CRU

January 15, 2021

CRU: Further Global Sheet Price Gains, Yet Some Weakness Now Emerges

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor

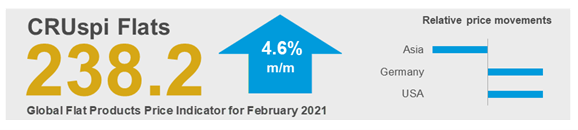

Higher steel sheet prices continue to be assessed across most global markets. Reflecting this, CRU’s Global Flat Products Steel Price Indicator (CRUspi flats), has risen for the seventh consecutive month, reaching 238.2, its highest reading since September 2008. This indicator is now 56% higher than the 2020 average of 152.3.

While sheet prices have continued to rise, the rate of increase in some key markets is slowing, while in others, prices have now fallen m/m. This trend of slower m/m gains is reflected in the CRUspi flats as the m/m increase for February was 4.6%, the weakest gain since August 2020.

Last month, we noted that nearly 30 Mt of had recently been or was in the process of coming online across multiple regions. The vast majority of this volume was restarted BF furnaces that were idled during the COVID-19 lockdowns. One area of note was 4.5 Mt of furnace restarts in Brazil. Before these restarts, Brazil temporarily became a net slab importer, which contributed to recent gains in slab prices. Today, slab prices from Brazil have stabilized at $770 /t, which is $60 /t lower than recent quotes due to the temporary situation of limited supply. Slab export prices from Southeast Asia have been assessed at an even lower level, $665 /t, as a new mill in that market started to sell slabs due to this historically high price.

For sheet products, February price assessments in the Southeast Asian market as well as the domestic Indian markets have fallen back from January levels. In China, prices have become more volatile over the past several weeks with both declines and gains. Over the past few business days while activity is slowing ahead of the weeklong holiday, prices have started to rise from recent lows. This trend has allowed HR coil to increase m/m, yet CR and HDG coil are lower m/m.

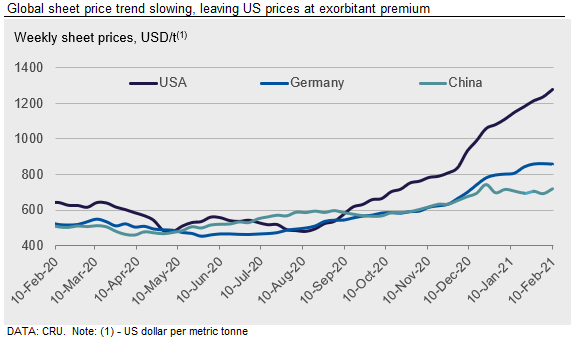

Elsewhere, domestic prices have continued to rise with the strongest gains remaining in the U.S. Midwest market. For HR coil, nominal prices here have risen to a record high of $1,279 /t, a gain of 165% since mid-August. With this rise, U.S. domestic prices are now $492 /t higher than market prices in Europe and Southeast Asia. For perspective, on Aug. 11 last year, U.S. prices were $482 /t, and at that time they were $6 /t below this same global price proxy.

In the European markets, higher sheet prices continue to be assessed, and while the overall rise since the market trough has been as high as 88%, recent m/m price gains have slowed, and a price peak may now be at hand. One fundamental reason for this is due to higher steel production. In fact, the volume of European production today, inclusive of furnaces being prepared to be restarted, is now higher than pre-pandemic levels.

Outlook: Global Price Peak

Sheet demand from the automotive markets has been a visible contributor to the overall rebound in both demand and prices. While global sheet supply continues to come back online from nearly all regions, automotive demand has now shifted from a net positive to a potential demand risk. This global issue is due to a shortage of electronic components, namely semiconductors, which is today negatively affecting sheet demand. Weakness in automotive demand is expected to be primarily isolated to 2021 H1 before becoming a net positive thereafter.

This new demand risk comes as steelmaking raw materials costs have started to fall, with scrap and pig iron falling faster than iron ore. However, our Chinese analysts are becoming more bullish for sheet demand and prices after the Chinese New Year. This view stems from less of a holiday slowdown than normal, due to travel restrictions. Additionally, we are now at the beginning of the 14th Five Year Plan and the 100th anniversary of the Communist Party. The government’s economic policy is expected to focus on stabilizing growth and ensuring a “good starting point” for the new five-year period. Based on this, we expect Chinese prices to fluctuate alongside costs, yet dramatic gains or declines in Chinese demand and prices will be less noticeable this year versus what was seen in 2020.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com