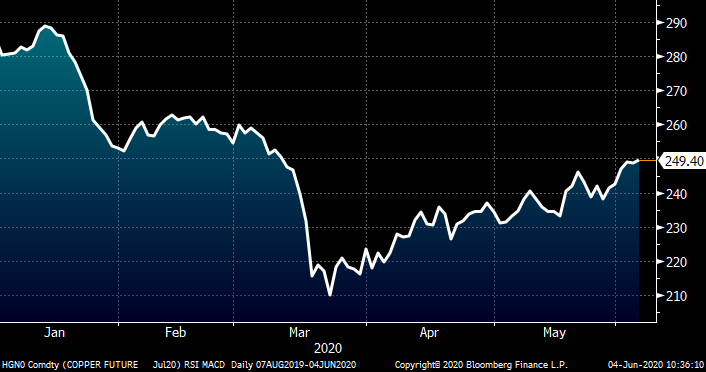

Case in point, copper has continued to rally, especially in recent days as the dollar has weakened. A number of factors are at work behind copper’s rally, which has now retraced 50 percent of what was lost in the sell-off since its peak in early January. The bottom line, Dr. copper can be a reliable indicator of the global economy with this rally perhaps indicating continued recovery ahead.

July CME Copper Cents/lb

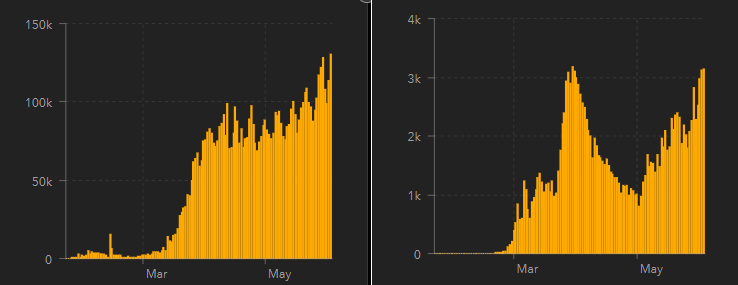

Of course, significant uncertainty pertaining to the COVID-19 outbreak’s effect on the global economy remains. The graph on the left shows new daily cases globally breaking out to what may be the beginning of a third wave of exponential growth. The graph on the right shows new daily cases in Iran as an example of what a failed effort to control an outbreak looks like as Iran looks to be experiencing a second wave of exponential growth.

New Daily COVID-19 Cases Globally & Iran

It was concerning to see many ignoring the measures to prevent the spread of COVID-19 over Memorial Day weekend and if that behavior would hamper efforts to slow the spread of the virus. Then came the historic events of the past week where protests across not only the United States, but also in Europe, Africa and Australia, among others, resulted in all-day mass gatherings day after day that still continue to occur. The tragic death of George Floyd and the events that followed is a very sensitive topic and this article is not an appropriate forum for it to be discussed. However, from an economic point of view tied to COVID, these events may result in significant economic outcomes. These gatherings broke many of the fundamental rules society has been following since March, such as no mass gatherings, wearing masks, maintaining social distance, etc. If we see a powerful resurgence in new cases as those involved in these events, whether it be the protestors, looters, police, reporters, etc., return to their homes and workplaces in their respective hometowns, then we can expect further economic pain in the months ahead.

This is very scary stuff. Hope for the best, but plan for the worst. Don’t underestimate the downside price risk that remains embedded in the steel industry and U.S. economy.

Disclaimer: The content of this article is for informational purposes only. The views in this article do not represent financial services or advice. Any opinion expressed by Mr. Feldstein should not be treated as a specific inducement to make a particular investment or follow a particular strategy, but only as an expression of his opinion. Views and forecasts expressed are as of date indicated, are subject to change without notice, may not come to be and do not represent a recommendation or offer of any particular security, strategy or investment. Strategies mentioned may not be suitable for you. You must make an independent decision regarding investments or strategies mentioned in this article. It is recommended you consider your own particular circumstances and seek the advice from a financial professional before taking action in financial markets.