CRU

August 3, 2021

CRU: Iron Ore Falls Below $190/dmt

Written by Erik Hedborg

By CRU Principal Analyst Erik Hedborg, from CRU’s Steelmaking Raw Materials Monitor

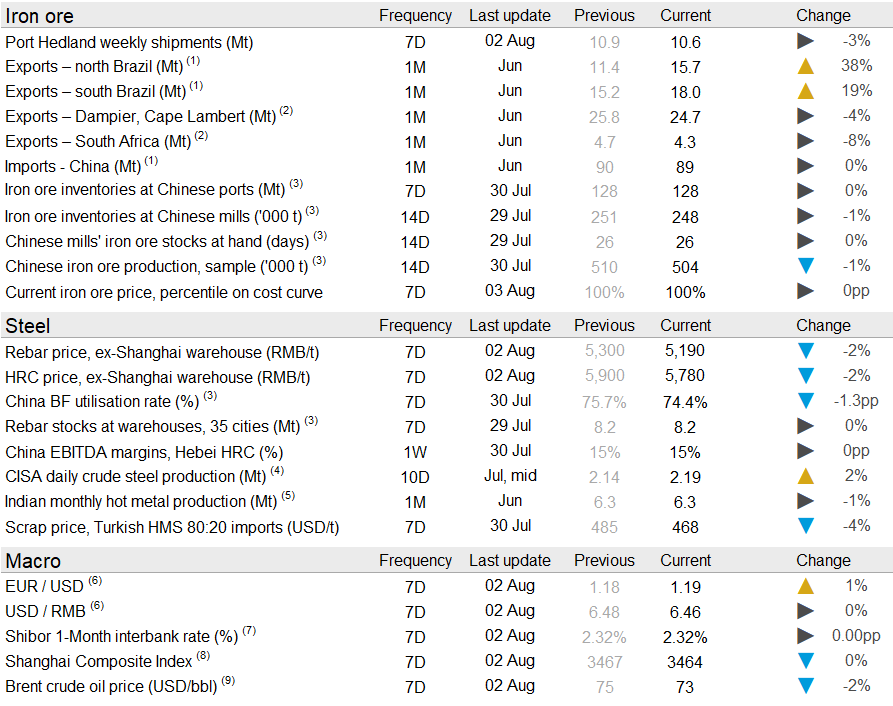

Iron ore has continued its fall by registering a $15 /dmt drop in the past week after steep declines at the end of last week, followed by a slight rebound on Monday and Tuesday. Chinese buying interest has subsided quickly as the number of steelmakers selling contract volumes in the market has increased. On Tuesday, Aug. 3, CRU has assessed the 62% Fe fines price at $185.0 /dmt, nearly $40 /dmt lower than two weeks ago.

Chinese domestic steel prices have fluctuated over the last few days. Following an initial increase last Friday, HRC and rebar prices both plunged on Monday, leading to a decrease of more than RMB100 /t w/w. This was followed by further price falls on Tuesday, meaning steel and iron ore have been moving in opposite directions recently. The reason for the steel price decline is a combination of weaker underlying demand and the expectation of less-than-anticipated crude steel production cuts in 2021 H2. In a recent government meeting, the central government said it would relax its decarbonization efforts somewhat, which means a chance of slightly higher steel production than previously expected. CRU understands that the price moves on Monday and Tuesday were caused by market participants speculating on an ease of production cuts in the energy and steel sectors in 2021 H2.

Although what the government said had an adverse impact on steel prices, it supported steelmaking raw materials prices, despite raw materials consumption continuing to fall. Last week, surveyed hot metal production dropped again by 1.4% w/w due to more steel mills conducting maintenance under the local governments’ request of cutting steel production. This, however, failed to build up iron ore onshore inventories, as port operations were disrupted by Typhoon “In-Fa” and local COVID-19 outbreaks. The vessel queue in China has grown further and is now at 168, the highest level since February. In addition, the demand for premium quality iron ore in China has continued to fall and we are hearing of an increasing number of mills selling contract volumes to smaller steelmakers, particularly higher-grade ore as steelmakers are now increasing their consumption of lower-grade material.

Seaborne iron ore supply improved in the past week. Rio Tinto’s shipments rose to higher levels and we saw high volumes being exported from Vale’s Northern System. Port Hedland shipments declined slightly, but we are seeing a particularly strong performance from FMG in the past two weeks. India’s exports in July fell yet again and reached the lowest level since 2019. Our sources in China have mentioned that many Chinese ports are refusing to accept Indian cargoes due to the heightened COVID-19 risk.

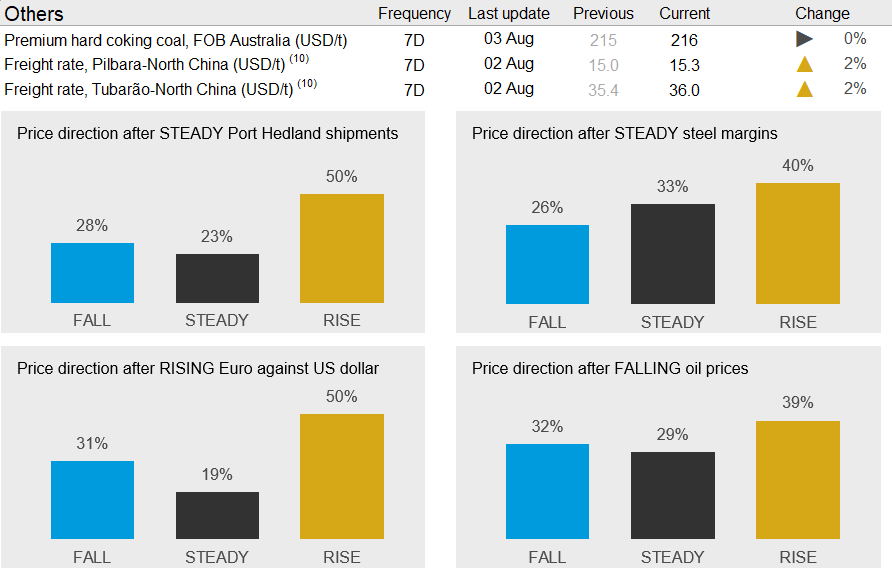

In the next week, we expect iron ore prices to decline further. The price is clearly in a downward trend and the lack of buying interest is going to remain. Steel prices are also in decline as demand appears to have weakened, which means steelmakers will take a cautious stance towards iron ore procurement. The one upside risk we will watch in the next week is the challenge to offload iron ore at ports in China. The vessel queue is already long and if these issues persist, we could see another short-term spike in the iron ore price.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com