Premium

September 11, 2020

SIMA: Steel Import License Data for August

Written by Peter Wright

Total rolled product imports in August were down by 28.0 percent on a three-month moving average (3MMA) basis. This was the 10th consecutive month in which imports were down by more than 20 percent compared to the same time last year.

This early look at August’s import volume is based on Commerce Department license data (see explanation below.) This import analysis includes all major steel sectors: sheet, plate, longs and tubulars, with a total of 18 subsectors. All volumes in this analysis are reported in short tons. We use three-month moving averages rather than single-month results to smooth out monthly variability. Next week we will publish our analysis of six flat rolled products broken out into seven regions. The change in imports for individual regions bears little resemblance to the change at the national level.

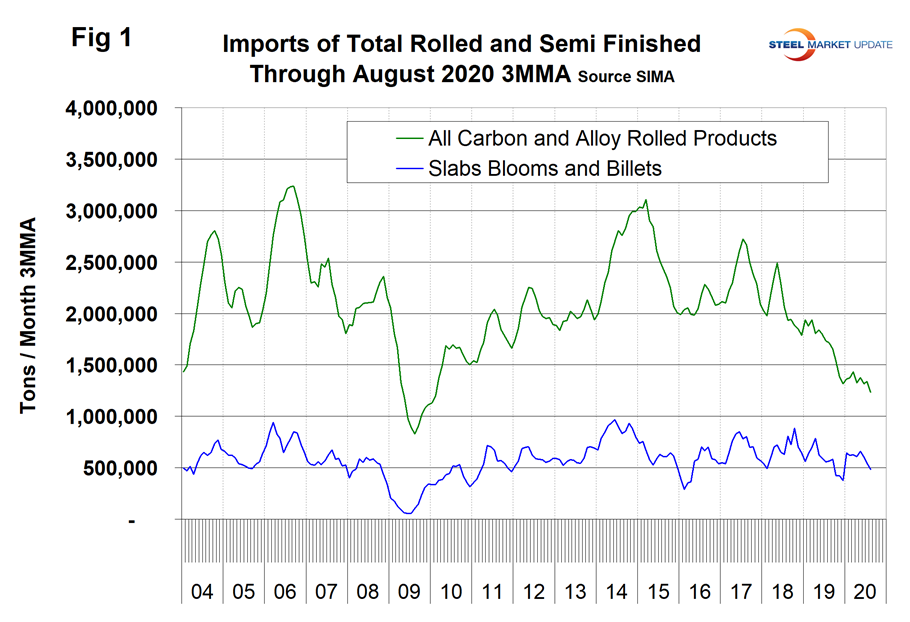

Imports of total carbon and low alloy rolled products in August were 1.1 million tons on a single-month basis, down from 1.3 million in July. From September last year through July this year, the new normal has been a range of 1.24 to 1.56 million tons with August breaking through the bottom of this range. Year over year on a 3MMA basis, sheet products were down by 14.6 percent, plate products were down by 39.6 percent, long products were down by 25.5 percent and tubulars were down by 43.7 percent. Imports of flat rolled, tubulars and longs all had a recent peak in August 2018.

Figure 1 shows the tonnage of total rolled steel and semifinished imports through August on a 3MMA basis. Due to quota opening and closing times, there is a sharp cyclicality within each quarter in the monthly volume of semifinished, which is masked by the 3MMA calculation. Imports of semifinished have recently ranged from a high of 1.5 million tons in January 2020 to a low of 63,000 tons in June 2020. The licensed volume of semis in July was 467,000 tons, but this was revised up to 1,151,000 tons when the preliminary data superseded the licensed data. There were no significant revisions between the licensed and preliminary data of rolled products. Total rolled product volume has been on an erratically downward trend since mid-2017.

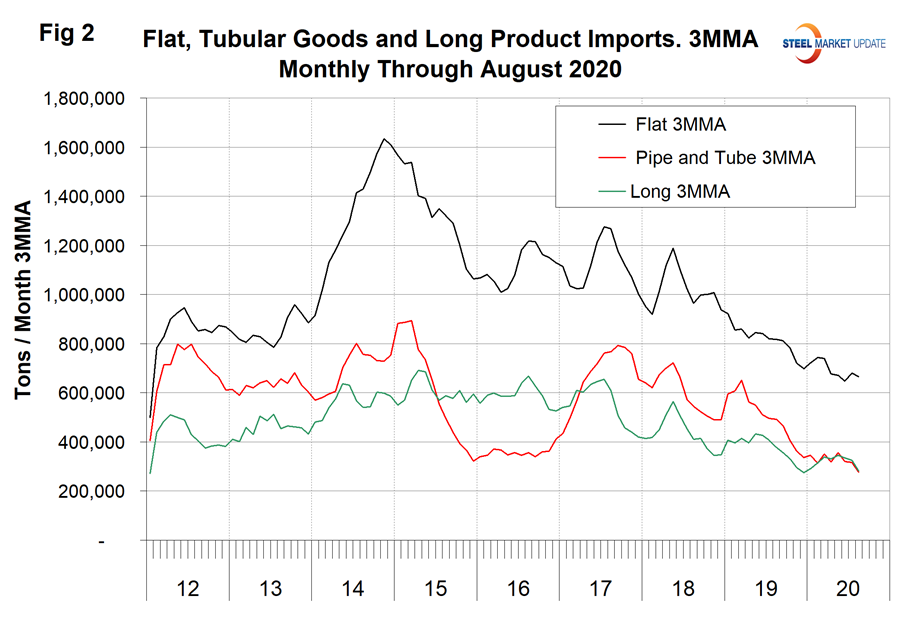

Figure 2 summarizes the import volume of flat rolled, tubular and long products since 2012 on a 3MMA basis. All three have been trending down since mid-2017.

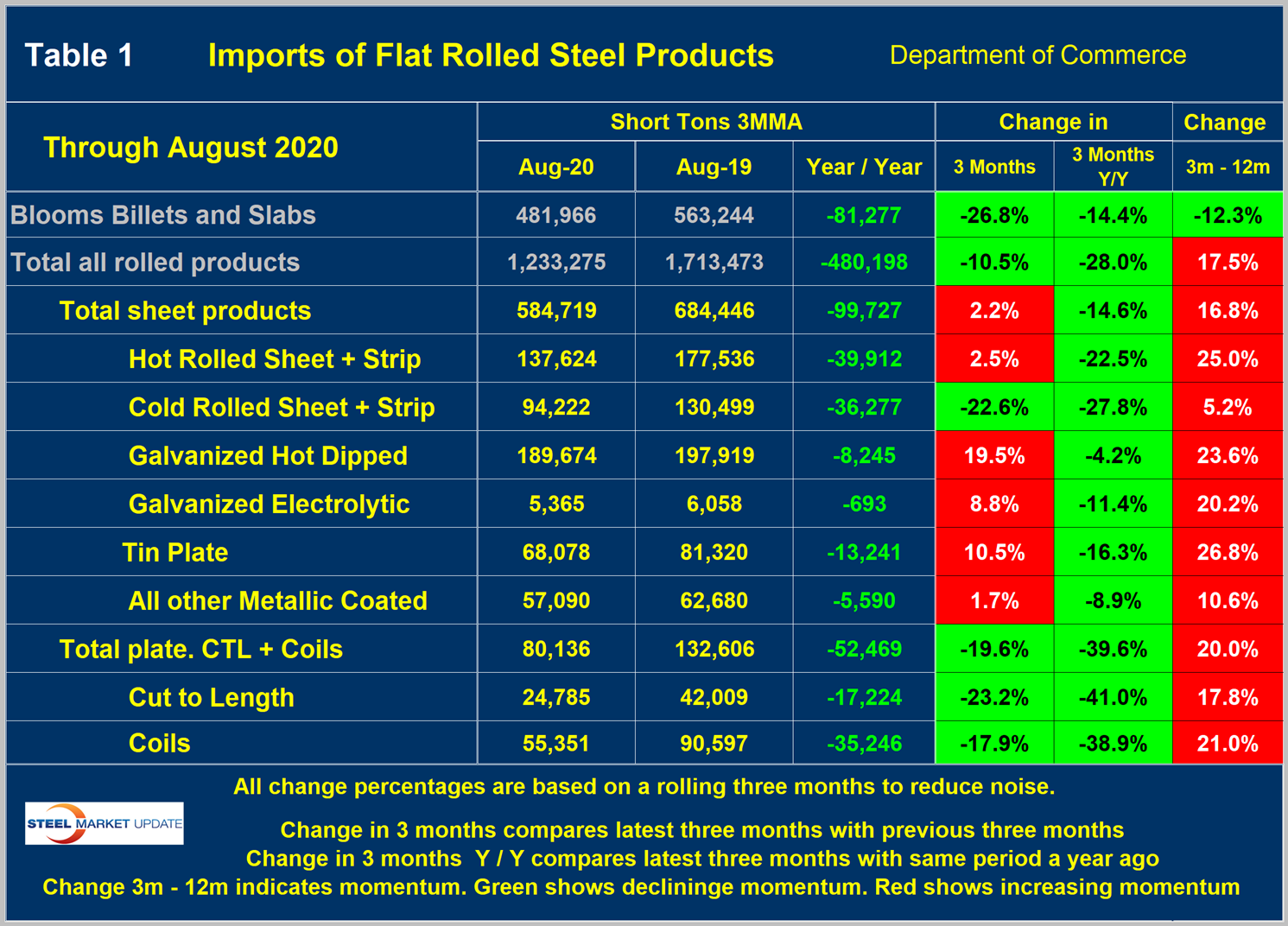

There are three tables in this report. In each of them we show the 3MMA of the tonnage in August 2020 and August 2019 with the year-over-year change in volume. We then calculate the percentage change in volume in the most recent three months with the previous three months. This month we are comparing June through August with March through May (3M/3M). The next column to the right shows the year-over-year change as a percentage. Declines are color coded green and increases are coded red. Finally, in the far-right column, we subtract the year-over-year change from the three-month change. This is a way of describing the recent momentum as a percentage. It is not unusual for the color code of the momentum to be the opposite of the year-over-year time frame analyses as it was in August.

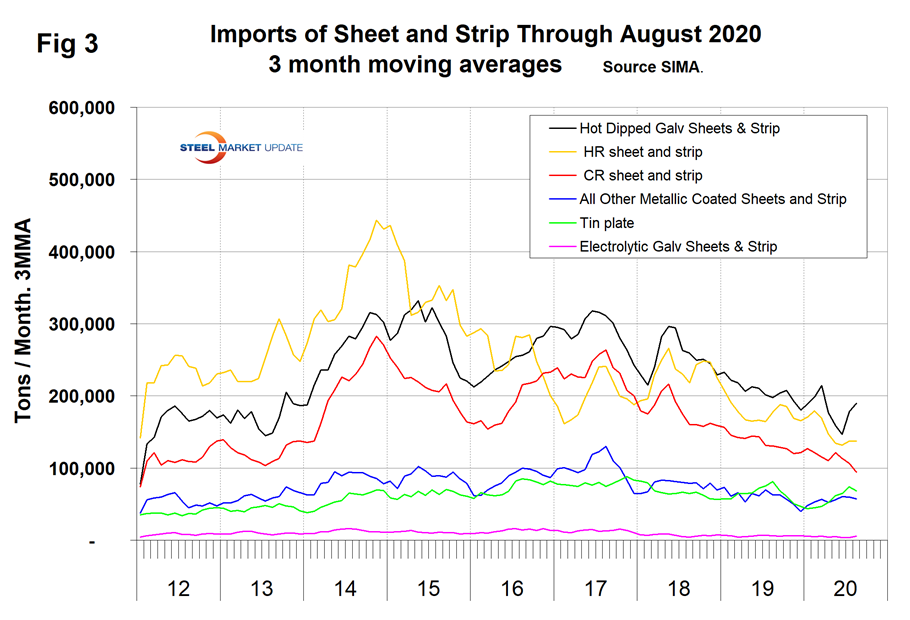

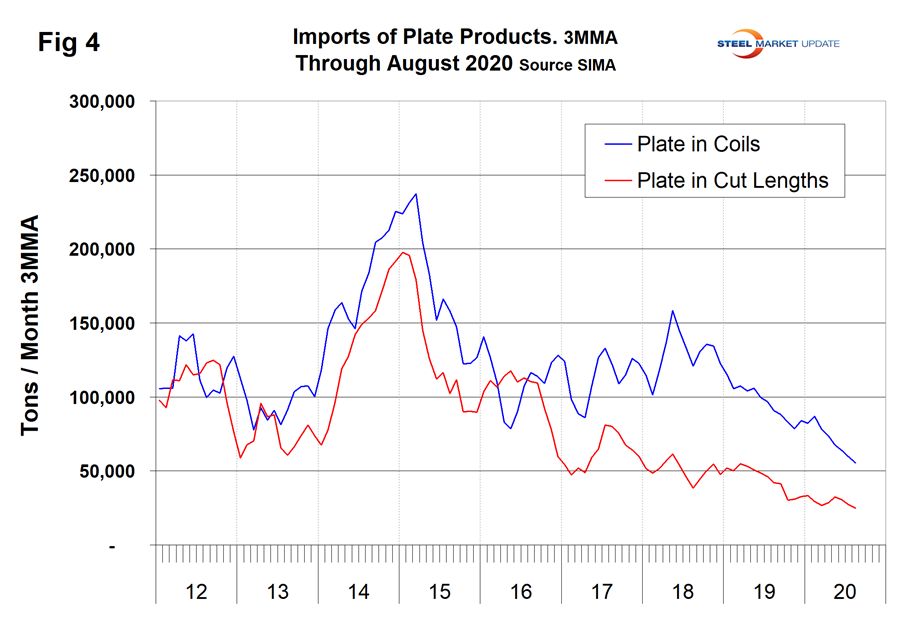

Table 1 describes the imports of all major sectors of the sheet and plate markets. In the flat rolled sectors shown in Table 1, total sheet products were down by 14.6 percent and total plate products were down by 39.6 percent, both year over year. All individual products in the sheet and plate groups were down year over year. Of the three major sheet products, HR, CR and HDG, galvanized was down by much less than hot and cold rolled. In the plate sector, cut to length was down by 41.0 percent and coiled down by 38.9 percent. Figures 3 and 4 show the history of sheet and plate product imports since January 2012.

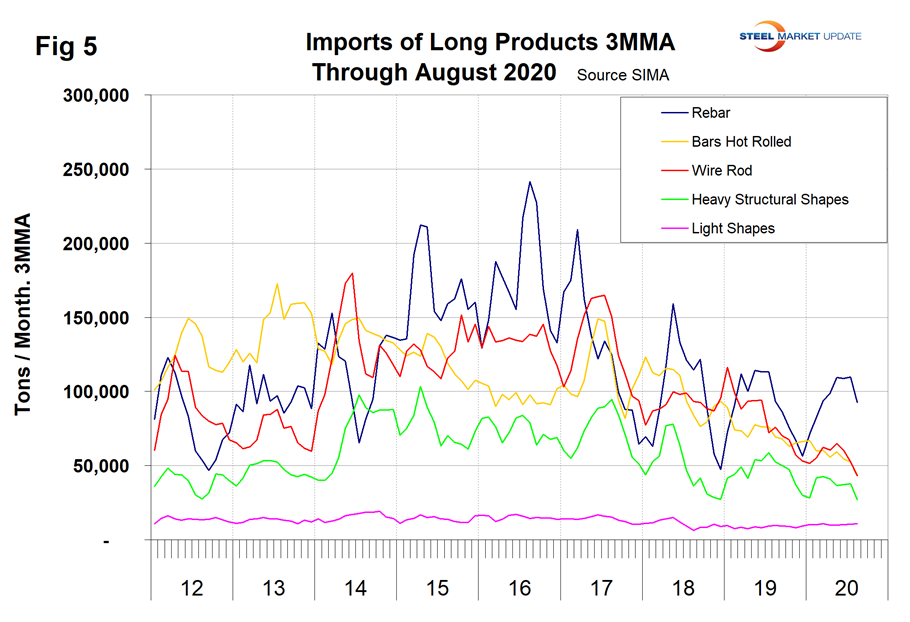

Table 2 shows the same analysis for long products where the year-over year volume was down by 25.5 percent in total. All individual products except light shapes were down year over year, but there were huge differences between long sectors. Rebar was down by only 0.5 percent as heavy structurals were down by 48.5 percent. Figure 5 shows the history of long product imports.

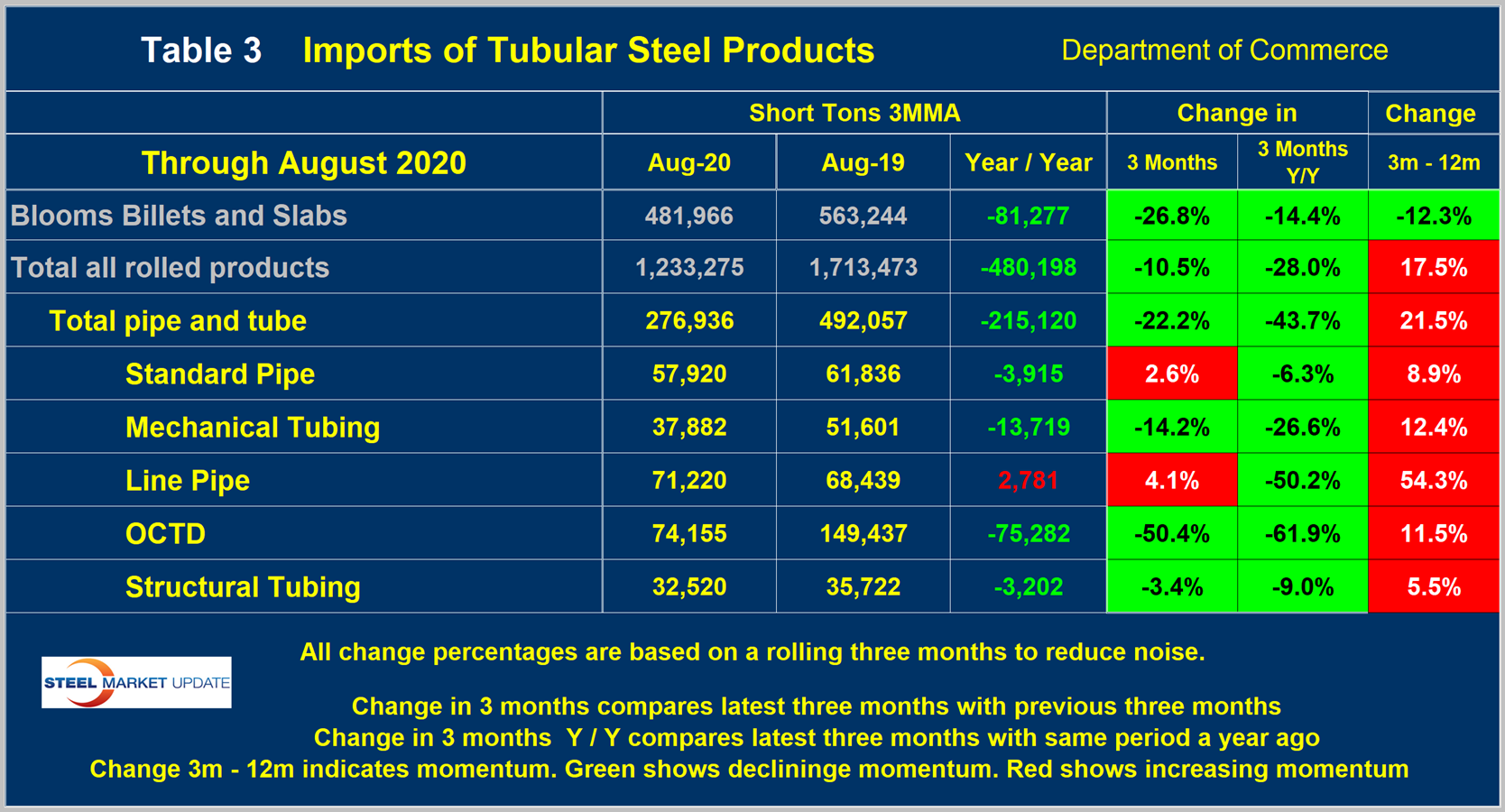

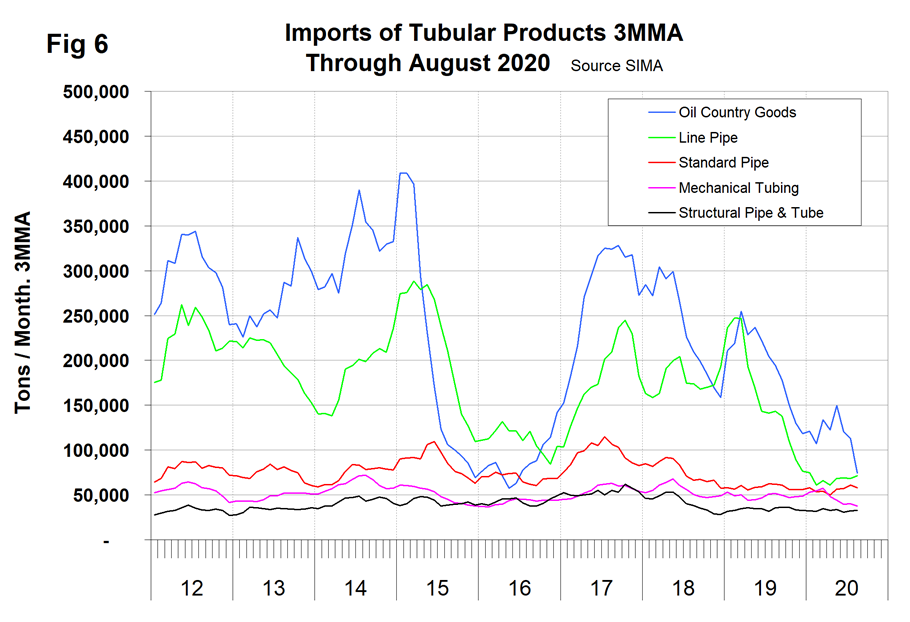

Table 3 shows that for tubular products in total the volume was down by 43.7 percent year-over-year with OCTG down the most at 61.9 percent followed by line pipe at 50.2 percent. Figure 6 shows the history of tubular imports since January 2012.

Explanation: SMU publishes several import reports ranging from this very early look using license data to the very detailed analysis of final volumes by product, by district of entry and by source nation, which is available in the Premium member section of our website. The early look is based on three-month moving averages using the latest license data, either the preliminary or final data for the previous month and final data for earlier months. We recognize that the license data is subject to revisions but believe that by combining it with earlier months in this way gives a reasonably accurate assessment of volume trends by product as early as possible. The main issue with the license data is that the month the tonnage arrives is not always the same month in which the license was recorded.

Statement from the Department of Commerce: The Steel Import Monitoring and Analysis (SIMA) system of the Department of Commerce collects and publishes data of steel mill product imports. By design, this information gives stakeholders valuable information on steel trade with the United States. This is achieved through two tools: the steel licensing program and the steel import monitor. All steel mill imports into the United States require a license issued by the SIMA office. The SIMA Licensing System is an online system for importers to register, apply for and receive licenses in a timely manner. In addition to managing the licensing system, SIMA publishes near-real-time aggregate data on steel mill imports into the United States. These data incorporate information collected from steel license applications and publicly released Census data. The data are displayed in tables and graphs for users to analyze. Additionally, SIMA provides data on U.S. steel mill exports, as well as imports and exports of select downstream steel products.