Analysis

October 7, 2021

Dodge Momentum Index Recovers in September

Written by David Schollaert

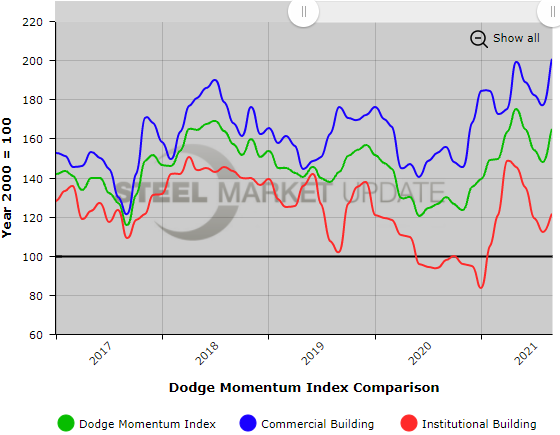

The Dodge Momentum Index rebounded in September after contracting for three successive months. The index registered 164.9 in September, an 11% gain against the revised August reading of 148.0, according to data and analytics from the Dodge Construction Network.

![]()

The improved Momentum Index in September suggests developers are looking past the current concerns over pricing, Delta and politics, and are moving forward with nonresidential building projects and planning to meet demand. The commercial planning component increased by 13% in September, while the institutional component rose 8%.

This does not mean there are no challenges ahead for the construction sector. Nonresidential building projects entering planning staged a solid recovery in early 2021, as the economy reopened from the COVID lockdowns. Entering summer, however, those gains turned to losses as higher material prices and shortages of labor and goods weighed on building activity.

The strength in projects entering planning was widespread last month. Most sectors were moving higher, excluding healthcare, which experienced a downshift in the dollar value of planning projects in recent months. The Momentum Index was 30% higher in September when compared to the same year-ago period. The commercial component was up 32%, while institutional planning was 25% higher.

The Dodge Momentum Index is a key advance indicator of nonresidential construction demand, leading construction spending by as much as a year. The report noted that a total of 17 projects with a value of $100 million or more entered planning during September. The leading commercial projects were the $500 million “The Star” office building in Los Angeles, Calif., and a $250 million office project in Cambridge, Mass. The leading institutional projects were the first and third phases of a lab facility in Boston, Mass., valued at $450 million and $225 million, respectively.

An interactive history of the Dodge Momentum Index is available here on our website; an example is shown below. If you need assistance logging into or navigating the website, please contact us at info@SteelMarketUpdate.com.