Analysis

September 9, 2020

Final Thoughts

Written by Tim Triplett

Our futures contributor, Tim Stevenson of Metal Edge Partners, raises a good question in his column this week. With the mills moving steel prices higher, have buyers restocked enough to stay out of the market? “If so, service centers and end users can step away from spot buys and wait for prices to fall again. If, on the other hand, inventory levels are still too low, people may have no choice but to keep buying higher priced steel, providing more longevity to this upward price cycle.”

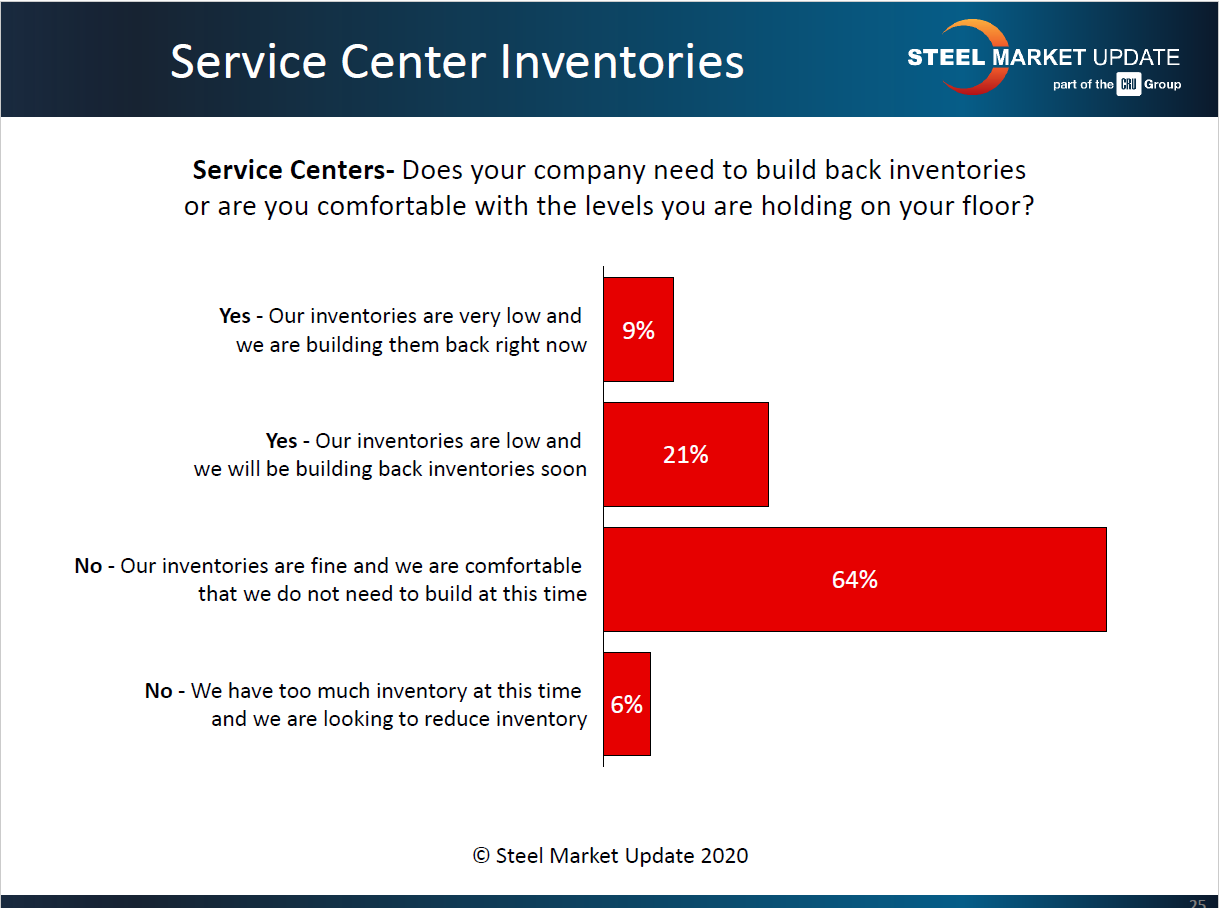

Steel Market Update’s latest market survey shows that 70 percent of service centers are comfortable with their inventory levels or are looking to reduce inventories. Only 30 percent say they are in a buying mode (see chart). We’ll be looking closely to see if those percentages change in next week’s survey. If not—if the escalating prices aren’t bringing more buyers in off the sidelines—that will say something about how long and how high prices may rise.

Welcome to David Schollaert, newly hired Deputy Editor at Steel Market Update. David brings a wide range of expertise to SMU’s reporting and analysis. He is the former Editor of Ryan’s Notes, a newsletter covering the global ferroalloys market, and he transitioned to Senior Editor of the CRU Prices Service following CRU’s acquisition of Ryan’s Notes in 2012. During his career, he has been a metals buyer as well as a journalist writing for metals buyers, so he understands both sides of how steel is bought and sold. He will contribute a new perspective and a new voice to SMU’s content, and we’re excited to add David to our team.

Don’t forget, those registered for the SMU Virtual Steel Summit have until the end of next week to use the conference platform and view the recorded presentations and exhibitors’ offerings one more time. But the platform will only remain live through Sept. 18.

As always, your business is truly appreciated by all of us here at Steel Market Update.

Tim Triplett, Executive Editor