Analysis

January 18, 2022

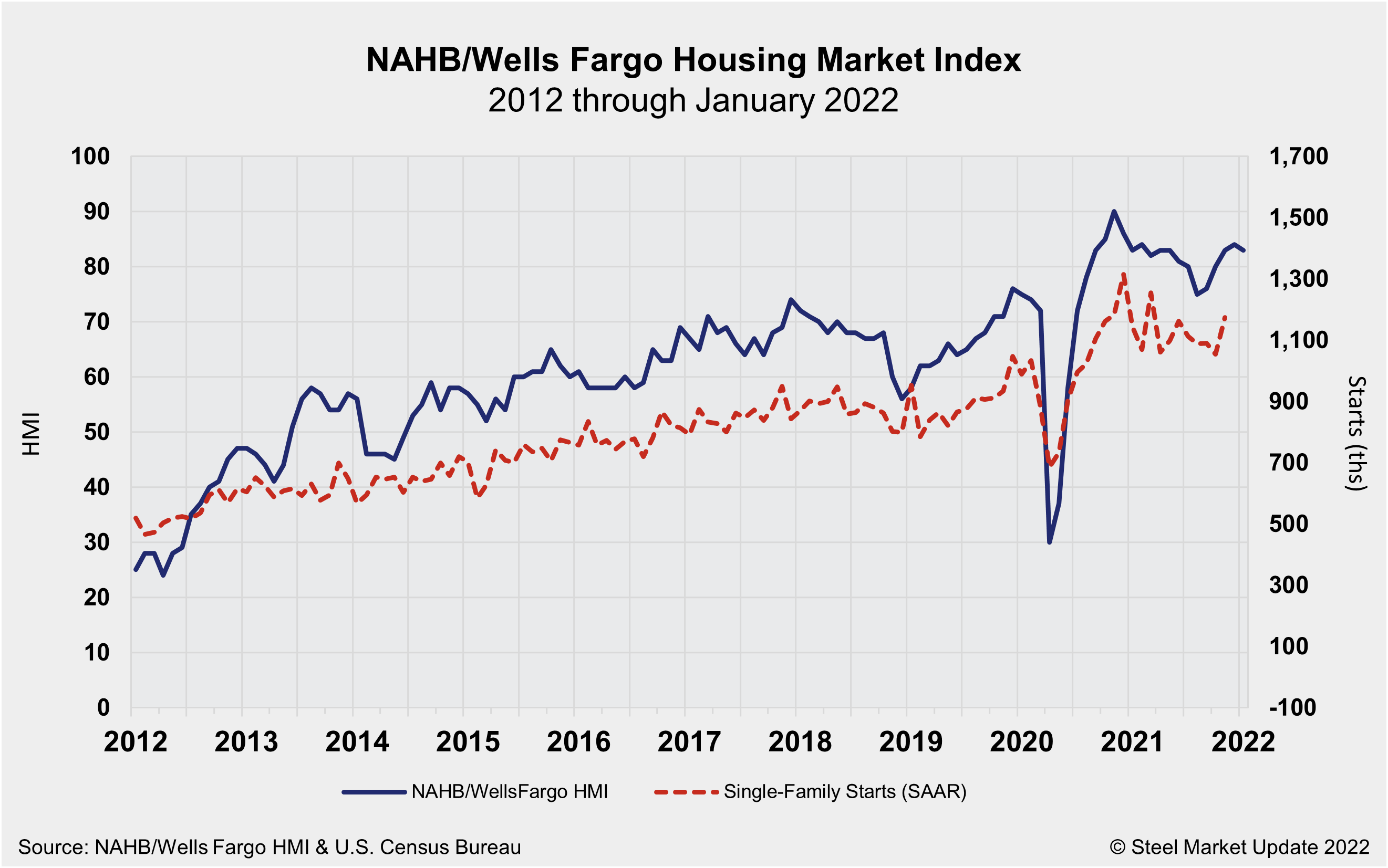

NAHB: Builder Confidence Slips in January

Written by David Schollaert

Builder confidence slipped in January, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI). Growing inflation concerns and ongoing supply-chain disruptions snapped a four-month rise in home builder sentiment even as consumer demand remains robust. January’s HMI reading moved one point lower to a reading of 83.

“Higher material costs and lack of availability are adding weeks to typical single-family construction times,” said Chuck Fowke, NAHB’s chairman. “NAHB analysis indicates the aggregate cost of residential construction materials has increased almost 19% since December 2021. Policymakers need to take action to fix supply chains. Obtaining a new softwood lumber agreement with Canada and reducing tariffs is an excellent place to start.”

The NAHB/Wells Fargo HMI survey gauges builder perceptions of current single-family home sales and sales expectations for the next six months as “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as “high to very high,” “average” or “low to very low.” Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view conditions as good than poor.

Two out of the three major HMI indices posted decreases in January. The gauge charting traffic of prospective buyers posted a two-point decline to 69 while the component measuring sales expectations in the next six months also fell two points to 83. The index gauging current sales conditions held at 90.

“The HMI data was collected during the first two weeks of January and do not fully reflect the recent jump in mortgage interest rates,” said Robert Dietz, NAHB’s chief economist. “While lean existing home inventory and solid buyer demand are supporting the need for new construction, the combination of ongoing increases for building materials, worsening skilled labor shortages and higher mortgage rates point to declines for housing affordability in 2022.”

Looking at the three-month moving averages for regional HMI scores, the Northeast fell one point to 73, the Midwest increased one point to 75 and the South and West each posted a one-point rise to 88, respectively.

By David Schollaert, David@SteelMarketUpdate.com