CRU

October 24, 2021

CRU: Key Insights from CRU Breakfast 2021

Written by Alex Tuckett

In this year’s edition of CRU Breakfast – part of LME Week – we explored three key themes that shaped the commodities markets – the global economic and commodities outlook, the changing role of China, and Navigating ESG. All three themes have been central to many developments in the industry and remain equally crucial moving forward into 2022.

2022 Outlook: Is the Commodities Boom Here to Stay?

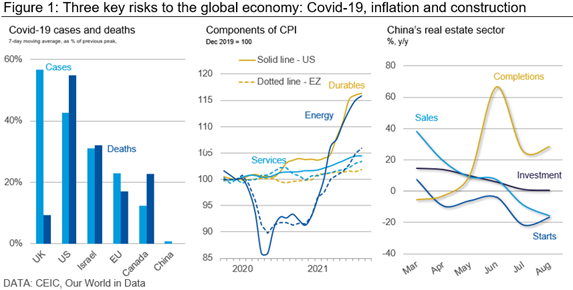

We expect a robust economic recovery to continue into 2022, with global GDP expected to expand by 4.8%. However, we see three major risks to the economy in 2022:

- The Delta variant: vaccination remains far too uneven to write off Covid-19 yet

- Inflation, driven by supply-chain shortages but potentially also the labor market

- Construction, particularly in China where the cycle appears to be turning

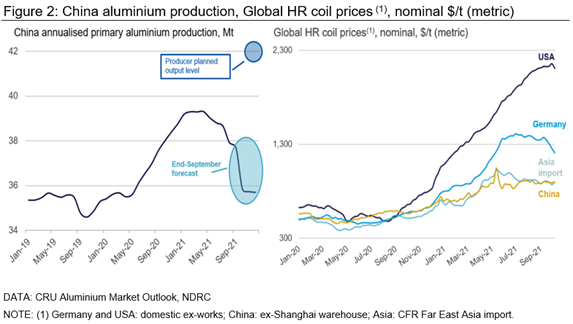

In the aluminum market, China’s production has been declining. This has pushed up prices dramatically. The continued shortages of power globally, China’s continued need to import primary aluminum and possible changes to Chinese VAT export tariffs will continue to keep prices high in 2022.

In the steel market, we have seen a growing gap between U.S. hot-rolled coil prices and other regions. European prices are gradually falling but the gap with prices in Asia is still large, in part supported by high regional freight costs. Despite high steel prices, iron ore prices have fallen sharply, driven by restrictions on Chinese steel output. We expect lower output in China as the new normal, and by 2026 China will represent less than half of global steel production.

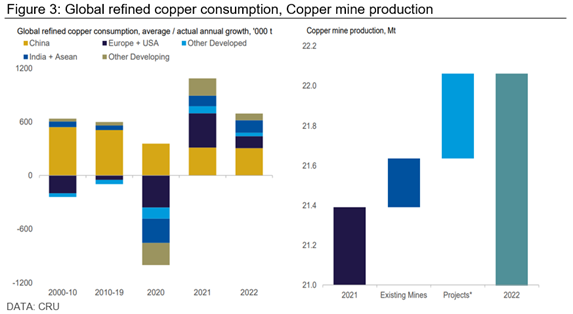

For copper, demand growth is projected to slow in 2022 with a significant slowdown in demand growth from Europe and the U.S. Mine supply will increase dramatically next year, driven by new large-scale projects to enhance production capacity. Slowing demand growth and new supply will push the market into a surplus and drive prices down. Despite that, with prices still high in absolute terms, copper miners can expect another bumper year of profits, with margins passing $4,000/tonne for the year.

The Changing Role of China

China and its policies remain hugely influential for global commodity markets. Recent changes in its policies and its evolving role are of huge interest to our clients and the industry.

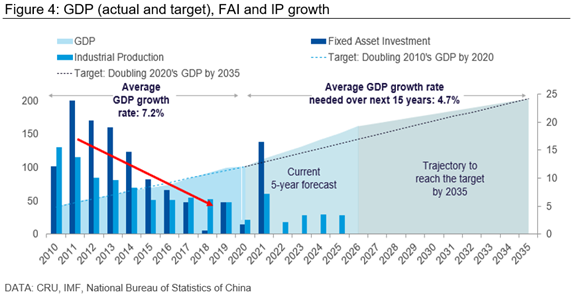

China will deepen its commitment to international leadership in a wider range of key technologies including hydrogen as well as carbon capture and storage. China’s 14th Five-Year Plan (FYP) announced in March placed a strong emphasis on high-quality economic development, enabled through ambitious levels of R&D spending and digitization.

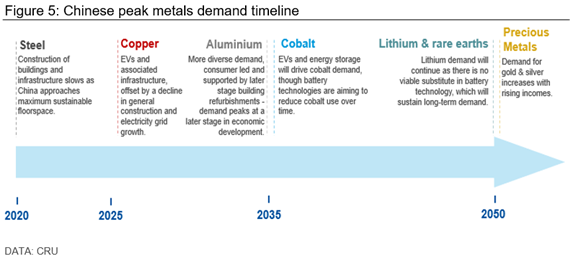

China Net-zero will require complete electrification of transport. EVs will drive base metals demand over the medium to long-term, with average growth of over 30% in EV-related demand for copper, aluminum and nickel to 2025.

China’s Three Red Lines Policy was introduced to cool the hot property market. Tighter credit has already affected property developers – witness the problems of Evergrande and Fantasia. Over the medium term to long term, there is substantial downside risk for the demand of all commodities used in construction, particularly for steel, aluminum and copper.

A common theme across the 14th FYP, Dual Circulation and Net-zero policies, is that they all work to incentivize much greater scrap collection and use. We see scrap as having the single most important impact on metals and bulk markets in China over the coming decade.

The surging commodity prices have further demonstrated the need to keep diverse sources of raw materials supply, and there is little doubt that China is looking to increase its self-reliance in key commodities. Trade interventions and geopolitics now play a bigger role today, as evident from import bans on numerous Australian exports. We are likely to see geopolitics and trade bans continue as a major feature of China’s trade in the future.

Navigating ESG: Challenges and Risks

ESG priorities are becoming more and more important for businesses and policymakers. We have established several challenges and risks in meeting these ESG commitments.

- Meeting climate commitments requires massive and rapid decarbonization. In turn this needs much higher carbon prices to incentivize the investment in new tech. That will impact metals as a big emitting sector.

- Renewables are a big part of the picture for greening of metal production, but also less proven tech.

- Social and governance considerations cannot be ignored; increasing the need to measure and report performance in a transparent way.

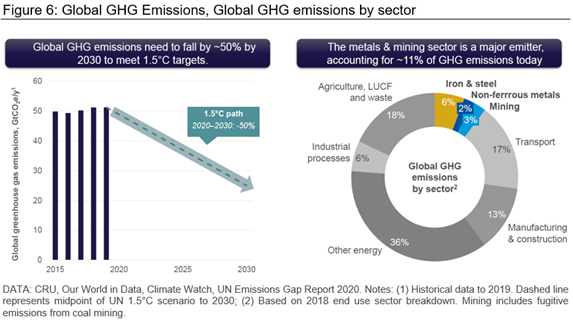

Firstly, decarbonization is a huge and costly task. With the metals and mining sectors accounting for ~11% of GHG emissions today, they have a large role to play in global decarbonization. Collectively, GHG needs to fall by ~50% by 2030 to meet the 1.5⁰C target. Renewables will be the key to decarbonization, but this energy transition could double electricity costs.

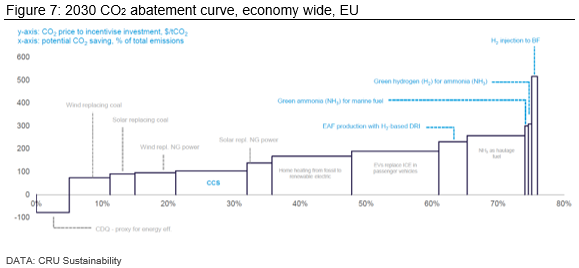

As well as renewables, other technologies, such as low emissions ammonia and hydrogen are being explored as a decarbonization solution. Ammonia has huge potential as a marine fuel, hydrogen carrier and low carbon explosive. However, these technologies are not yet economically feasible and require innovation to bring costs down.

Carbon prices are essential to incentivize decarbonization technologies. Based on CRU research, the carbon price needs to rise past $200/t to reduce total carbon emissions by 50%. Commodity prices will also need to increase to support the green transition.

Beyond environment, social and governance issues cannot be neglected. CRU research shows the increasing prominence of social value in mining. In fact, the average social contribution as a share of the profit has doubled from 3% to over 6% since 2012. Country-specific governance issues could also alter commodity dynamics as well. For instance, the imposition of trade bans, royalties and environmental regulations and permitting are increasingly commonplace. Multiple resource-rich, mining active countries have raised royalties and taxes to aid with closing budget gaps created by Covid-19.

Watch the CRU Breakfast 2021 recordings:

Is the Commodity boom here to stay?

Navigating ESG Challenges and Risks

Download the CRU Breakfast 2021 slides:

Navigating ESG Challenges and Risks

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com