Market Data

August 21, 2020

CRU: U.S. Dollar Shifts into the Spotlight as Economic Forecasts Stabilize

Written by Jumana Saleheen

By CRU Chief Economist Jumana Saleheen from CRU’s Global Economic Outlook

Our global economic forecast has stabilized as our understanding of the economic impact brought on by the virus has improved. In August, there have been some offsetting changes across regions with the USA and China data a little stronger than expected and the EU a little weaker. This has allowed us to focus our overview on the impact the virus is having on currencies. The U.S. dollar initially strengthened when the virus struck, however it has recently lost most of these gains. This has led many to believe it is the start of a broader dollar unravelling. We do not think so. Instead we believe that the dollar will gain value marginally once the USA manages to bring the virus under control and Congress seals the deal on a second Covid-19 stimulus package.

The Greenback is Not Unravelling

In this month’s overview we focus on the U.S. dollar, which has lost 2 percent of its value on a trade weighted basis since June. Is this the start of a broader dollar unravelling? We do not think so. Instead we believe the dollar will gain value marginally once the USA manages to bring the virus under control and Congress seals the deal on a second Covid-19 stimulus package.

Dollar Worries Grow as it Falls Sharply in July

There is broad agreement that the dollar is overvalued, by ~10 percent, propped up by its status as a safe-haven currency that investors turn to in uncertain times. This factor is what led the dollar to peak in late March. Since then it has dropped back, with the U.S. Dollar Index falling by 4 percent in July, when the value of other safe-haven investments, such as gold and silver, has risen. This has led many to ask if this is the start of the dollar unravelling.

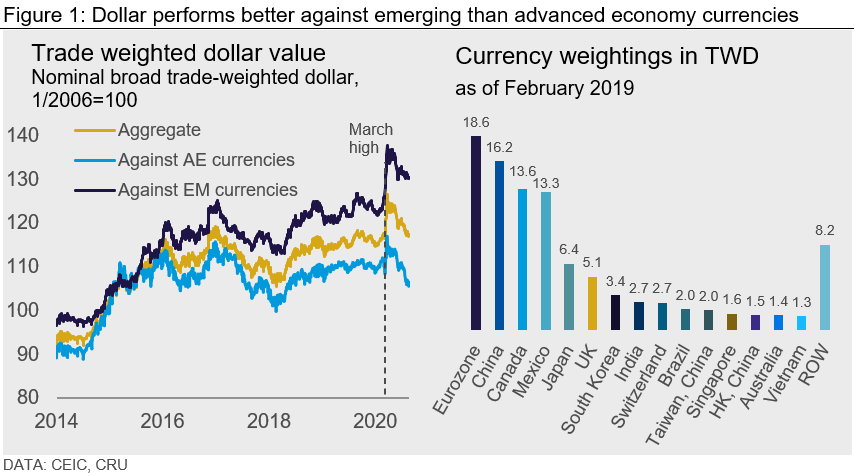

The dollar has certainly lost value, but mainly against advanced economy (AE) currencies; it has been stable against emerging markets (EM) currencies since June (Figure 1). The currency trade weightings remind us that the territories whose currencies matter most for the trade weighted dollar (TW$) include the Eurozone, China, Canada, Mexico and Japan.

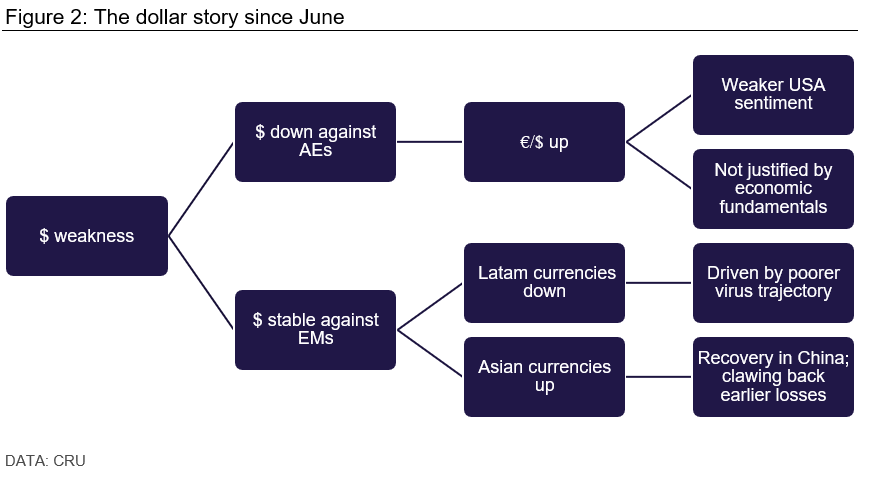

In the June Exchange Rate Outlook, our view was that the TW$ would remain broadly stable through the rest of 2020 supported by pandemic uncertainty. Instead the trade weighted dollar fell by 2 percent. Figure 2 shows how this has happened.

A Raging Virus and Delayed Second Stimulus Hurt the Dollar

Our view is that the recent euro rally will not continue, as economic fundamentals have not changed; interest rates will remain unchanged and growth prospects continue to be better for the USA than for the Eurozone. As a result, the weaker dollar must be driven by sentiment: negative towards the USA and positive towards the Eurozone.

In the USA, the weak sentiment stems from two factors—the high number of virus cases and the inability of Congress to agree a second stimulus package before the summer recess. Many U.S. states have paused plans to reopen amid rising case counts. Several are re-imposing restrictions such as the closure of bars and restaurant dining. In contrast, the positive sentiment towards the Eurozone comes from a lower (albeit rising) level of new virus cases, and the EU stimulus agreed and announced in July. The latter did not alter the macroeconomic outlook, but it did nevertheless boost the euro as it provided a better than expected policy response. Given the previous weakness of the euro, this was enough to tip sentiment in favor of the euro and push it closer to its fair value.

Fed Chairman Jerome Powell noted at the FOMC press conference that a worse course of the virus means a weaker economic recovery. Faced with an unemployment rate of 10 percent, Republicans and Democrats agree that further fiscal support is needed. However, they disagree on the total stimulus required, and the form of that stimulus. President Trump issued Executive Orders on Aug. 8 mandating a federal extended unemployment insurance of $400 p/w (down from $600 under the CARES Act). The U.S. section details our base case view that Congress will agree to a large stimulus package in September. That, together with an improved virus trajectory, is expected to boost the dollar against the euro and other AE currencies this fall.

On Aug. 27, as part of the Jackson Hole Economic Symposium, the Fed announced that it would be altering its monetary framework. It will move from an inflation target of 2 percent, to a flexible inflation target of 2 percent. That means if inflation undershoots 2 percent in one year, it can legitimately overshoot the following year, so that on average inflation hits 2 percent. That change may alter investors’ assessment of future interest rate differentials and the trajectory of the dollar. CRU will continue to monitor implications of this change and keep clients informed.

Currency Winners (Asia) and Losers (Latam)

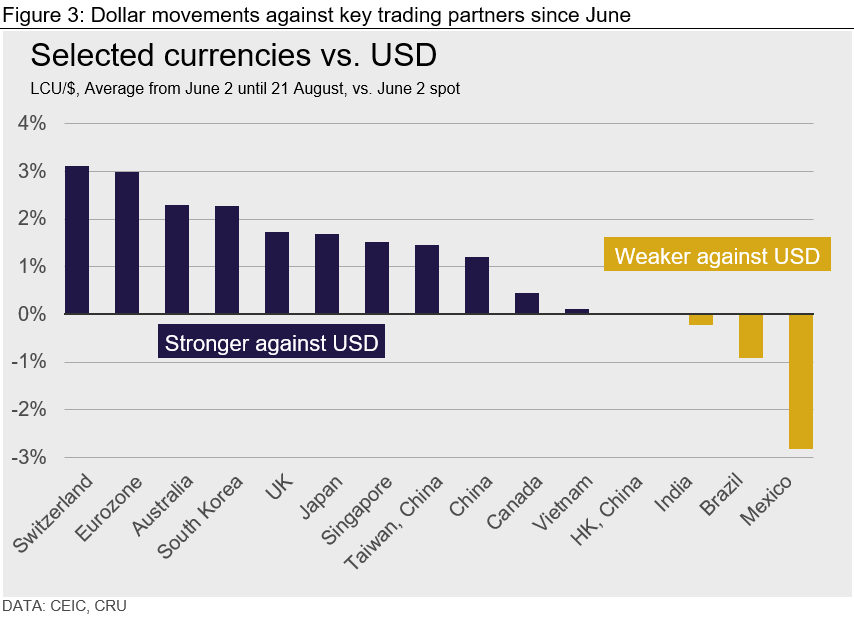

Despite the stability of the dollar against a basket of EM currencies, within that basket there have been winners and losers. Since June, the Chinese RMB has gained about 1 percent against the dollar. This reflects the robust recovery underway in China in Q2 (the outbreak was in Q1). China’s authorities are also seen to be successful in stamping out local outbreaks. On average, the Indian rupee has been stable since June, but that broad stability hides a more nuanced volatility. It depreciated by 1.5 percent in the first two weeks but recovered 1 percent since mid-June. We interpret this recent strength as a clawing back of the 7 percent fall of the rupee against the dollar in the first half of 2020. In contrast, the Brazilian real and the Mexican peso have fallen by 2-3 percent against the dollar as the two countries continue to battle the virus, and as the virus takes a toll on economic activity.

By Year-End Expect the Dollar to Strengthen Slightly

We judge that the current strength of the euro against the dollar will not continue further. Once Congress agrees to a second stimulus package and the virus is brought under control in the USA, we think the dollar is set to strengthen (albeit modestly) against the euro. The dollar is likely to remain stable against the EM currency basket for as long as virus fears justify the global “risk off” sentiment. Once the virus is behind us, sometime in 2021, we expect the dollar to start to lose its appeal as a safe-haven and at that point it should fall back against all its trading partners as it returns to fair value. The dollar is not losing its dominance anytime soon.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com