Overseas

June 25, 2020

CRU: China On its Own for Higher Prices

Written by George Pearson

By CRU Prices Analyst George Pearson, from CRU’s Steel Monitor

Steel sheet prices in the U.S. Midwest market were mixed this week with slight declines for both HR and HDG coil, while CR coil was slightly higher. Market contacts have noted that markets are weakening as demand has not come about as previously expected. Lead times for HR coil at mills, on average, have remained short while inventories throughout the supply chain were said to be higher than expected.

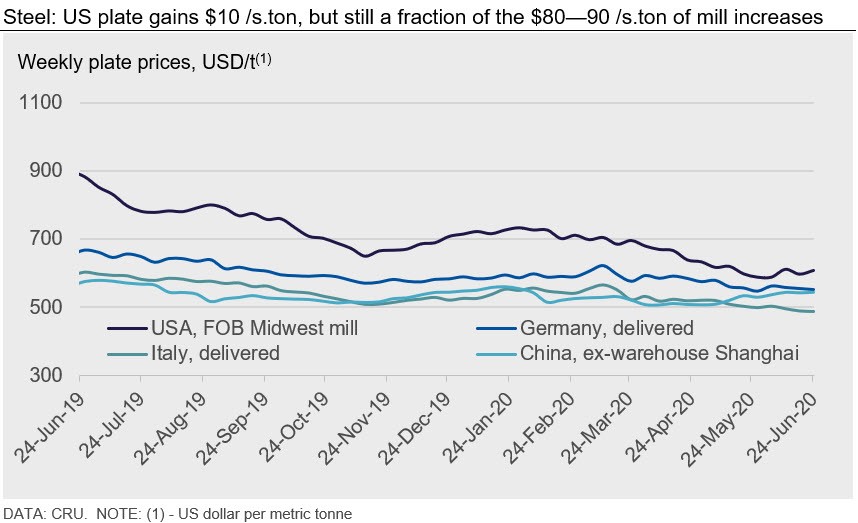

For HR coil, the number of weekly data points has increased again, and continues to remain at a high level, though average volume per data provider fell back from last week. Plate prices in this market rose by $10 /s.ton. While prices were higher, they are now just $18 /s.ton higher than their recent bottom and reflect only a portion of the two recent mill price hikes, which totaled $80-$90 /s.ton. Plate prices are likely to rise in the near term, yet resistance will come as scrap prices fall back in July while sheet prices have reversed course and are falling back as well.

Five of the six sheet prices for Europe fell, with only German HR coil remaining unchanged w/w. After several weeks of speculation, there are now reports that ArcelorMittal has announced a price increase in Northwest Europe, but no blanket increase in Italy. European mill increase announcements last year did not automatically result in higher prices, but we maintain that there are enough factors for prices to rise. All sheet prices are now well below the bottom of last November and mill margins are around the low of that time. Raw material prices are high, and import offers are less competitive than previous months. We have heard of regular European buyers from Turkey that are looking to source material domestically. Despite the efforts of domestic sellers to hold prices two weeks ago, destocking has continued to exert price pressure in Europe. The coming weeks are likely to give a better idea of demand appetite from buyers and the ability of service centers to pass on higher costs to end-users.

Chinese steel prices were mixed this week, with HR coil up by RMB60-70 /t and rebar unchanged. Steel destocking has slowed over the last week due to low construction activity caused by the bad weather in southern China. Total steel inventory remained largely flat w/w. However, prices were stable due to the positive demand outlook of market participants. The Ministry of Finance reported that it had released RMB2.29 trillion worth of special bonds before June 15, around 60 percent of the annual quota. These were focused mainly on transportation, municipal projects and residential quality of life improvements, which boosted market sentiment. Sheets demand continued its strong momentum in end-use sectors. The latest published statistics indicate that the fundamentals of sheet-consuming sectors, such as auto and home appliances, have remained robust with continuous recovery in sales and production.

Steel production remains at a record high level. Given low physical transactions ahead of the Dragon Boat Festival and a weaker demand outlook in the summer, we expect to see growth in inventories in the coming week. Together with high BF utilization rates driven by high steelmaking margins, we believe steel prices are be likely to fall in the next few weeks.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com