Analysis

February 3, 2021

CPIP Data Shows Rising Construction in December

Written by David Schollaert

Total construction expenditures rose further in December 2020 to $1,490.4 billion, a 1.0 percent gain on the revised November estimate of $1,475.6 billion, according to the U.S. Census Bureau. Despite a health crisis that marred most of 2020, year on year the figure is 5.7 percent above the December 2019 estimate of $1,410.3 billion.

The report goes on to note that the value of construction in 2020 was $1,429.7 billion, 4.7 percent above the $1,365.1 billion spent in 2019. Even though the economy is still in a rebuilding mode and reeling from the effects of the global pandemic, the construction sectors continue to be a bright spot. Construction accounts for about 45 percent of total U.S. steel consumption. See the end of this report for more background on the Construction Put In Place (CPIP) data used in this analysis.

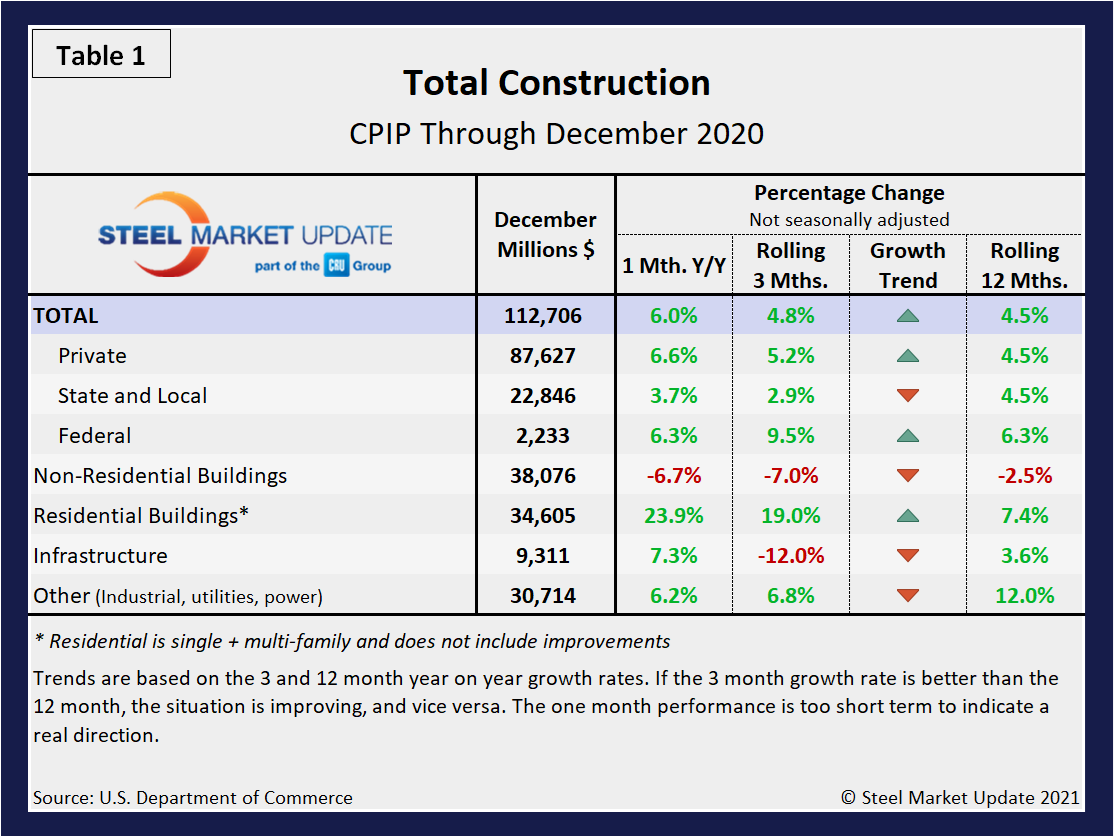

Total Construction

Although construction has been impacted by the global pandemic, it has not suffered nearly as much as manufacturing due largely to pre-funded construction projects. Nevertheless, the positive momentum seen from August 2019 through April 2020 has been steadily eroding since, as seen by the growth trend arrows (Table 1). Through December, only non-residential buildings were noting a decrease on a rolling three- and 12-month basis. State and local, infrastructure and other categories have all been edging down, however. Private, federal and residential construction remain on an upward move, with residential construction still taking center stage.

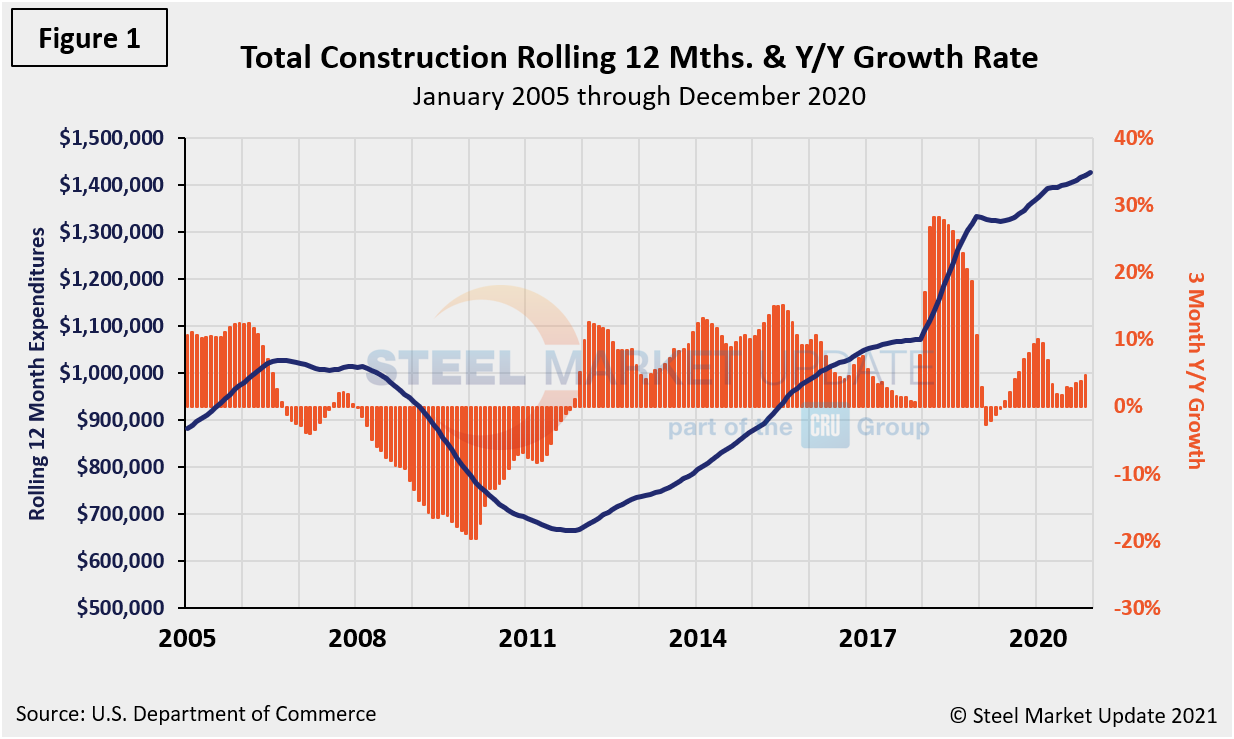

Figures 1, 2, 6, 7 and 9 in this analysis use the same rolling format to smooth out variation and eliminate seasonality. We consider four sectors within total construction: non-residential, residential, infrastructure and other (industrial, utilities and power). Figure 1 shows total construction expenditures on a rolling 12-month basis as the blue line and the rolling three-month year-over-year growth rate as the orange bars.

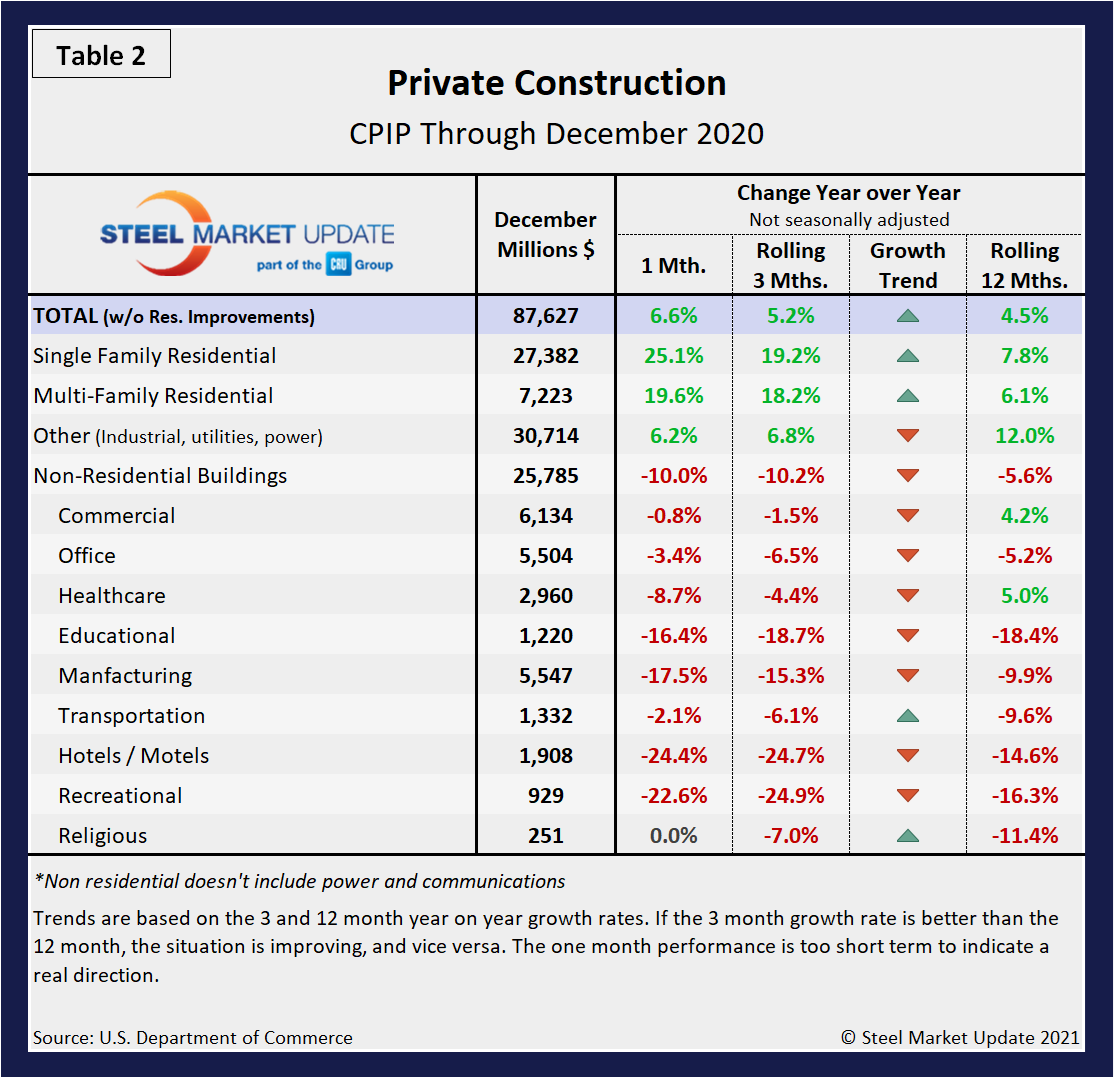

Private Construction

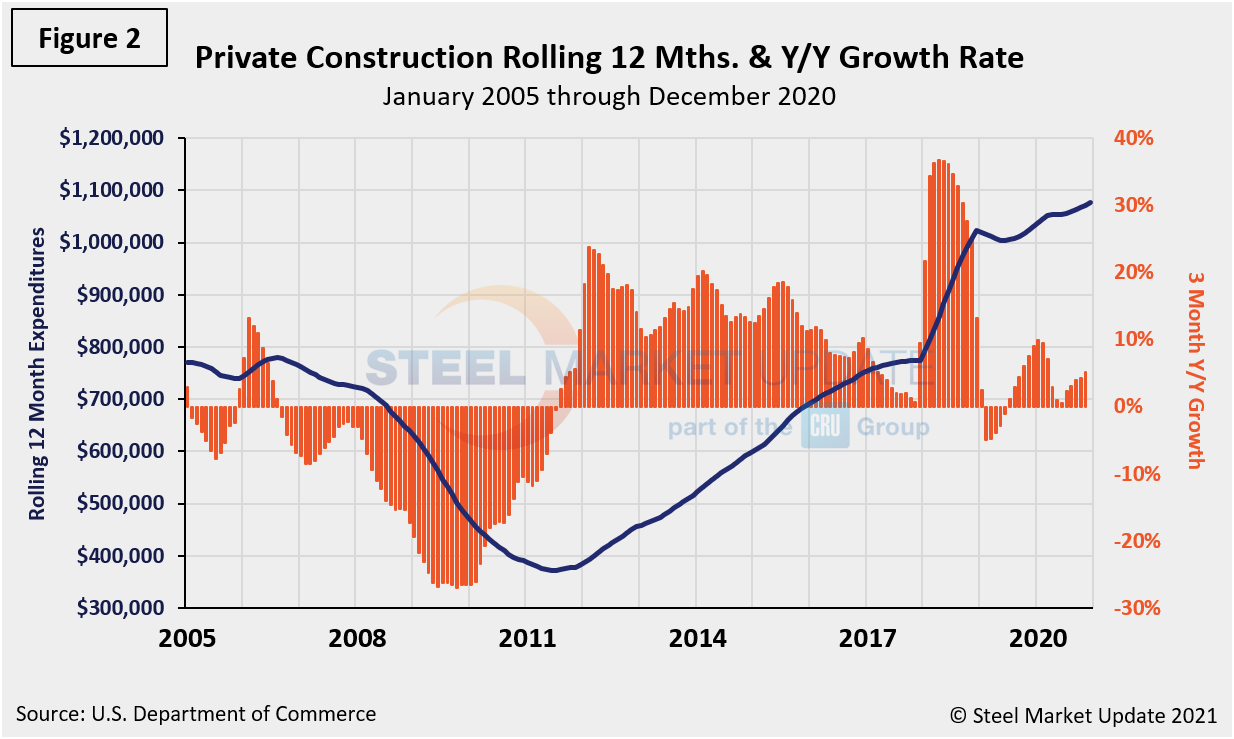

Table 2 shows the breakdown of private expenditures into residential and non-residential and their subsectors. The growth rate of private construction in three months through December 2020 was a negative 10.2 percent, down from a negative 9.2 percent the month prior. Despite the steady fall for non-residential, a strong growth trend in both single- and multi-family residential construction has been notable in maintaining an overall upward trend (Figure 2).

Excluding property improvements, single-family residential expanded by 19.2 percent in three months through December, up from 13.8 percent in November (Table 2). Multi-family residential expanded by 18.2 percent, also with positive momentum. Seven of the nine sectors within non-residential construction remained on a declining trend and momentum was negative for all except transportation and religious buildings. The CPIP that is the main focus of this report is based on spending work as it proceeds; the value of a project is spread out from the project’s start to its completion. The Census Bureau reports separately on construction starts in which data for the whole project is entered into the database when ground is broken

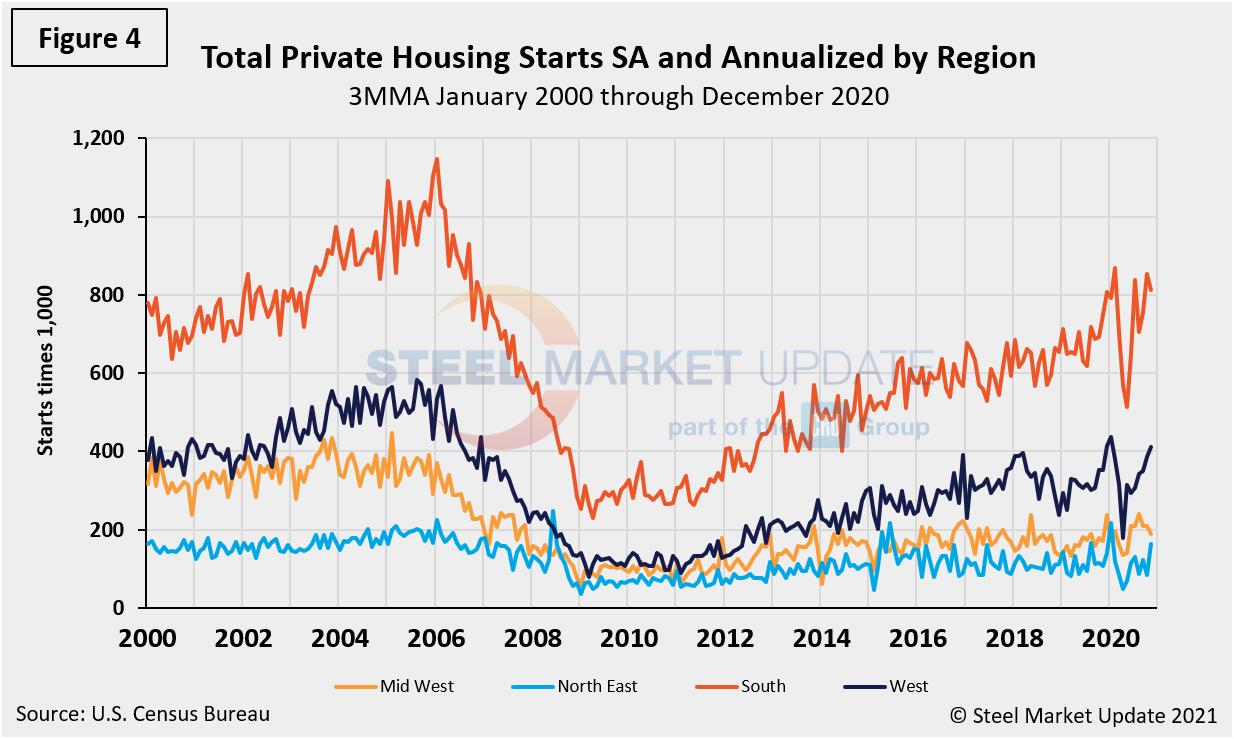

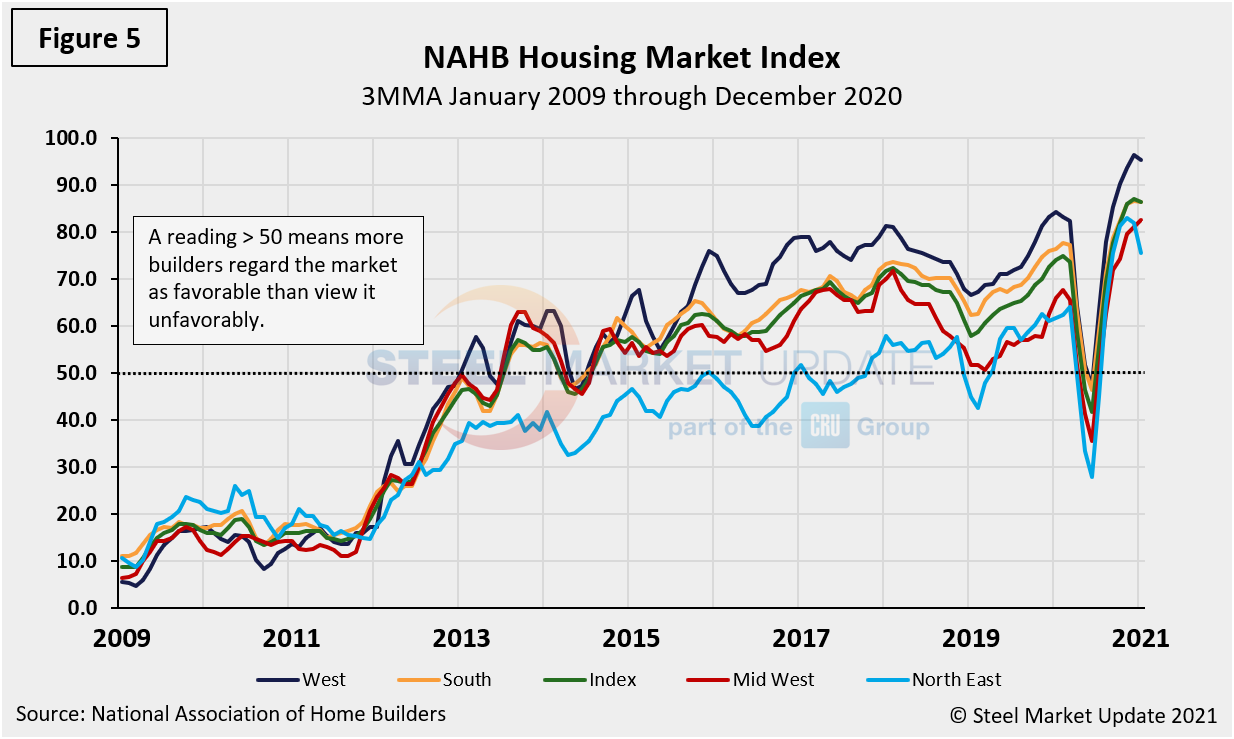

Figure 4 shows total housing starts in four regions with the South being the strongest and the Northeast the weakest. All four regions suffered major declines in 2020 beginning in March but have partially recovered since May. The National Association of Home Builders optimism index crashed in April and recovered each month May through December as shown in Figure 5.

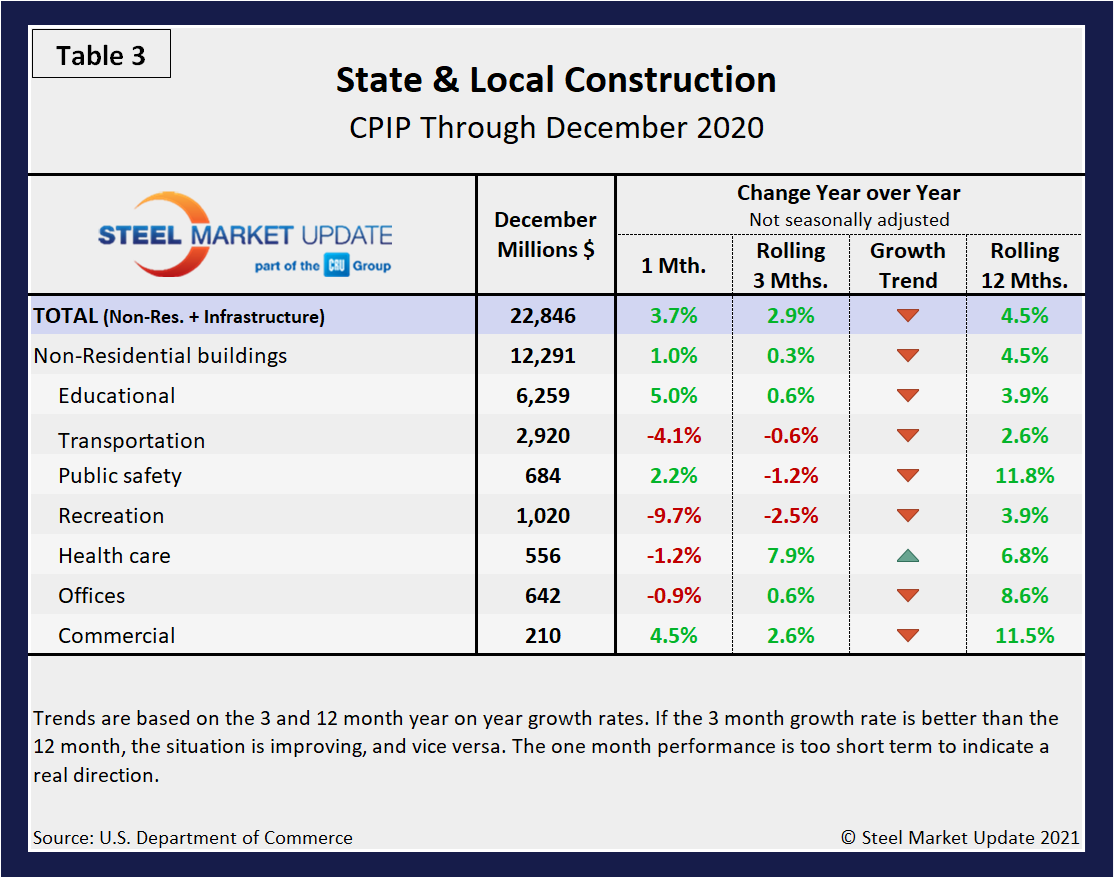

State and Local Construction

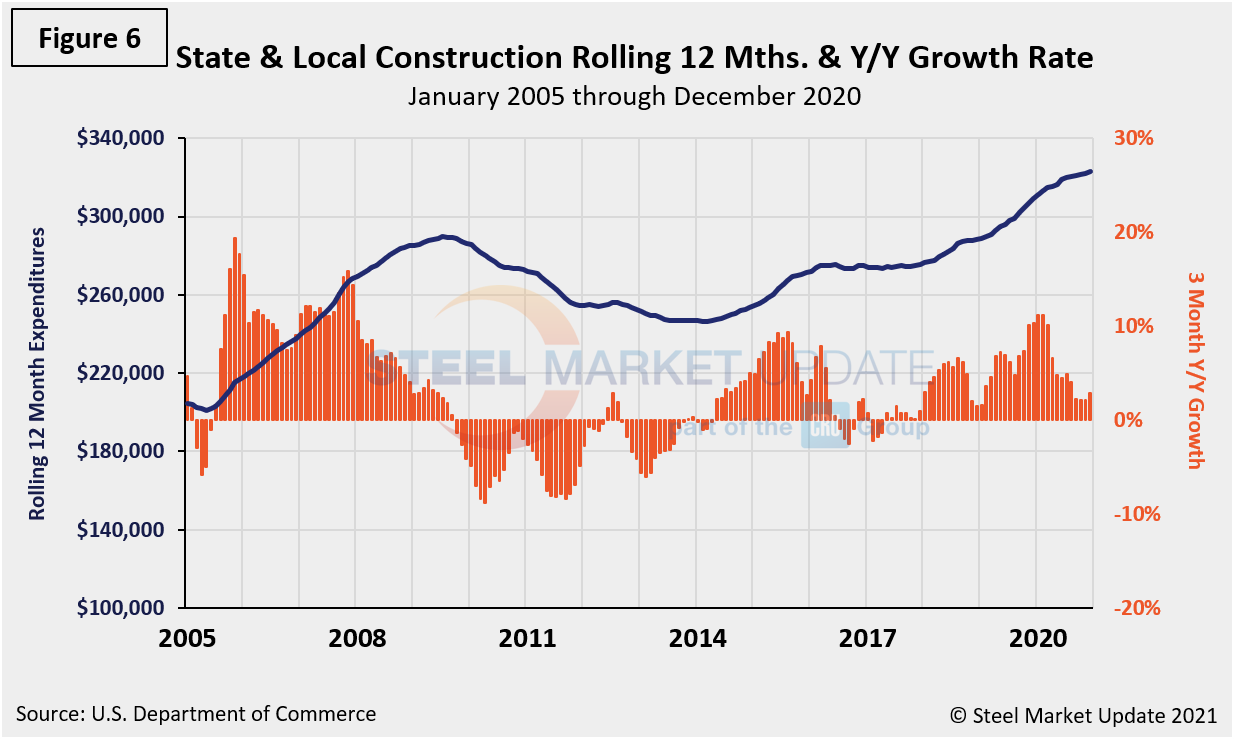

Total S&L expenditures recovered more slowly than private work from the last recession and are again showing a delayed reaction though with largely positive numbers. However, the growth trend remains on the decline (Table 3). In three months through December, only health care had positive momentum. Educational is by far the largest subsector of S&L non-residential buildings at $6.3 billion in December. Figure 6 shows the history of total S&L expenditures.

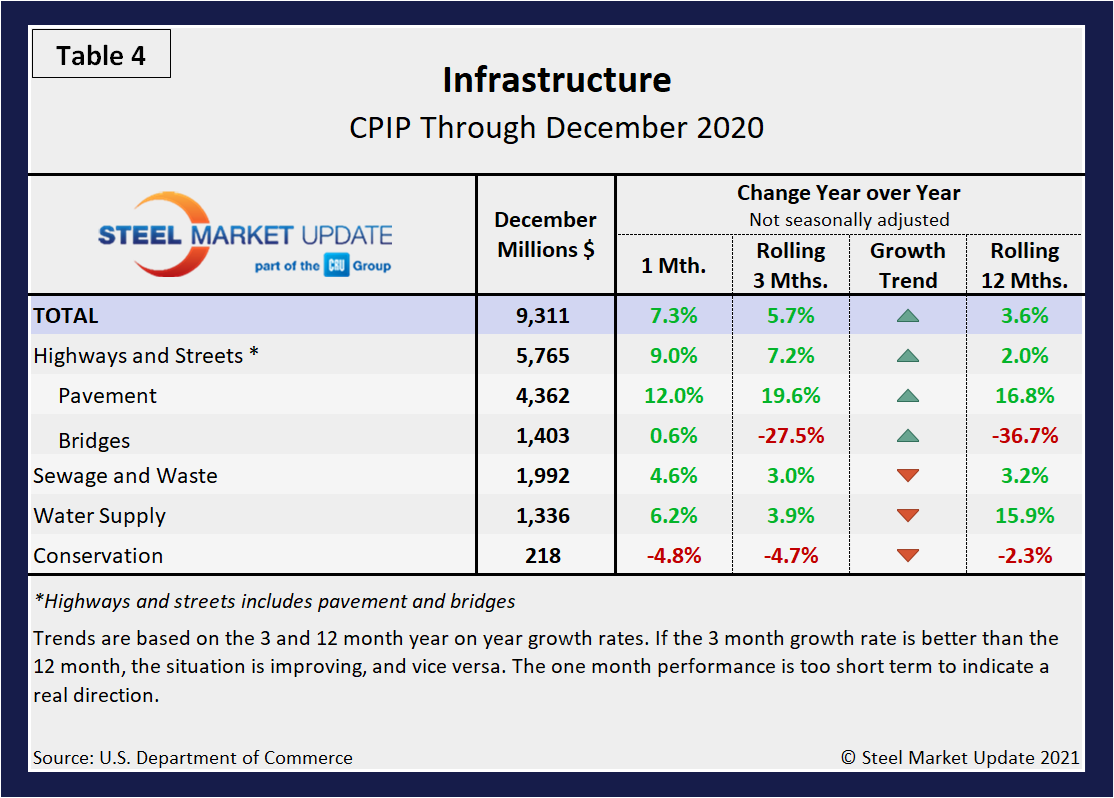

Infrastructure

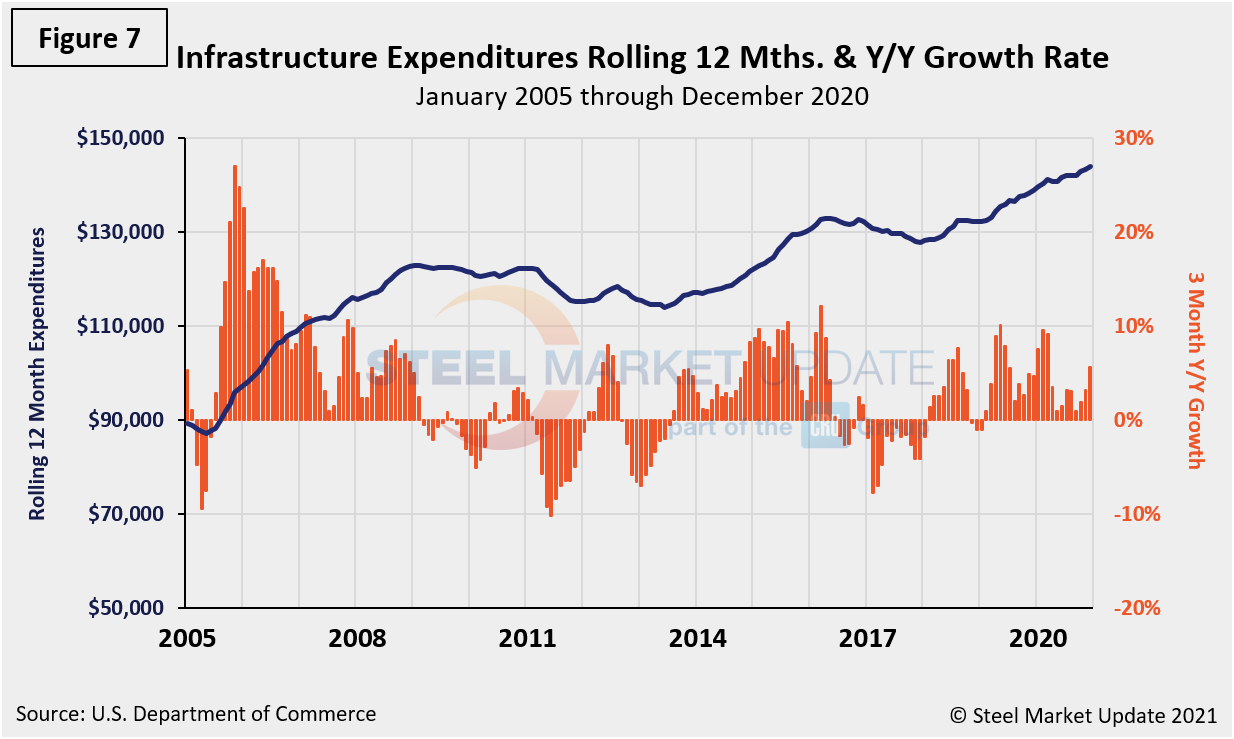

Infrastructure expenditures have seen growth since January 2019. Year over year, the growth of infrastructure expenditures in three months through December was 5.7 percent, up from 3.2 percent the month prior. Highways and streets including pavement and bridges account for almost three-quarters of total infrastructure expenditures. Highway pavement is the main subcomponent of highways and streets and had a 7.2 percent growth in three months through December. Bridge expenditures have had a double-digit contraction rate every month since September 2019. Table 4 shows the breakdown of infrastructure expenditures in three months and 12 months through December and Figure 7 shows the rolling 12-month history of infrastructure expenditures and the year-over-year growth rate.

Total Building Construction Including Residential

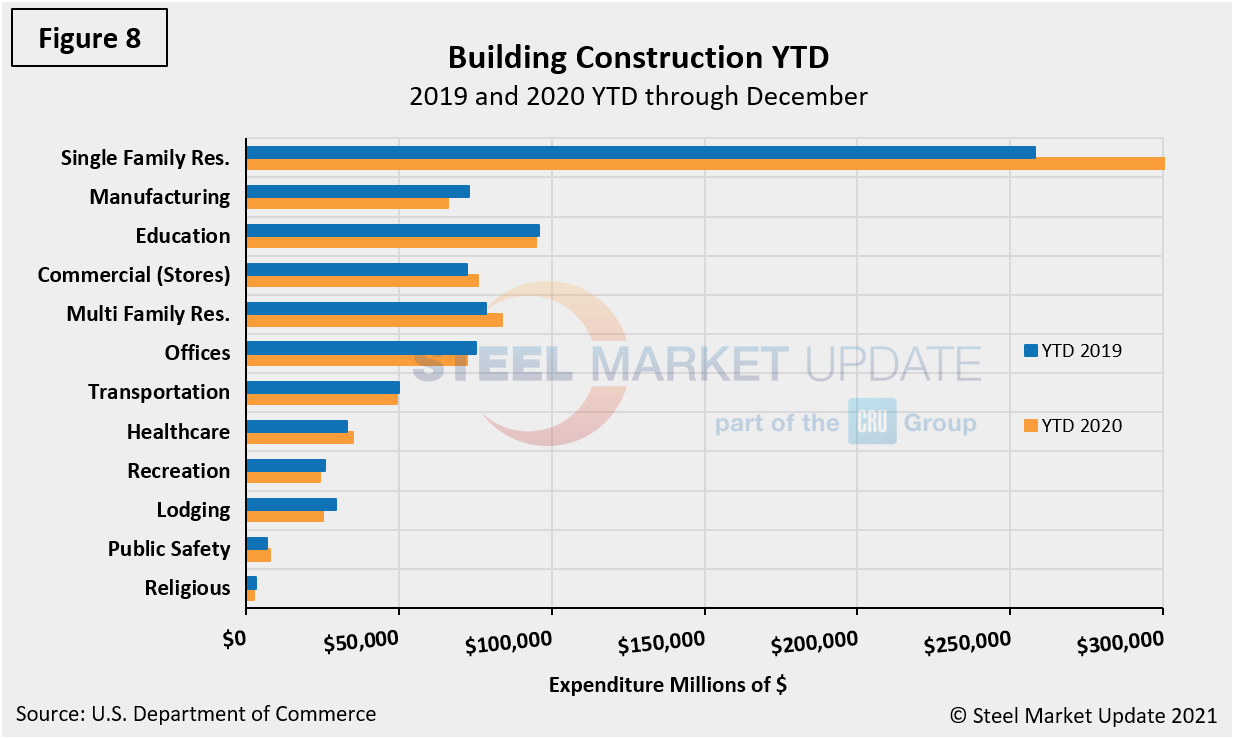

Figure 8 compares year-to-date expenditures for the construction of the various building sectors for 2019 and 2020. Single-family residential is dominant with 2020 expenditures totalling $301.9 billion annualized.

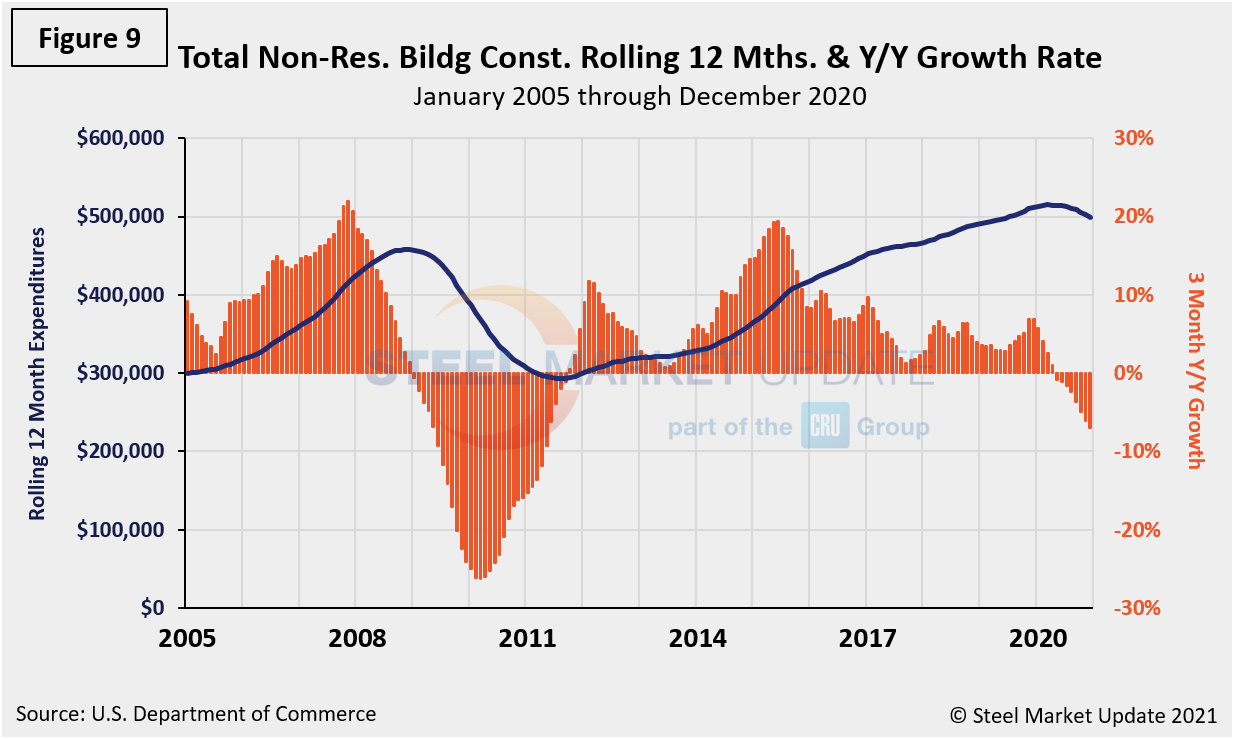

Figure 9 shows total expenditures and growth of non-residential building construction. Growth has slowed every month since November 2019 and in December 2020 reached negative 7.0 percent.

Explanation: Each month, the Commerce Department issues its Construction Put in Place (CPIP) data, usually on the first working day covering activity one month and one day earlier. There are three major categories based on funding source: private, state and local, and federal. Within these three groups are about 120 subcategories of construction projects. At SMU, we analyze the expenditures from the three funding categories to provide a concise summary of the steel-consuming sectors.

By David Schollaert david@steelmarketupdate.com