CRU

September 16, 2021

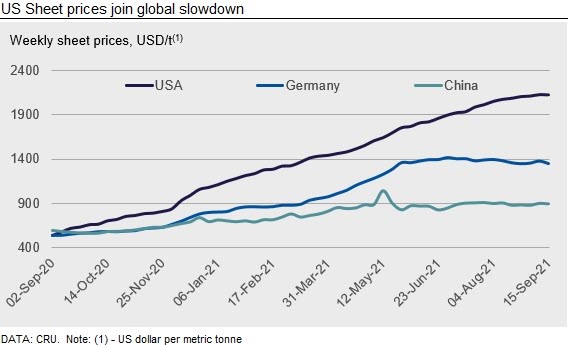

CRU: U.S. Sheet Prices Join Global Slowdown

Written by Ryan McKinley

By CRU Senior Editor Ryan McKinley, from CRU’s Steel Sheet Products Monitor

Steel sheet prices were either little changed or fell w/w across most of the globe, with the U.S. market now joining in the global cooldown. Prices in the U.S. fell w/w for the first time in over year, albeit the decline was only by $2 /s.ton and the amount of material purchased was limited. In Europe, prices fell substantially as less expensive offers from other areas of the world forced domestic mills to lower their own selling prices. While elevated freight costs buoyed prices in some countries in Asia, Chinese prices fell w/w as unexpectedly weak demand conditions turn the market there increasingly bearish. This same bearish sentiment occurred in India, where domestic buyers are withholding bids because they sense prices have more room to fall.

USA

HR coil prices in the USA posted a slight fall of $2 /s.ton w/w, with a larger variance in spot pricing reported last week. While spot volumes were within normal levels, there was a drop in the amount of material purchased. This is most likely due to the large amount of material already on order and the unwillingness of mills to quote on new inquiries. Demand is still expected to remain strong through 2021 Q4, although the continued supply shortages that are disrupting production in several market segments have led to some concern that we may see more of a seasonal slowdown than previously expected.

Steel sheet prices remained unchanged on the U.S. West Coast this week as buyers await the opening of December order books. While some companies have experienced a slight softening in sales volumes over the past two weeks, most are optimistic that demand in 2021 Q4 will remain strong. Many buyers have limited their mill purchases to material needed to fulfil sales orders that have already been accepted at replacement cost levels.

Europe

European sheet prices have shown substantial decreases this week, particularly in Germany where a downwards correction can be seen across all sheet products. German HR coil fell by €17 /t w/w to €1140 /t, CR coil down by €30 /t w/w to €1250 /t and HDG decreased by €20 /t w/w to €1270 /t in our latest assessment. One of the drivers for the drop in prices these last couple of weeks has been the availability of cheaper imports. Lower priced material of Indian, Turkish and Russian origin has appeared in the European market.

Automotive contract negotiations for next year are underway, although settlements between local mills and buyers have yet to be reached in what are expected to be prolonged discussions. Our forecast remains one where prices fall over the rest of 2021, and an early start for the automotive contract negotiations indicates mills are trying to convince buyers to lock in as soon as possible.

China

Chinese domestic sheet prices trended downward this week. Underlying sheet demand has stayed weak and expectations of a weaker-than-expected Q3 continue to keep market sentiment bearish. The latest NBS statistics reported that manufacturing IP grew by 5.5% y/y in August, slower than the 6.2% growth in July. Meanwhile, domestic auto production continued to fall, decreasing by 19% y/y in August due to semiconductor shortages. As the negative impact on sheet demand from slower manufacturing is likely to continue, concerns over weaker-than-expected September and October demand conditions have started to impact prices. Although transactions are slow, significant production restrictions have resulted in a reduction in sheet inventories by 3% w/w.

Although demand will likely be weaker than earlier in the year, lower production costs will still keep mill margins high.

Asia

The prices of imported sheet products in Asia slightly increased due to rising freight costs.

Indian mills raised their HR coil offer to $920-925 /t CFR Vietnam this week while buying interest remained thin. According to market sources, Vietnamese rerollers are also facing tough competition in the export market from India and Turkey for HDG coil.

During the week, two domestic steel mills in Vietnam also announced their new offers. Formosa Ha Tinh lowered their HR coil offer by $35/t m/m to $920/t CFR Vietnam and Hoa Phat’s offers stand at $900/t CFR Vietnam.

CRU assessed HR coil prices at $910 /t, CFR Far East Asia, a $10/t rise w/w. CR coil prices were assessed at $1,150 /t CFR Far East Asia, flat w/w, while HDG prices were assessed at $1,170 /t CFR Far East Asia, unchanged w/w.

India

Indian sheet prices are unchanged w/w following sharp corrections in prices of downstream sheet products last week because of weak buying sentiment. Key buyers of CR coil and coated sheet have stayed away from spot buying, while traders are reluctant to build stock at current price levels as price declines in the future are likely. For steelmakers, a sharp decline in sheet offtake from automakers because of ongoing production cuts due to semiconductor shortages has led to a rise in mill inventory, forcing them to offer discounts to boost buying. This is despite a consistent rise in input cost due to an upsurge in coking coal prices, which are now hovering in the range of $360-365 /t CFR India, up by over $60 /t w/w.

Moreover, Indian steelmakers are offering larger volumes of HR coil for export to the Middle East, Turkey, and NE Asian markets, with there being limited opportunity to sell into traditional export markets of Europe and SE Asia. Steelmakers are hopeful for an uptrend in prices in the coming month as seasonal domestic restocking is accompanied by increased interest from importers as China further reduces its exports.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com