Analysis

May 14, 2021

North American Auto Assemblies Tumble in April

Written by David Schollaert

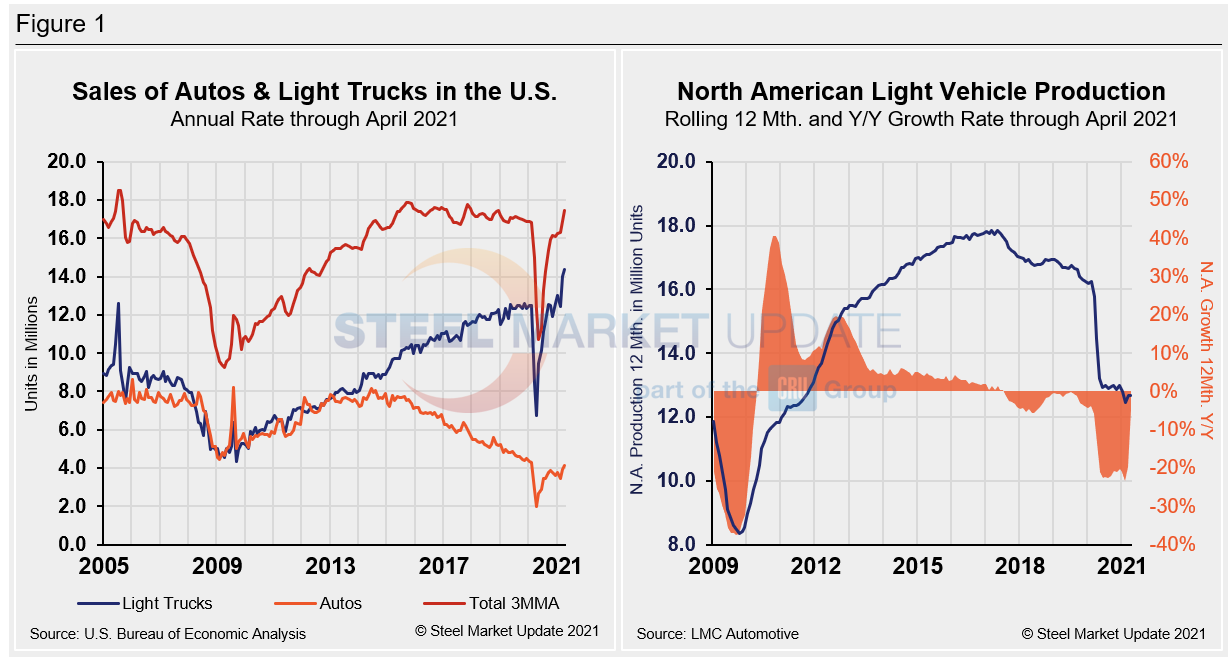

Auto assemblies in North America backpedaled in April as the ongoing shortage of semiconductor chips intensified and hindered automakers’ ability to produce cars and trucks, according to LMC Automotive (LMCA). April’s production totaled 1.087 million units, down from 1.217 million units in March or 10.7%. March saw a bump in auto production—the first in nearly five months—but it was short-lived as the chip shortage impacted April. Further declines are expected in automotive until semiconductor production can catch up with demand.

“Risks remain elevated for additional auto production reductions,” said the LMCA. “Aside from further COVID-related demand disruption, delays to the normalization of semiconductor supply could lead to a deeper than expected contraction in Q2, while continuing disruption in Q3 would limit the available capacity for OEMs to recover earlier ‘lost’ output.”

North American production was up absurdly in April compared to year-ago levels—more than 12,000%—as the auto industry nearly came to a halt due to COVID-19-related shutdowns in 2020, producing only 8,709 units across North America. When comparing the latest data to the equivalent pre-pandemic period in 2019, production is down just 18.7% or 250,191 units. The annual production rate in April was 13.04 million units, down from 14.6 million units the month prior.

Although U.S. automakers continue to work through the effects of the pandemic, chip shortages and supply chain disruptions that have tightened vehicle inventories, U.S. light vehicle sales broke records once again in April, according to LMCA. Despite lean inventories and record high transaction prices, April sales of 1.54 million light vehicles were driven by extraordinary retail demand. The selling rate for U.S. light vehicles reached 18.8 million units, up from 18.0 million units in March, the highest monthly level since 2005. Canada’s light vehicle sales totaled 158,000 units in April, up 232.8% compared to year-ago sales but down from 172,000 units sold in March. Canada’s selling rate was 1.56 million units per year in April, down from 1.9 million units per year in March. Meanwhile, the Mexican market saw sales dip by 14.5% month on month, from 95,000 units sold in March to 83,000 units in April. The annualized selling rate edged up, however, toward 1.15 million units versus 1.11 million units the month prior. For comparison, Figure 1 shows U.S. sales and North American production.

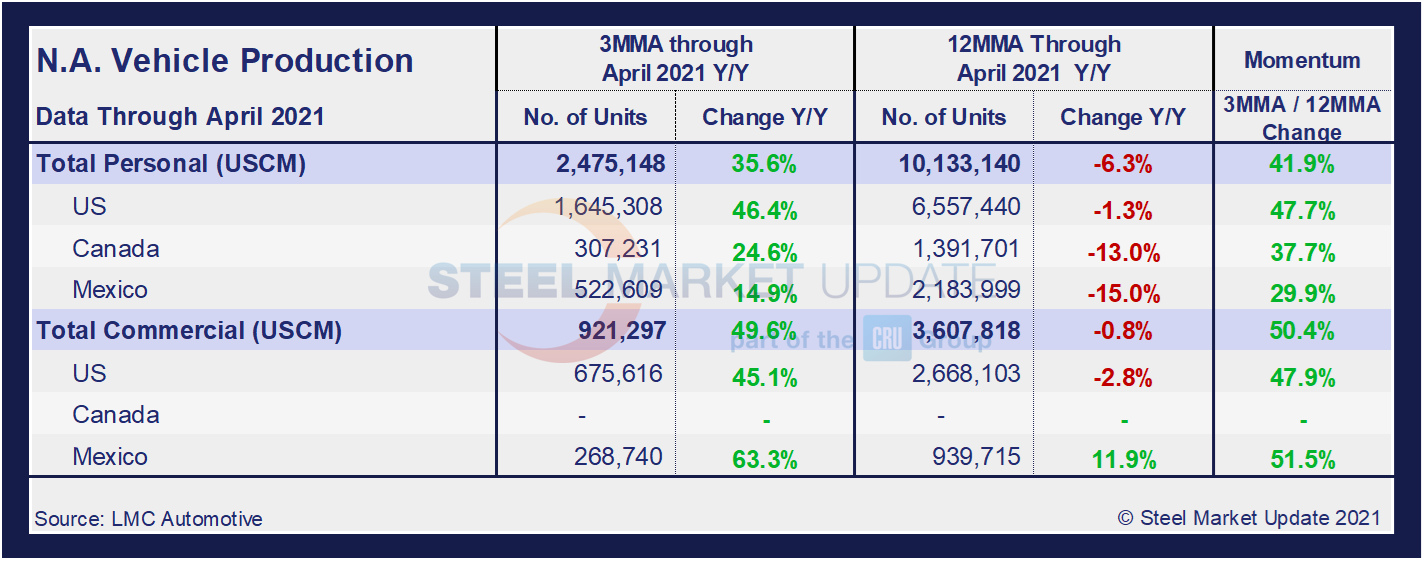

A short-term snapshot of assembly by nation and vehicle type is shown in the table below. It breaks down total North American personal and commercial vehicle production into the U.S, Canadian and Mexican components, along with the three- and 12-month growth rate for each. At the far right it shows the momentum for the total and for each of the three nations. In three months through April, total personal vehicle assemblies in the USMCA region were a positive 35.6% year over year, a significant swing from negative 12.6% the month prior. The year-ago supply chain disruptions from the global health crisis and the more recent chip shortage make yearly comparisons difficult and misleading. Therefore, when compared to April 2019’s pre-pandemic and non-chip-shortage production, current automotive output is behind by 21.1%. Despite the large percentage changes, on a 12MMA year-ago-basis, personal automotive production is down 6.3%, potentially a more indicative view of the auto sector’s performance. Commercial light vehicle assemblies were up 49.6% year over year in April, a surge compared to a positive 5.1% in March, and miles away from the negative 41.6% in April of 2020. But again, when compared to 2019’s pre-COVID-19 output, current production through April is down 12.6%. Note that there has been zero commercial vehicle production in Canada for 16 consecutive months.

Personal Vehicle Production

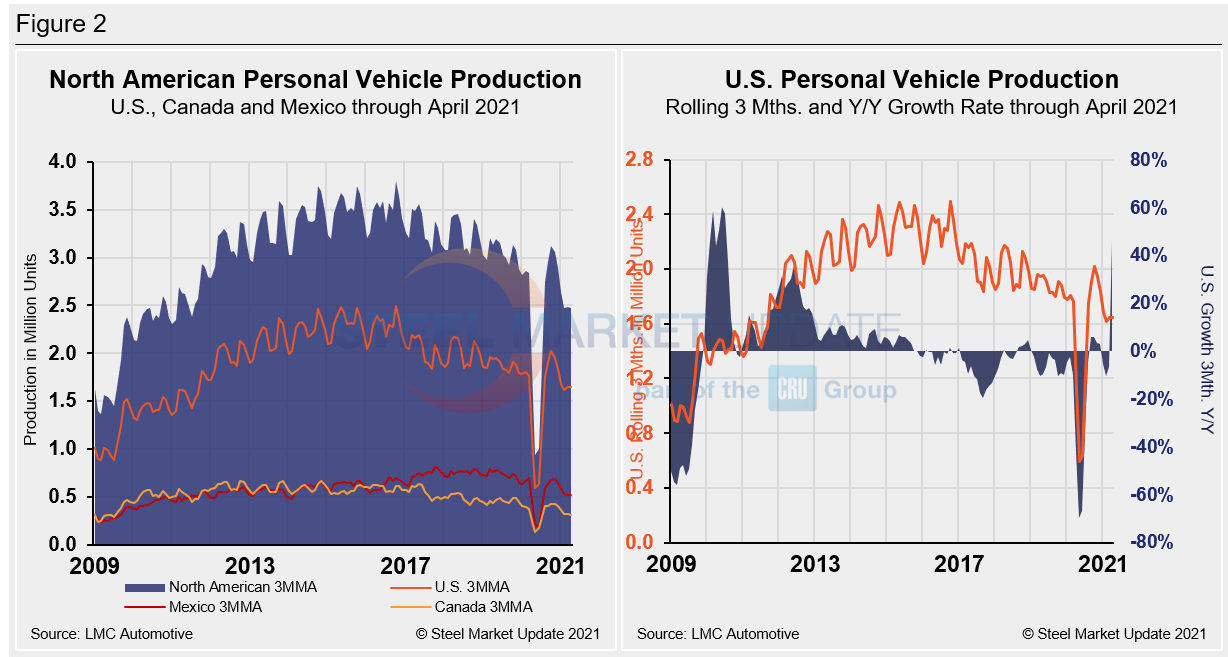

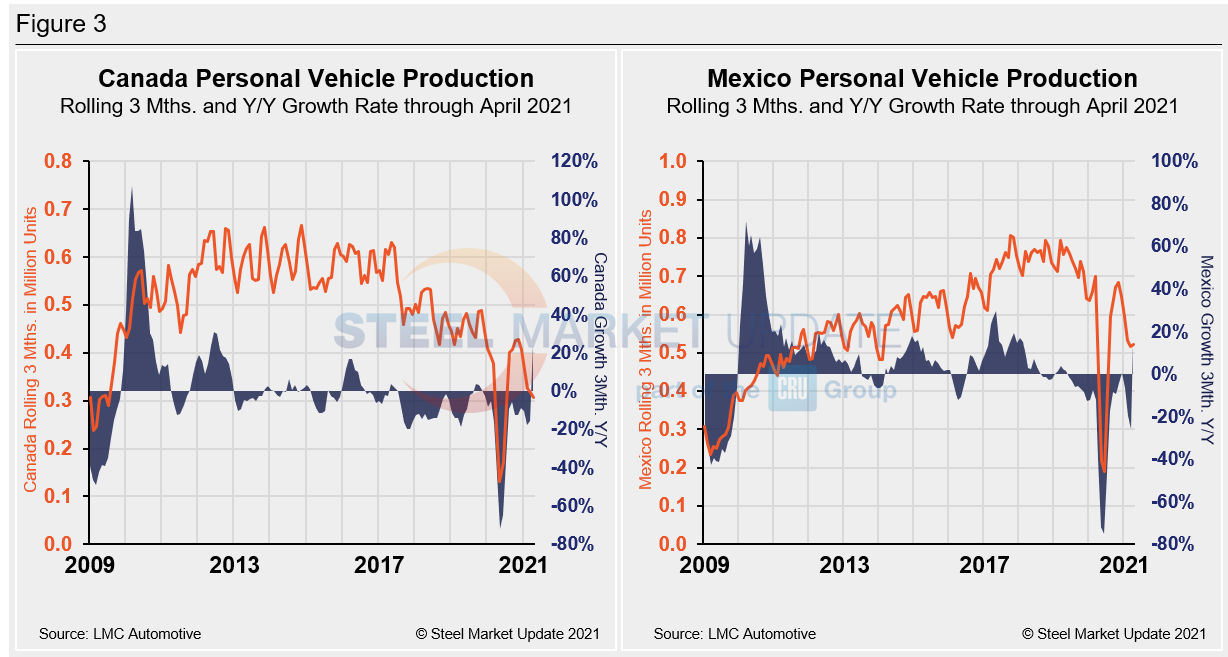

The longer-term picture on personal vehicle production across North America is shown below. The first chart in Figure 2 shows the total personal vehicle production for North America and the total for each nation. The production of personal vehicles in the U.S. and the year-over-year growth rate is displayed in the second chart. Figure 3 shows side-by-side the production of personal vehicles in Canada and Mexico, and the year-over-year growth rate.

In terms of personal vehicle production, Mexico, at 20.0%, was the only North American country to see a positive annual growth rate month on month in April. Both the U.S. and Canada were heavily affected by the chip shortage, as the annual growth rate in the U.S. was down 9.1% in April, while Canada posted a negative 23.6% growth rate in the same period. Canada’s personal vehicle production share of the North American market dipped to 12.4% in April, down from 12.8% the month prior. Mexico carries 21.1% of the market share across the continent, while the U.S. has 66.5% of the North American production share. After seeing its market share slip slightly at the close of 2020 to 63.6%, the U.S. has since rebounded to its highest share since April 2016.

Commercial Vehicle Production

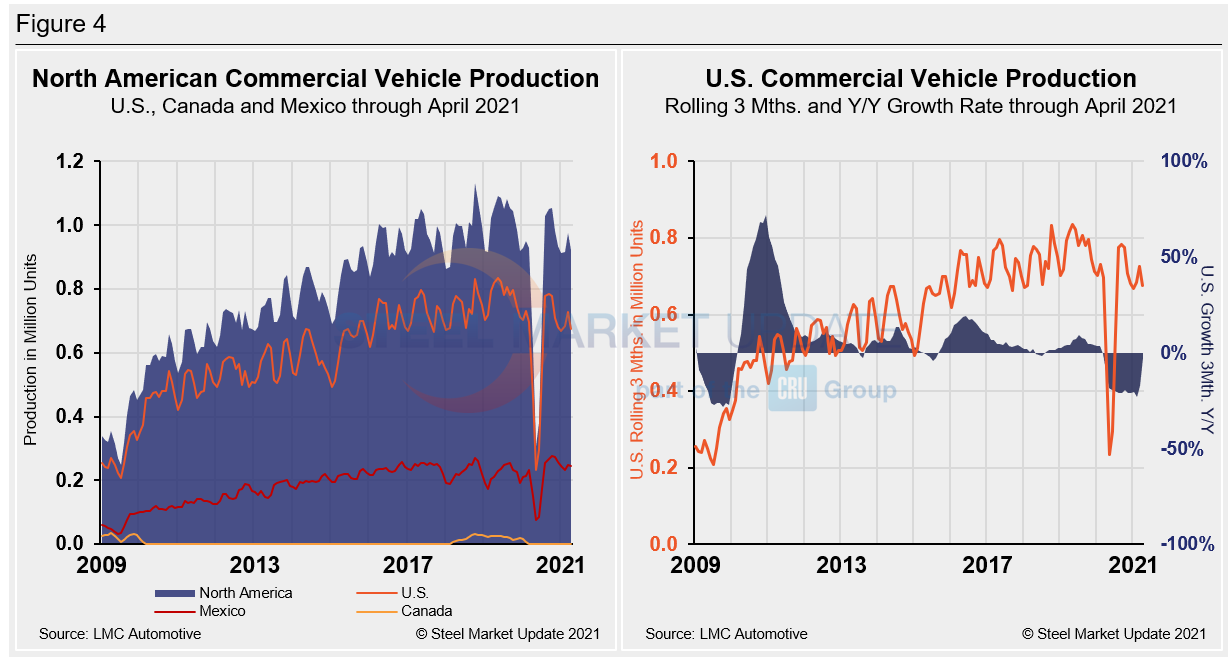

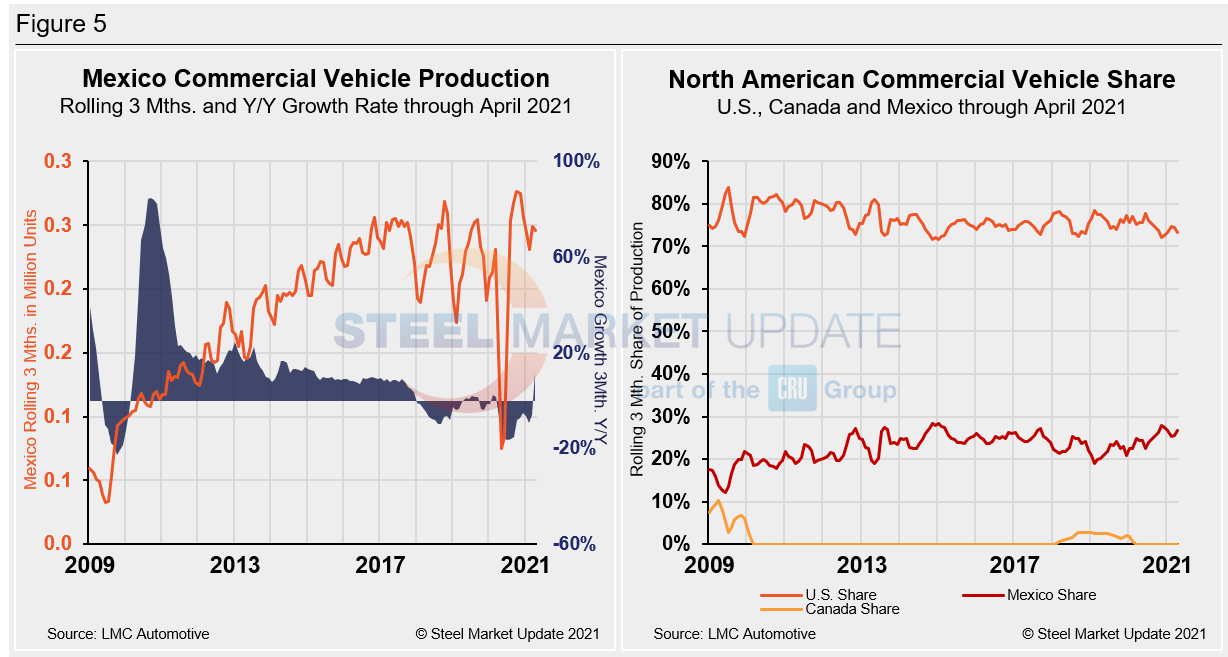

The total commercial vehicle production for North America and the total for each nation on a rolling three-month basis is shown below in the first chart in Figure 4, while the production of commercial vehicles in the U.S and the year-over-year growth rate is displayed in the second chart. Figure 5 shows the production of commercial vehicles and the year-over-year growth rate in Mexico displayed in the first chart, while the second chart shows the production share for each nation. It’s important to note that Canada has not produced a single commercial vehicle over the past 16 consecutive months.

North American commercial vehicle production was down 23.4% on an annual rate in April, compared to the month prior. Despite some production limitations due to pandemic-driven safety measures, the fall is directly related to the shortage of semiconductor chips, primarily in the U.S. Mexico’s commercial vehicle production was down 5.7% on an annual rate month on month in April, while the U.S saw a decrease of 29.4% over the same period. The U.S. share edged down to 73.3% in April from 74.5% the month prior, and down from the most recent high of 77.6% in June 2020. Mexico’s share rose to 26.7% in April, up from 22.4% over the same period. Canada’s share was most recently as high as 3.0% in mid-2019, but has been at zero over the past 16 consecutive months, as Canada hasn’t produced any commercial vehicles over that span. Mexico currently exports about 80% of its light vehicle production, while the U.S and Canada are the highest volume destinations for Mexican exports.

Editor’s Note: This report is based on data from LMC Automotive for automotive assemblies in the U.S., Canada and Mexico. The breakdown of assemblies is “Personal” (cars for personal use) and “Commercial” (light vehicles less than 6.0 metric tons gross vehicle weight rating; heavy trucks and buses are not included). In this report, we describe light vehicle sales in the U.S. and report in detail on assemblies in the three regions of North America.

By David Schollaert, David@SteelMarketUpdate.com