CRU

March 16, 2021

CRU: China Drives the World Higher

Written by CRU Americas

By CRU Principal Analyst Matt Watkins from CRU’s Global Steel Trade Service

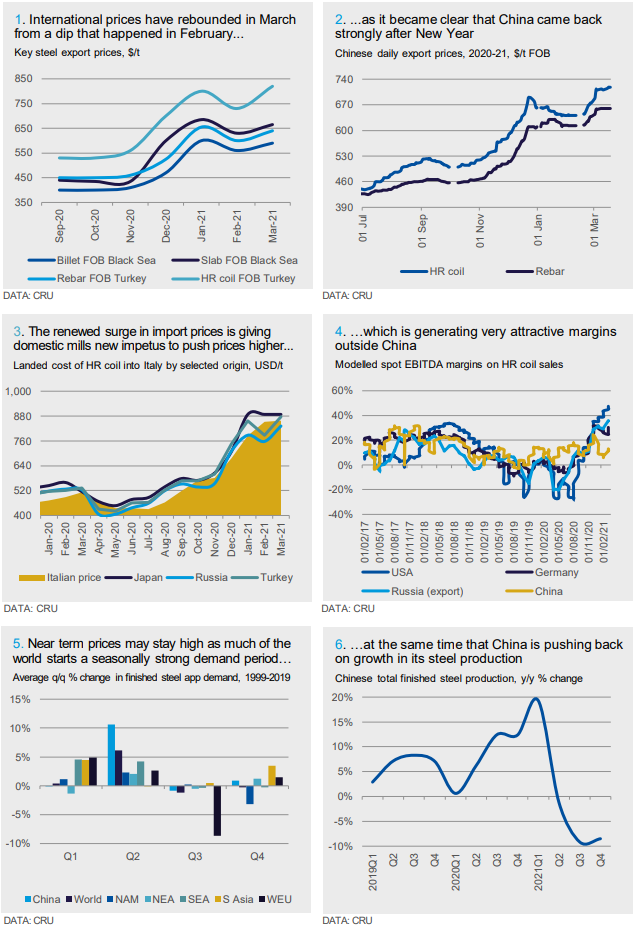

International prices have rebounded in March from a dip that happened in February (see chart 1). Larger m/m gains have occurred in flats than in longs, which have been more impacted by a pullback in scrap costs, but almost all prices are up significantly.

Prices pushed higher as it became clear that China had come back strongly from its New Year holiday. Export prices from China jumped upward immediately after the break (see chart 2) and although these have leveled off more recently, they remain very high.

Rising Import Prices Push Up Domestic Markets

Higher Chinese export prices are supporting higher prices across the wider Asian region and in turn higher export prices from key global suppliers such as the CIS and Turkey. As the temporary threat of a return of price-competitive global imports has receded, domestic mills in several regions have felt empowered to push through further price increases (see chart 3).

This process has its limits. In the USA in particular the scale of domestic price increases over recent months has been such that buyers are actively looking to the import market, even including S232 tariffs and other duties that may be payable. A wave of import volumes is on the way and will arrive in the U.S. over the coming months. Elsewhere this dynamic is not yet so evident. In Europe, import volumes were very low in 2020 and the region’s buyers have become more dependent upon domestic supply. European prices are now heading up rapidly as these buyers are presented with few, if any, price-competitive options.

Margins at Exceptional Highs

Outside China, steel mill margins continue to grow. Spot profitability has reached truly exceptional highs (see chart 4) for which the only historical comparator is 2008. Chinese margins are modest in comparison, though positive and sustainable. Much of the difference comes from China’s higher cost base. China’s mills are paying higher coal costs following the decision to discourage Australian coal. And the global netback system of calculating iron ore prices from a CFR China benchmark is, at today’s high freight rates, providing a relative benefit to steel mills outside China.

Outlook: Near-term Prices Set to Stay Strong

Last month, we highlighted that prices could be supported for longer if Chinese demand was strong after New Year. This is now the case. The near-term outlook is robust. Chinese demand remains strong, for example with recent data points on car and yellow goods production coming out at high levels.

Not only that, but in China as well as many other parts of the world we are entering what is historically a seasonally strong quarter for demand (see chart 5). It is possible that the recovery from lockdowns will in some way affect this normal seasonal pattern, but it is likely that warmer northern hemisphere spring weather will drive strength in outdoor steel demand such as in construction. As such we do expect to see a seasonal pickup.

At the same time, while steel production in many parts of the world continues to rise following last year’s extensive round of idlings and in response to record available margins, in China the government is pushing back on output growth. There have been a set of short-term environmental measures imposed in Tangshan, backed up by some spot government inspections, but there is also a longer-dated goal to reduce steel output in 2021 and more widely to continue China’s efforts to reduce environmental pollution.

For the remainder of 2021, we expect to see y/y falls in Chinese finished steel production (see chart 6). As a base case, we also expect that demand growth will slow as stimulus tapers. This will create a supportive environment for prices, though not necessarily one in which there will be further upward surges. But if demand were to surprise to the upside, it could see China return strongly to the import market this year, which would be likely to keep global prices stronger for longer.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com