CRU

January 15, 2021

CRU: Emissions Announcement Pushes Up China Sheet Prices

Written by George Pearson

By CRU Prices Analyst George Pearson, from CRU’s Steel Sheet Products Monitor

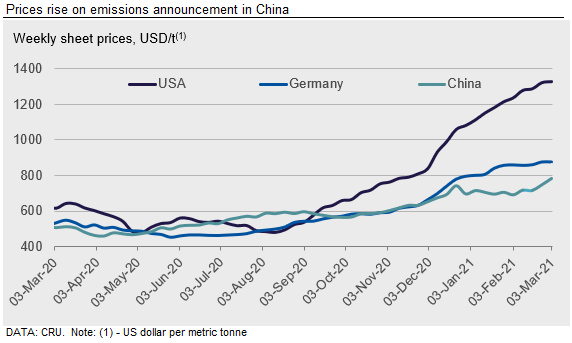

Chinese sheet prices reached a new high this week after a government policy notice on March 2 notifying of emissions production cuts in Tangshan province in late-February to late-March. We expect the impact of this announcement to be lower than the initial price rise suggests. In other regions, sheet prices globally have continued to rise, but at a slower pace.

North America

Sheet prices in the U.S. Midwest continued to increase over the last week, with the expectation that they will continue to rise. Due to limited supply and strong demand, March scrap prices are expected to increase, lending support to higher sheet prices. The recent winter storm that affected many parts of the U.S. has only added to late mill deliveries and lack of availability by limiting production and affecting shipping routes. Some mills have notified buyers there will be no available spot tonnage until June. However, rising domestic production and the arrival of imported material currently presents a downside risk to the price rally.

U.S. West Coast buyers are being forced to rely more heavily on imported material, as CSI and UPI continue to strictly control order entry and the Midwest and Southern mills decline to quote on inquiries due to a lack of availability. Despite very attractive pricing on imports, buyers are hesitant to purchase material with delivery dates in August and September.

Europe

European domestic sheet prices rose by €3–11 /t w/w across all products. Lead times remain similar for both import and domestic orders. New import bookings are for June shipment, arriving in late July or August and European mills are also quoting July-August delivery. CR and HDG coil prices increased more than HR coil prices this week. This continues to reflect the tighter supply of these products. ArcelorMittal announced higher offer prices for CR and HDG coil last week, but not for HR coil. Some HR coil stock in Italy may have been able to be replenished since the beginning of February with import bookings from India and Turkey. However, these offers are no longer there, and Turkish prices have increased again to uncompetitive levels. On the demand side, we have heard that the number of urgent enquiries received from auto OEMs has decreased in recent weeks, suggesting a balance of supply and demand from that sector.

China

Chinese domestic sheet prices jumped by RMB80-200 /t w/w. Although transactions significantly increased w/w as demand recovered after the Chinese New Year holiday, demand from traders was the major contributor to this. Weekly HR and CR sheet inventories at major traders rose by 14% w/w, while inventories at major steel producers fell by 6% w/w.

In addition, Wednesday’s spot market was buoyed by the Tangshan emission control policy. There are two main messages that the policy outlines. Firstly, the policy focuses on enhancing control over emissions for one month from late-February to late-March. We expect this will mainly impact re-rollers in Tangshan in the short-term and the reduction can be offset by output increases in other regions. Secondly, the policy also indicates an annual target to reduce the volume of emissions by 40% y/y in 2021. Some participants see this as a clear sign that steel production will need to be cut significantly to achieve this.

However, we expect this to have a limited impact on the market. The 40% cut in emissions refers to total emissions, not only from steel. Most integrated steel mills in Tangshan have either successfully finished or are in the process of advancing their facilities to meet the ultra-low emission standards. Therefore, contributions would need to come from other sectors like coal, coking, refractories or car emissions rather than from steel. Therefore, we see some room for a correction in the sheet spot market if this buoyant sentiment reduces before the two sessions take place this weekend.

Asia

Sheet prices in the Asia import market continued to increase following higher transactions and a jump in offer levels. CRU assessed HR coil prices at $730 /t, CFR Far East Asia, up by $30 /t w/w. CR coil rose by $40 /t to $840 /t and HDG prices increased by $20 /t to $850 /t. For HR coil SAE1006, deals took place at $720 /t CFR Vietnam at the end of last week, but sellers increased offers this week. Indian and Chinese offers are now at $740-750/t CFR Vietnam. While buyers remain cautious, sellers have been reluctant to sell below $730-735 /t CFR Vietnam. For HR coil/sheet SS400, offers also increased to $740-750 /t CFR Vietnam for Chinese origin material. Buying indications for the same grade were $710 /t CFR Vietnam.

India

Indian domestic sheet prices were relatively unchanged this week, as bearish sentiment continues to prevail in the market with buyers holding back from purchases. Meanwhile, CRU understands that stocks at traders and stockists remain high because they are finding it difficult to sell, even after offering at a significant discount to mill prices. Simultaneously, traders are deferring restocking from mills at current price levels, fearing imports may put further downward pressure on prices. Steelmakers, on the other hand, have increased their export allocation for the coming two months to manage plant inventory. In fact, Indian steelmakers have been heard to increase their HR coil export offers to SE Asian buyers by $15-25 /t w/w to $730-740 /t CFR Vietnam for late-March to early-April shipments. CRU’s market sources suggest that discounts of around $20-30 /t to these prices are being offered to bulk importers, but such deals are hard to come by and not widely repeatable. Given that Indian mills have increased export allocations for the coming few months, the price premium of Indian HRC exports over CIS export sales prices to Vietnam is likely to narrow.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com