Market Data

November 8, 2021

Employment by Industry: October’s Results Surprise

Written by David Schollaert

October saw a major improvement for the U.S. labor market and a sign of optimism as the latest coronavirus surge eases. The latest data from the U.S. Bureau of Labor Statistics showed that the economy created a noteworthy 531,000 new jobs in October following disappointing monthly results in August and September.

October’s results included nearly 100,000 more jobs than previously anticipated, but was still well below the peak of 1.091 million positions added in July. Nevertheless, the month-on-month recovery was a welcome mark to kick off the fourth quarter, and hopefully a sign of things to come ahead of the holiday spending season.

Leisure and hospitality were again the primary drivers of job creation, adding 164,000 jobs in October. Notable job gains also occurred in professional and business services, which saw an increase of 100,000 new jobs, while manufacturing added 60,000 to their payrolls, and transportation and warehousing was boosted by 54,000 additional positions. Construction added 44,000 jobs while health care was up 37,000 and retail added 35,000 to the workforce.

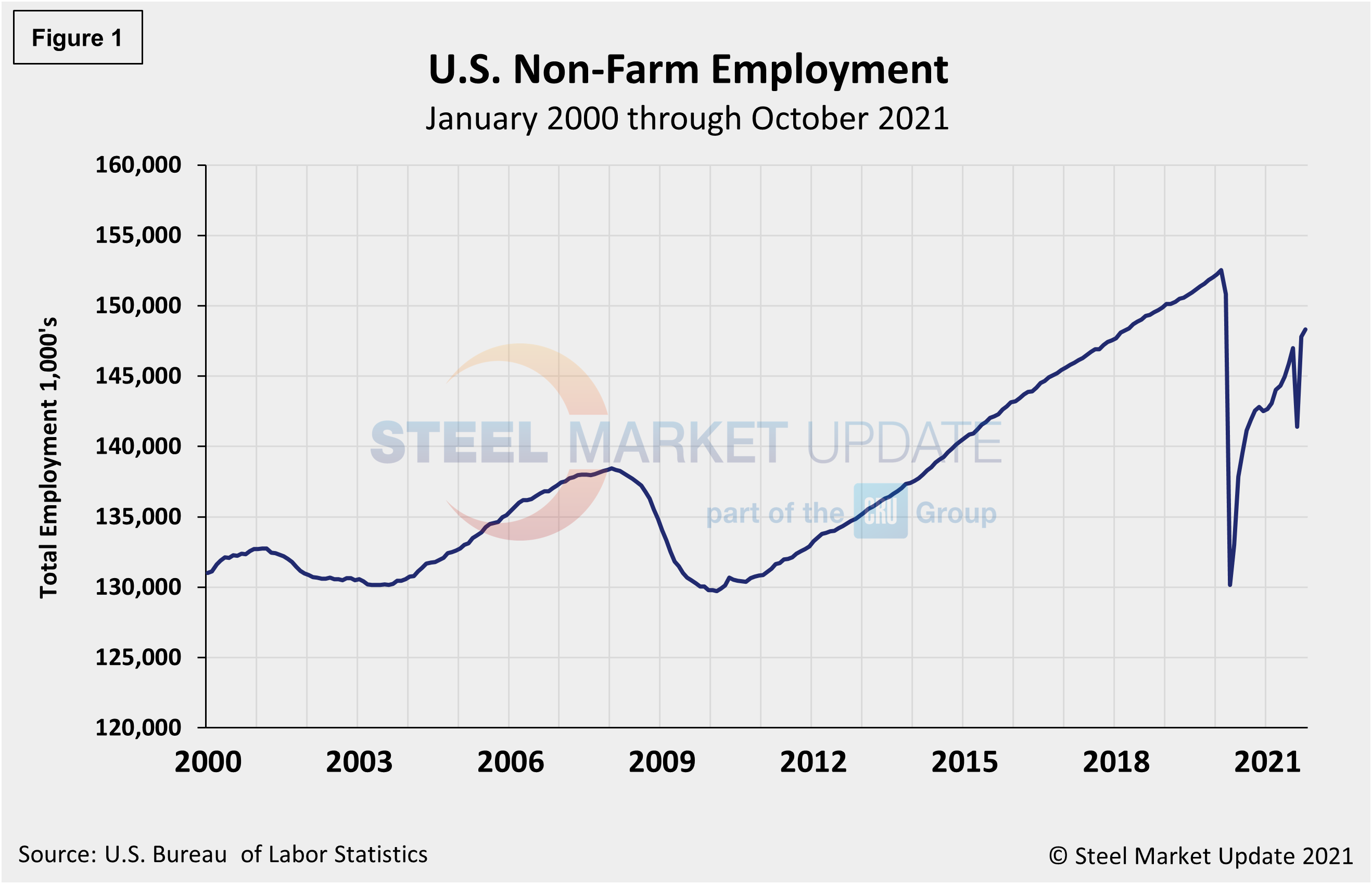

The number of unemployed persons fell by 470,000 to 6.9 million last month. To date, the U.S. has recovered nearly 15.6 million or 69% of the 22.5 million jobs lost last spring. There are still 678,000 more Americans out of work than at the start of the pandemic, a sign that the labor market recovery still has a way to go. Figure 1 shows the total number of people employed in the nonfarm economy.

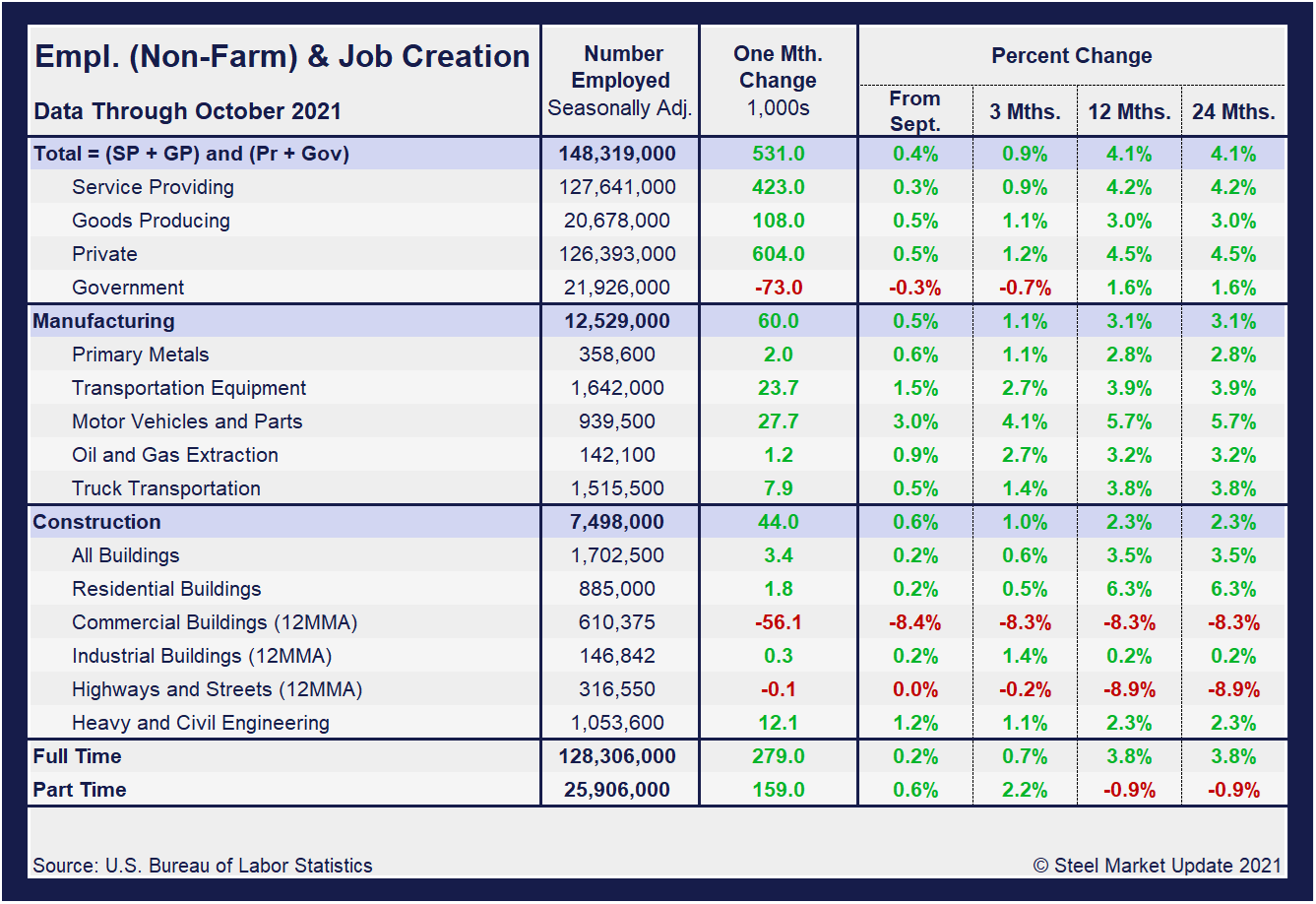

Designed on rolling time periods of 1 month, 3 months, 1 year and 2 years, the table below breaks total employment into service industries and goods-producing industries, and then into private and government employees. Most of the goods-producing employees work in manufacturing and construction. Comparing service and goods-producing industries in October shows service jobs have increased by just 0.3%, while goods-producing jobs rose by 0.5% from September’s result. The steady month-on-month gains have pushed both industries beyond pre-pandemic levels for the first time. Note, the subcomponents of both manufacturing and construction shown in this table don’t add up to the total because we have only included those with the most relevance to the steel industry.

Comparing October to September, manufacturing employment was up 0.5% versus a gain 0.2% the month prior. Construction was up 0.6% month on month compared to a 0.3% increase in September. The construction sector has been driven by the residential market, a 6.3% increase year on year. Gains have been held back, however, by struggling commercial building and highway and streets markets. Despite the overall improvement, the inconsistencies in some of the subcomponents reflects the significant obstacles still facing the U.S. economy and domestic job creation. The recovery has been remarkable, nevertheless, as the three-month, 12-month and 24-month comparisons are mostly reporting growth. In the year-over-year contrast, manufacturing is up just 3.1% and construction is up 2.3%. Further growth is still expected as the marketplace advances from the freefall seen during the second quarter of 2020.

Manufacturing employment increased by 60,000 jobs in October compared to an increase of 26,000 the month prior, led by gains of 28,000 in motor vehicles and parts. Employment also rose in fabricated metal products by 6,000, while chemicals were up 6,000, and printing and related support activities gained 4,000. Manufacturing employment is down by 270,000 compared with February 2020, however.

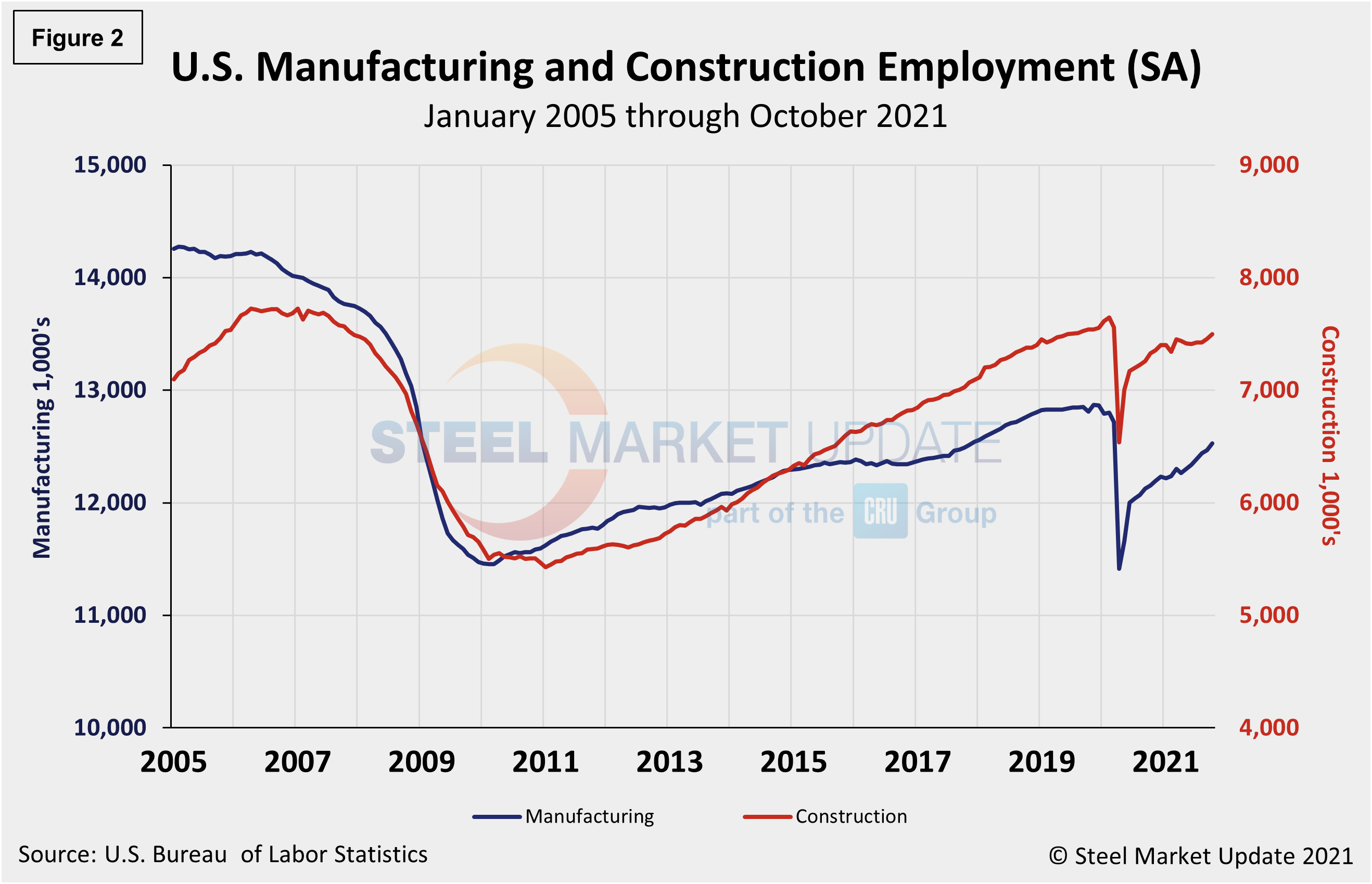

In October, construction employment rose by 44,000, following a 30,000 increase the month prior. Employment among nonresidential specialty trade contractors increased by 19,000, and in heavy and civil engineering construction by 12,000. Construction employment is still 150,000 below its February 2020 level. The history of employment in manufacturing and construction since January 2005 is show below in Figure 2, seasonally adjusted.

For the third month in a row, companies in the health care/products sector announced the most job cuts with 6,694. This industry includes hospitals and other health care facilities, as well as health care products manufacturers. So far this year, this industry has announced 25,630 cuts, the second most for any industry and 56% lower than the 58,105 cuts announced through the same period in 2020.

Aerospace/defense companies have announced the most cuts this year with 34,207, 57% lower than the 79,861 announced through the same period last year. Telecommunications providers announced the third most cuts this year with 25,481, down 15% from the 29,999 announced through October 2020.

Despite the job cuts, human resources consulting firm Challenger, Gray and Christmas Inc., said the numbers are still very low. “We’re still seeing record-low job cut announcements and the record quits rate and number of job openings suggests workers are really calling the shots right now,” said Challenger.

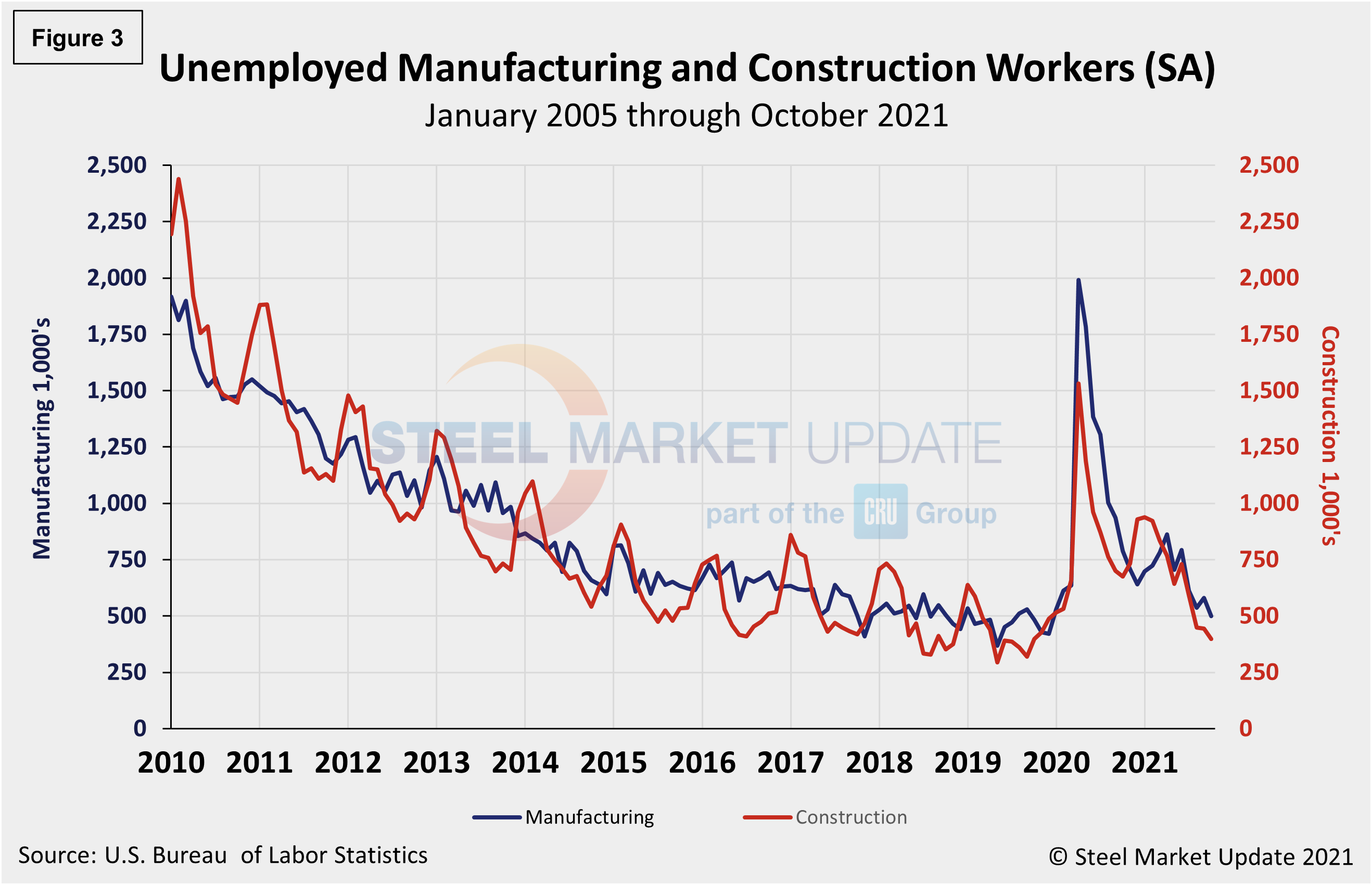

The reported number of unemployed manufacturing and construction workers is shown in Figure 3. Construction and manufacturing unemployment decreased in October when compared to the month prior. Construction unemployment was down 10.4% month on month, from 444,000 in September to 398,000 in October. Manufacturing’s unemployed persons fell from 580,000 in September to 499,000 in October, a 14.0% decline month on month. Both sectors have been heavily impacted by supply-chain disruptions and labor force constraints, and October’s improvements are significant.

Explanation: On the first or second Friday of each month, the Bureau of Labor Statistics releases the employment data for the previous month. Data is available at www.bls.gov. The BLS employment database is a reality check for other economic data streams such as manufacturing and construction. It is easy to drill down into the BLS database to obtain employment data for many subsectors of the economy. The important point about all these data streams is not necessarily the nominal numbers, but the direction in which they are headed.

By David Schollaert, David@SteelMarketUpdate.com