CRU

August 7, 2021

CRU: Grading the Infrastructure Bill for Aluminum Demand Potential

Written by Greg Wittbecker

By Greg Wittbecker, Advisor, CRU Analysis

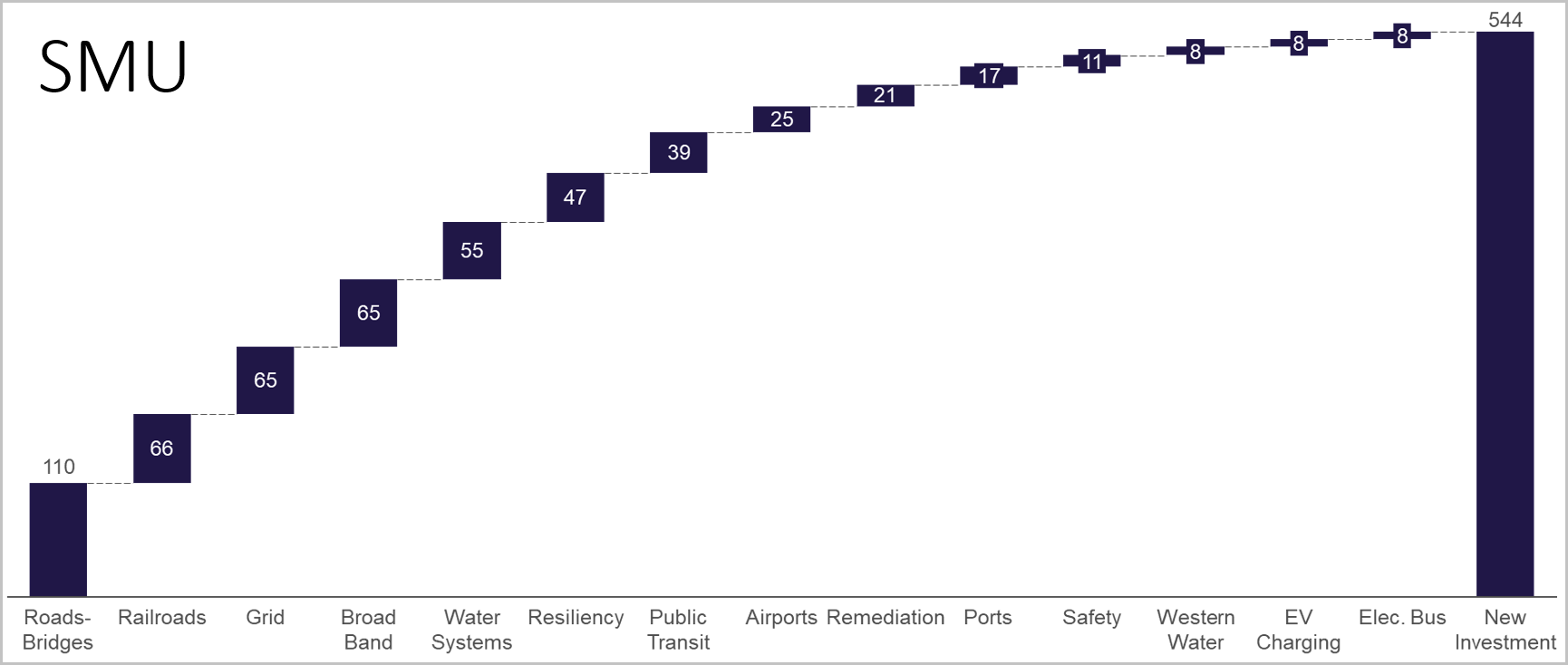

The $1.2 trillion infrastructure bill promises to deliver about $550 million in actual new investment. The breakdown of that investment looks as follow.

Aluminum and steel have superior sustainability advantages and should exploit them. Clearly, the steel industry is cheering the passage as much as the aluminum industry. Both sectors will enjoy a lot of incremental demand. The Biden administration’s mantra of “build back better” and an emphasis on climate change can be especially positive for both industries. Both have a huge competitive edge in sustainable production, particularly in recycling. This is an advantage that we’d expect both industries to really press. When materials choices are being made, shouldn’t aluminum and steel clearly win vis-à-vis plastics and other petroleum-based alternatives? If the goal is to decarbonize and reduce our dependency on fossil fuels, what better way to do that than to use metals which are infinitely recyclable. It’s a unique and powerful message.

How Does Aluminum Fare with the Bill?

Aluminum is such a versatile metal it is likely to appear in many of the major categories above. Let’s briefly cite some of the applications that could benefit:

Roads and bridges: Lighting fixtures, signage and even some basic structural parts where resistance to corrosion is sought.

Railroads: The bill is focusing on passenger upgrades in which lightweight, high-strength cars will be in play. An emphasis on electrified trains in the Northeast corridor creates demand for aluminum cable within medium- and high-voltage catenary systems.

Grid: A huge opportunity for aluminum, where 100% of the overhead transmission lines are comprised of ACSR (Aluminum Core Steel Reinforced) cable. The biggest hurdle will be fast-tracking regulatory approvals for both retrofitting old lines and building new lines.

Broadband: Fiber optic will dominate, of course, but switch gear employing aluminum will come into play

Water Systems: PVC, concentrate and copper likely will get a lot of the investment, but aluminum castings for metering systems will be important

Resiliency: This is focused on cyber security and remedial actions to combat climate change. Aluminum extrusions are a big part of thermal management in high-end services. Investment in new security systems means more server farm capacity and could deliver more demand pull.

Public transit: Another big win for aluminum, which is often dubbed “the metal of motion.” Upgrades to aging buses, subway and urban rail systems could be a boon to sheet, plate, extrusions and castings.

Airports: Much of the emphasis here is on the air traffic control system, which may be system-oriented. Again, some server applications could benefit. If towers are literally being replaced, you could see aluminum curtain wall enjoy some good business.

Remediation: It sounds dull, but clean-up of Superfund sites could actually be a nice win for the aluminum sector by utilizing some of its legacy bauxite residues (which are highly alkaline) to remediate acid run-off from defunct coal mining areas.

Ports: Similar to airports, with a surge in warehousing space, is the opportunity for high speed conveyor systems.

Safety: Hard to pinpoint much here.

Western water infrastructure: Pumps, irrigation and diversion piping.

EV charging: It’s low voltage, so not an obvious win for aluminum wire and cable, but thermal management of the units could deliver some extrusion demand plus structures to house the charging ports.

Electric bus: Like public transit, a huge opportunity. Lightweight electric buses are running in China now. Lots of aluminum applications in body panels, chassis and forged wheels.

The situation in flat rolled products is equally tight. All domestic rolling mills are running flat out. Antidumping actions on common alloy aluminum sheet from 18 countries have cut import supply and enabled domestic mills to fully load their capacity into first-quarter 2022.

On balance, the infrastructure bill delivers great potential to aluminum, and it should be complementary to steel.

What’s important now is getting to the right decisionmakers designing and appropriating money to make the right choice for both metals.

Greg Wittbecker joined CRU in January 2018 after retiring from Alcoa, where he was Vice President of Industry Analysis and Managing Director of Alcoa Beijing Trading, based in Shanghai, China. His career spans 35 years in the aluminum industry, having also held senior commercial and management roles at Cargill, Wise Metals and Koch Supply and Trading. Greg brings perspective on the entire aluminum supply chain from bauxite to aluminum finished products and will be a regular contributor to SMU going forward. He can be reached at gregory.wittbecker@crugroup.com

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com