Overseas

December 9, 2021

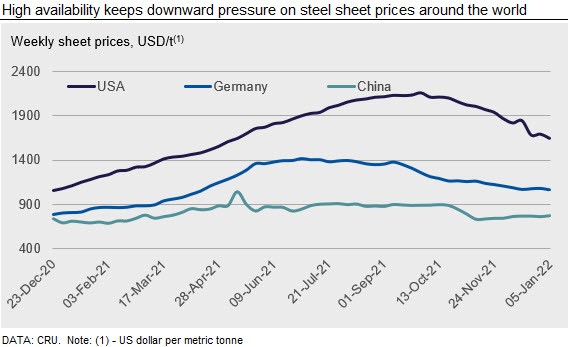

CRU: Global Sheet Prices Continue to Fall on Increasing Availability

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor, Jan. 5

Sheet prices fell in most markets around the world as supply availability grew. In the USA, market participants report that end users are cancelling or postponing orders, which has led to an even greater build up in inventory levels and caused most sheet prices to fall w/w. A similar situation is true for Europe, where inventories are also building and competitively priced imports, especially from India, continue to put downward pressure on prices. In part, these competitive offers have come about as domestic producers in India face their own pressure from competitively priced imports from northern Asia. In China, prices were unchanged w/w but demand weakness and rising inventories will likely result in further price falls in the near term.

USA

U.S. HR coil and HDG coil prices fell last week, while CR coil prices ticked up slightly. Many buyers said they have not sought new mill pricing over the past two weeks due to the holiday season. Numerous service centers and distributors have reported that customers are cancelling or postponing orders as well as adjusting forecasts downward, leading to speculation that these orders were placed at multiple vendors to ensure supply. These revisions have led to higher inventory levels, forcing buyers to limit new purchases to only those guaranteed to ship immediately.

Activity on the U.S. West Coast was also slow this week as many buyers remained on holiday break. While imports are expected to play a significant role in 2022, some companies have begun shifting back to domestic sources in preparation for infrastructure work that stipulates material must be melted and poured in the USA. There has been increased availability to the West Coast from Midwest and Southern mills, but prices have not been competitive enough yet to compete with local mills or imports.

Europe

European sheet prices have continued their downwards trend into the new year as both northern and southern European prices decreased to price levels not seen since April 2021. In Germany, prices fell between €12-€15 /t w/w, while decreasing in Italy by €6-€12 /t w/w across all sheet products. Stock levels seem to still be high for distributors and end-users. Spot business was expected to be weak in the first couple of weeks this month, especially as half and full-year contracts for 2022 are still being negotiated.

Indian import offers for both HR coil and CR coil have been heard at competitive price levels, including offers to Italy at just below €800 /t CFR, including duties, for January-February shipment.

China

Chinese domestic sheet prices went up slightly this week after the holidays, yet transactions remained scarce. The CFLP manufacturing PMI was 0.2 percentage points higher m/m in December, which pointed to a continuous recovery in manufacturing including sheet-consuming automotive and appliance sectors. Likewise, blast furnace output picked up and utilization rates rose last week even as inventories piled up significantly during the holiday week. Meanwhile, participants are still reluctant to return given sluggish market conditions. Therefore, sheet prices will face continuous supply-side pressure before the Chinese New Year holiday. Still, mill profitability will remain around current levels as production costs stay low.

Asia

Imported sheet product prices in Asia were flat w/w amid limited trading activity.

Even though offers slightly increased by $5-10/ t this week to $765-775 /t CFR Vietnam for HR coil SAE1006 grade, buying indications were heard at below $750 /t CFR Vietnam. Offers for HR coil SS400 grade were heard at $768 /t CFR Vietnam with mute buying interest.

According to market sources, even though inventory is not high in Vietnam buyers remain reluctant to restock because of a bearish demand outlook.

CRU assessed HR coil prices at $760 /t CFR Far East Asia, while CR coil prices were assessed at $920 /t CFR. HDG prices were assessed at $950 /t. All prices were unchanged from the prior week.

India

Spot sheet prices in India weakened further at the start of 2022, falling by INR1000-1300 ($13-17) /t w/w, as key end users continued to hold off purchases. Given the continued weakness in Asian markets and a widened differential between domestic and export offers for HR coil, local buyers are expecting further downward revisions to Indian prices. Meanwhile, major sheet producers have decided to officially roll over sheet prices for January 2022, while trade discounts remain in place to boost buying.

A key pain point for Indian steelmakers is the sharp decline in exports during November and December, which has led to a rise in mill and trade inventory in the domestic market. Although they do expect export sales to revive once European quotas open for 2022 Q1, price competition has intensified amongst Asian suppliers, so price realization may not be attractive for sales even to Europe. Currently, Indian mills are offering HR coil to SE Asian buyers at $740-750 /t CFR, while similar quality HR coil is being offered to buyers in the Middle East at $760-770 /t CFR. Furthermore, another concern for Indian steelmakers is a gradual rise in HR coil imports to India, particularly from NE Asian suppliers, who have reduced their export price offers, following eased input costs. Given the trade dynamics, domestic sheet prices are likely to remain under pressure at least until the Chinese New Year holidays.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com